7 Peculiarities of Rural Credit in the Cerrado: Private Resources Attracted to Finance Large Producers Contrast with Scarcity of Credit for Family Farming

The Cerrado plays a central economic role in Brazilian agricultural production, accounting for a relevant share of agricultural commodities.[1] The biome is responsible for approximately half of the nation’s soy production, a product whose grains, meal, oils, and by-products represented, in 2019, 34% of the country’s agribusiness exports and around 15% of its total exports.[2],[3]

This economic relevance has been increasing over the last few decades. Reconciling agricultural production with greater sustainability is crucial. With growing international concern about climate issues, sustainable cultivation practices are essential to ensure a good placement in global trade chains. It is possible to increase production and, at the same time, preserve native vegetation. Between 2004 and 2019, the growth of agricultural production in the biome was accompanied by significant reductions in deforestation rates.[4] Building on this process while avoiding setbacks is one of the challenges facing public policies in this biome.

To act effectively in the region, it is necessary to understand the Cerrado. The biome boasts significant economic and social diversity. In terms of geography, it is present in the five regions of the country and it spans 10 states and the Federal District. Additionally, the distribution of agricultural activities across these states varies considerably.

Rural credit, the primary public policy instrument available for agriculture, plays an important role in financing producers in the biome. In this brief, researchers from Climate Policy Initiative/Pontifical Catholic University of Rio de Janeiro (CPI/PUC-Rio) analyze the key features of rural credit in the Cerrado biome and highlight the specificities of the region’s agricultural activities. This work complements the previous analysis of rural credit in the Amazon conducted by CPI/PUC-Rio and seeks to provide a deeper understanding of rural financing in the Brazilian biomes.[5] This analysis aims to help improve the credit policy and adapt this instrument to the specific challenges and context of the Cerrado.

This analysis points to the existence of a considerable credit market which is proportional to the volume of its agricultural activity in the domestic market. The Cerrado biome accounts for approximately one third of the country’s rural credit and agricultural production. Soy production has expanded in parallel to a growing concentration of financial flows in the Cerrado. Average contract values are 181% higher than in the rest of the country. Credit for small and medium producers is relatively scarce. Public policy must consider whether suitable credit conditions are being offered to smaller producers. Previous studies by CPI/PUC-Rio show that credit provided to small and medium-sized producers increases agricultural productivity and alleviates deforestation pressures.[6]

The Cerrado also stands out in the use of financing from private sources, with fewer government subsidies and less targeting. While Agricultural Credit Notes (Letra de Crédito do Agronegócio – LCA) and Rural Savings – Unrestricted[7] have been on the rise, public banks – especially Banco do Brasil and Banco do Nordeste – remain the primary financial institutions for rural credit operations. Therefore, there is room to increase private sector participation and foster more competition among banks in the region.

BOX 1. MAIN CHARACTERISTICS OF RURAL CREDIT IN THE CERRADO

1. The volume of rural credit directed towards the Cerrado is proportional to the value of its agricultural production: approximately a third of both the country’s rural credit and agricultural production are in the biome. Most of the rural credit in the Cerrado is channeled to crops: 68% of the total amount of contracts went to crop production in the 2019/20 agricultural year.[8] Soy accounts for 38% of the R$ 50 billion loaned for crop production in the biome. In the rest of the country, soy accounts for only 28% of the total credit amount destined to crops.

2. Rural credit is more concentrated in the Cerrado than in the rest of the country. In 2019/20, the average contract value in the Cerrado was R$ 224,000, 181% higher than the average contract value in the aggregate for the other biomes. In addition to being historically higher than in the rest of the country, the average value of contracts in the Cerrado has been rising in recent years.

3. Credit volume varies considerably across the municipalities located in the Cerrado. When analyzing the territorial distribution of the ratio between the volume of rural credit and the Gross Value Added of agriculture, it appears that the central region (the Brazilian states of Goiás, Mato Grosso, and Tocantins) makes more intensive use of credit. Analysis at the state level indicates that in São Paulo, Tocantins, and Goiás, the ratio between rural credit and the value of agricultural production is 0.98, 0.88, and 0.85 (respectively), whereas in Maranhão, Piauí, and Bahia, the ratios are 0.49, 0.48 and 0.42, in that order.

4. Though the high average value of contracts may be related to larger property sizes, most of the credit in the biome is borrowed by individuals. In the 2019/20 agricultural year, 99% of all credit operations and 85% of the total amount went to individuals, and the rest to companies.

5. The share of public banks in the Cerrado rural credit market is considerably higher than that of private banks. In the 2019/20 agricultural year, Banco do Brasil was the main credit provider in 72% of the municipalities that make up the biome and was responsible for 50% of the credit volume. Banco do Nordeste (another public bank) was the largest lender in 19% of the municipalities, accounting for 5% of all rural credit volume. Bradesco, a private bank, was the largest lender in only 1% of the municipalities, with 7% of the credit volume. Overall, competition in rural credit markets is low in the Cerrado, as in the rest of Brazil.

6. Despite the predominance of public banks, proportionally the Cerrado has attracted more private resources for financing agriculture than the rest of the country. The shares of LCA and Rural Savings – Unrestricted – which were close to zero in 2002/03 – increased to 19% and 15% of the total credit amount in the 2019/20 agricultural year.[9],[10] On the other hand, Compulsory Resources and Rural Savings – Restricted have been losing importance over the years, even though Compulsory Resources remain the main source of financing in the biome.[11] In 2019/20, these sources accounted for 25% and 13% of the total credit amount, respectively.

7. Penetration of the National Program for Family Farming (Programa Nacional de Fortalecimento da Agricultura Familiar – PRONAF) in the Cerrado is limited, corresponding to only 4% of the rural credit volume in 2019/20. In fact, while the National Program to Support Medium-Sized Farmers (Programa Nacional de Apoio ao Médio Produtor Rural – PRONAMP) is more relevant than PRONAF, it accounted for only 13% of all credit in the same period. In the rest of Brazil, PRONAF and PRONAMP were responsible for 22% and 16% of the credit volume, respectively. As such, most of the rural credit in the Cerrado is not associated to programs and follows the rules of the respective sources (76% of the total amount in the 2019/20 agricultural year). Loans with these characteristics are more often associated with medium and large-scale producers.

1. AGRICULTURE IN THE CERRADO

Soy is the Cerrado’s most important crop. In 2019, soy production in the biome amounted to R$ 63 billion (in actual amounts as of December 2020[12]), which corresponds to 43% of the total value of crop in the biome and represents an increase of 159% from 2002. Elsewhere in Brazil, the value of soy production was R$ 69 billion in 2019, equivalent to 30% of the value of crop production in the rest of the country.[13]

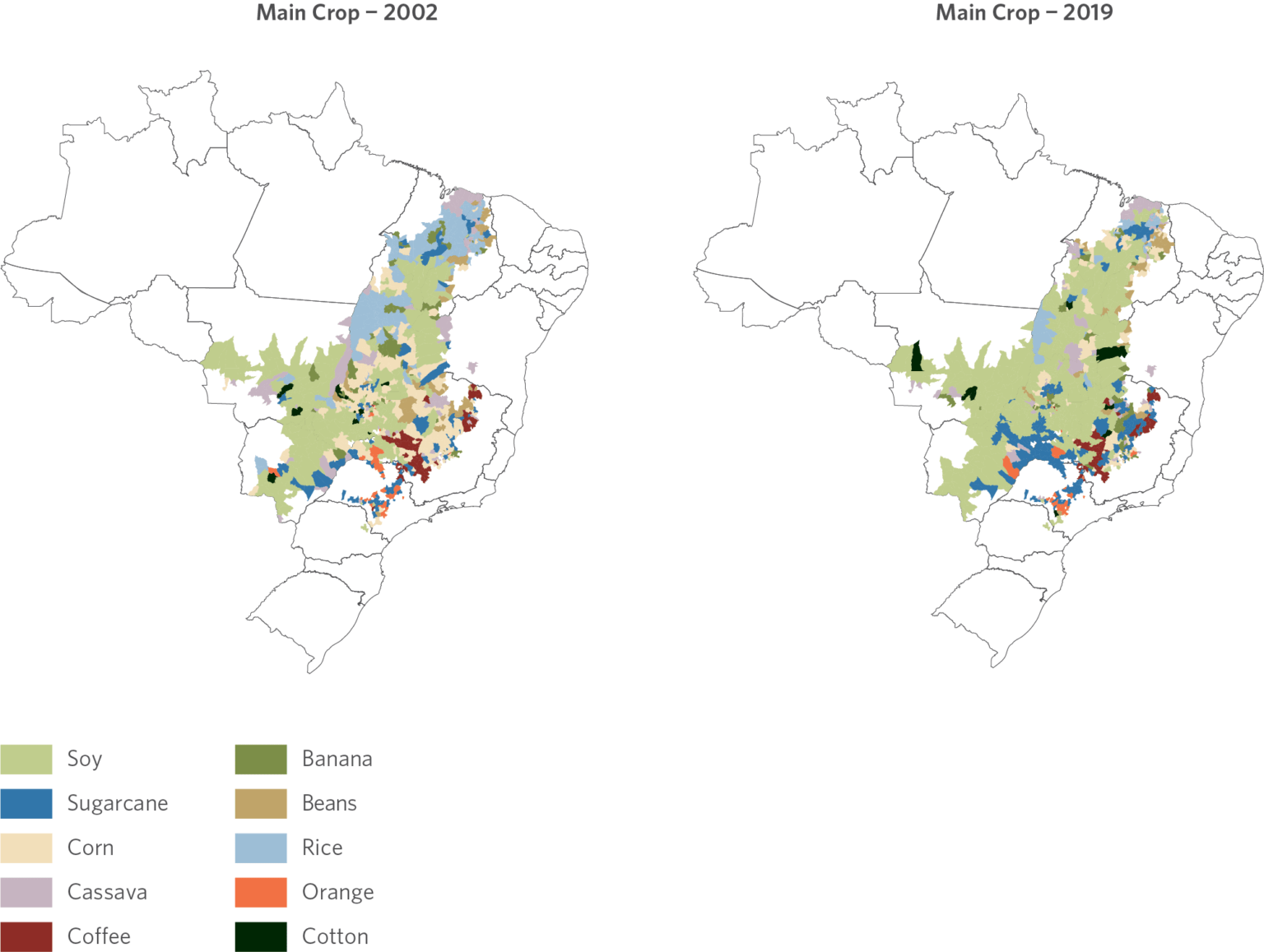

Figure 1 shows the main crop in produced value by municipality in the Cerrado. In addition to being the predominant product in most municipalities in 2002 and 2019 alike, soy gained additional relevance during this period. More specifically, soy overtook rice to become the primary crop in most of the municipalities in the states of Maranhão, Piauí, and Tocantins, and surpassed corn in parts of Goiás, Minas Gerais, and Tocantins. Even so, corn is the second biggest product in terms of produced value in the entire biome, reaching R$ 24 billion in 2019 (a 207% increase from 2002). Sugarcane and cotton also stand out in the Cerrado. In 2019, these crops produced R$ 22 billion and R$ 15 billion in the biome, respectively (up 229% and 315% from 2002).

Figure 1. Main Crop by Municipality in the Cerrado, 2002 and 2019

Note: The main crop is the one with the highest production value in a given municipality for a given year. December 2020 constant values (inflation adjusted by IPCA).

Source: CPI/PUC-Rio with data from IBGE’s Produção Agrícola Municipal (PAM), 2021

The growth of cattle ranching in the Cerrado was less pronounced. The region’s cattle herd grew 6% between 2002 and 2019, while the rest of the country experienced a 22% increase in the same period.[14] The area devoted to pasture in the biome in this period fell by 4%; however, in 2019, 70% of the area devoted to agriculture in the Cerrado was still used for pasture and 30% was used for crop production.[15] Other biomes only experienced a 1% decline in pasture areas between 2002 and 2019. In 2019, 73% of the area devoted to agriculture in the other biomes were used for pasture.

Within the Cerrado biome, the evolution of agricultural production in the MATOPIBA region also stands out.[16] Between 2002 and 2019, the municipalities in MATOPIBA experienced a 299% growth in crop production value. In the other municipalities that make up the Cerrado region, the increase was 132%. In terms of value growth during the period, the crops that stood out in the region included cotton (+ 1,019%), soy (+ 437%), and corn (+ 220%). Livestock has also been growing at an accelerated pace. Cattle production in MATOPIBA increased 32% between 2002 and 2019 compared to a 3% increase in the rest of the biome in the same period. Even so, the region’s overall contribution to the biome’s agricultural production remains limited: in 2019, MATOPIBA accounted for 16% of the value of crop production in the Cerrado, and 13% of the cattle herd. In 2002, the region’s shares were, respectively, 10% and 11%.

Strong agricultural production – especially soy and corn – has helped to increase the Cerrado’s contribution to the value of Brazilian agricultural production over the years (Figure 2). On the other hand, the participation of the biome in cattle production – represented by the number of head of cattle – shows a downward trend in the period under analysis.

Figure 2. Evolution of Cerrado’s Share in Brazil’s Agricultural Production, 2002-2019

Source: CPI/PUC-Rio with data from IBGE’s Produção Agrícola Municipal (PAM) and Pesquisa da Pecuária Municipal (PPM), 2021

Between 2002 and 2019, the value of crop production in the Cerrado increased 149%, reaching a total of R$ 147 billion in 2019. For the rest of Brazil, the growth rate was 60% and the total produced was R$ 231 billion in 2019. As a result, there was a robust 10 percentage point increase in the biome’s contribution to the value of Brazil’s crop production, from 29% in 2002 to 39% in 2019. The ratio between head of cattle in the biome and the country’s total decreased slightly. In 2002, the Cerrado accounted for 36% of all head of cattle; in 2019, it was 33%.

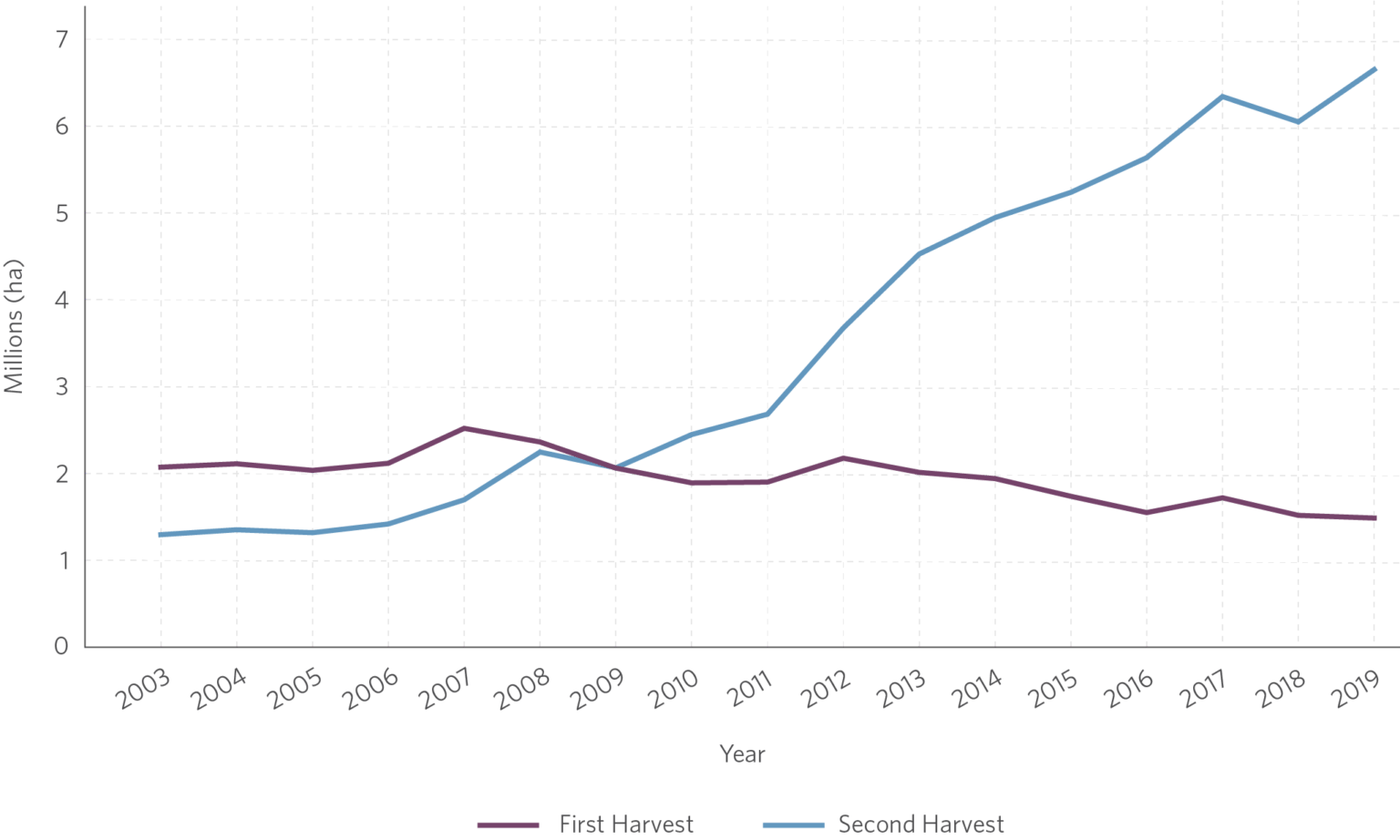

BOX 2. THE INTENSIFICATION OF OFF-SEASON CORN PRODUCTION

Second crop corn has been gaining relevance in the Cerrado’s annual production. Also known as off-season harvest or safrinha in Portuguese, the second crop harvest cycle begins after the main harvest that usually involves soy or even corn itself. Though it takes place under less favorable climate conditions, the off-season used to be an additional source of income for rural producers. In recent years, however, there has been a change in producers’ behavior, who have prioritized growing soy as the main crop and corn as the second crop. In 2003, 2 million hectares in the Cerrado were devoted to the production of corn as a first crop, and 1.3 million as a second crop. In 2019, 1.5 million hectares were used for grain production in the first harvest, and 6.7 million hectares in the second harvest. Figure 3 below shows this evolution.

Figure 3. Evolution of the Area for Corn Production in the Cerrado, 2003-2019

Source: CPI/PUC-Rio with data from IBGE’s Produção Agrícola Municipal (PAM), 2021

This change of pattern in the area devoted to each crop is reflected in corn production. In 2003, the second harvest accounted for 37% of the total amount of the grain produced in the Cerrado, while 63% of the total was produced in the first harvest. In 2010, the second harvest surpassed the yield of the first harvest in the biome and, in 2019, it accounted for 82% of the amount produced in the Cerrado – a total of 41 million tons. In the same year, the first corn harvest in the biome totaled 9 million tons. The off-season corn harvest has also grown in importance in the rest of the country, increasing from 24% of all corn production in 2003 to 67% in 2019.

2. VOLUME AND COMPOSITION OF RURAL CREDIT IN THE CERRADO

The rural credit market in the Cerrado is considerable and compatible with its agricultural production size. The biome accounts for, approximately, a third of the credit volume and, also, a third of Brazilian agricultural output. Rural credit in the Cerrado is more concentrated than in the rest of the country. In addition to being historically higher than in the rest of the country, the average value of contracts of rural credit in the Cerrado has been rising in recent years.

Regarding the composition of rural credit in the biome, soy and cattle boast the largest shares, accounting for 26% and 25%, respectively, of the total value of rural credit in the Cerrado (Figure 4). In the rest of Brazil, the percentages are lower: 18% for soy and 20% for cattle. Even so, other crops are also relevant in terms of credit in the Cerrado, indicating the dynamism of agricultural activities in the region. Among them is corn, which accounts for 10% of the total loaned amount, and coffee, which accounts for a further 5%.

Figure 4. Rural Credit Composition by Product and Activity in the Cerrado, 2019/20

BY PRODUCT

BY ACTIVITY

Note: The category “Others” includes rice, milk, eucalyptus, and 140 other products.

Source:CPI/PUC-Rio with data from SICOR from Central Bank of Brazil, 2021

Breaking rural credit down by activity, cattle production is the primary activity by number of contracts (70% of the total), while the remaining 30% correspond to crop production. The statistics are the opposite in terms of the total value of operations – crop production accounts for 68% of the total volume, and cattle accounts for 32%. This shows that the average contract value for crops is much higher than for cattle in the Cerrado. The breakdown is similar for the rest of the country: 64% of the amount of rural credit contracts were allocated to crop production in 2019/20, and 36% to livestock.

As for the evolution of the total amount of rural credit contracts in the Cerrado, the trend is positive until the 2013/14 agricultural year, when, following an economic crisis in the country, the total value of contracts in the biome starts to decline. The indicator resumes growth in 2017/18, reaching R$ 73 billion in 2019/20, a level close to the 2013/14 peak of R$ 74 billion.

Furthermore, there has been a concentration of financial flows. In 2019/20, the average contract value of rural credit in the Cerrado was 181% higher than the average for other biomes (Figure 5).[17] As in the rest of the country, the average value has increased in recent years. In the Cerrado, the average value of rural credit contracts increased from R$ 96,000 in 2002/03 to R$ 224,000 in 2019/20 (an inflation-adjusted increase of 134%). For the rest of the country, the average value was R$ 80,000 in 2019/20, up from R$ 36,000 in 2002/03 (an inflation-adjusted increase of 119%).

Figure 5. Evolution of the Number, Volume and Average Value of Rural Credit Contracts in the Cerrado and Other Biomes, 2002/03 – 2019/20

5a. Evolution of the Number of Contracts

5b. Evolution of the Volume of Contracts

5c. Evolution of the Average Value of Contracts

Note: Data refer to rural credit contracts and consider working capital, investment, trade, and industrialization. December 2020 constant values (inflation adjusted by IPCA).

Source: CPI/PUC-Rio with data from RECOR and SICOR from Central Bank of Brazil, 2021

The higher average value of rural credit contracts in the Cerrado are tied to agricultural establishments that are historically larger than elsewhere in the country (Figure 6). In 2017, the average area of agricultural establishments[18] in the Cerrado was 154 hectares, in contrast to 54 hectares in the other biomes.[19] In the Cerrado, the average area of establishments devoted to crop is very close to the average area devoted to livestock – 151 hectares on average for the former and 155 hectares on average for the latter. In the rest of Brazil, the difference between the two activities is significantly greater in terms of average establishment area: an average of 34 hectares for crop establishments and 74 hectares for establishments devoted to livestock.

Figure 6. Average Area of Agricultural Establishments in the Cerrado and Other Biomes, 2006 and 2017

Between the last two Agricultural Censuses (2006 and 2017), the average area of crop establishments in the Cerrado increased by 45%, compared to 16% in the rest of the country. As a result, the Cerrado became the biome where the establishments devoted to crop span the largest average areas (in 2006, the Pantanal was number one in average area devoted to crop production). On the other hand, the average area of establishments devoted to livestock production decreased, which is tied to the intensification of production. There was a 14% drop between 2006 and 2017 in the Cerrado, while in the other biomes the reduction was 2%.

3. HETEROGENEITIES IN THE CERRADO BIOME

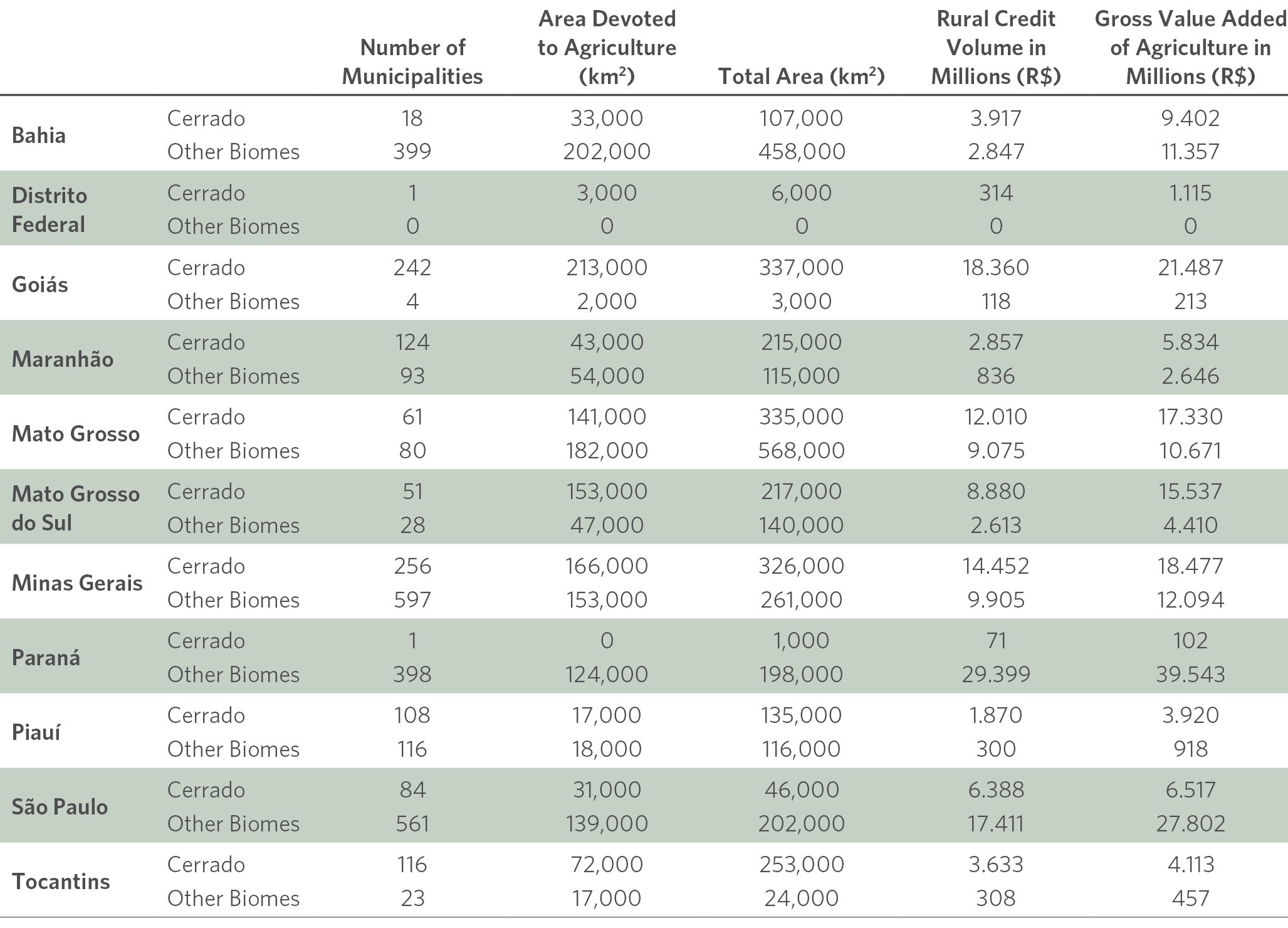

There is considerable heterogeneity between the municipalities that comprise the Cerrado. This section analyzes the different characteristics of rural credit contracts in the Cerrado biome. The Cerrado spans 10 states and the Federal District. In general, the biome encompasses only part of each state. Table 1 shows the distribution – between Cerrado and other biomes – of the number of municipalities, the area devoted to agriculture, the total area, the rural credit volume, and the Gross Added Value of agriculture by state.[20] The analyses below refer only to municipalities classified as belonging to the biome.

Table 1. Number of Municipalities, Area Devoted to Agriculture, Total Area, Rural Credit Volume, and Gross Value Added of Agriculture by State in the Cerrado and in Other Biomes, 2018

Note: December 2020 constant values (inflation adjusted by IPCA).

Source: CPI/PUC-Rio based on data from IBGE, MapBiomas and SICOR from Central Bank of Brazil, 2021

In the 2019/20 agricultural year, most of the amount of credit contracts in the Cerrado was concentrated in the states of Goiás (25%), Minas Gerais (21%), Mato Grosso (14%), and Mato Grosso do Sul (14%), as shown in Figure 7. As such, four states accounted for 74% of all the credit volume in the biome. This share is similar to the shares of these states’ agriculture areas within the Cerrado (77% of the total biome).

Figure 7. Evolution of Rural Credit Volume by State in the Cerrado, 2002/03 – 2019/20

Note: The data refer to rural credit contracts and consider working capital, investment, trade, and industrialization purposes. Amounts deflated by the IPCA, using December 2020 as reference.

Source: CPI/PUC-Rio with data from RECOR and SICOR from Central Bank of Brazil, 2021

There are striking differences in the ratio between rural credit and Gross Value Added of agriculture in the Cerrado states. In 2018, while São Paulo, Tocantins, and Goiás had ratios of 0.98, 0.88 and 0.85 (respectively), Maranhão, Piauí, and Bahia had ratios of 0.49, 0.48 and 0.42, in that order. This indicates significant heterogeneity in access to credit across the different regions of the Cerrado.

Municipalities in the MATOPIBA region are increasing their share in the total amount of loans in the Cerrado, although the current percentage remains relatively modest. In 2002/03, MATOPIBA accounted for 9% of the total value of operations in the Cerrado. By 2019/20, it had risen to 16%. Credit in this region is mainly used for soy (40% of the total amount), cattle (18%), and infrastructure and real estate products (11%). In comparison to the rest of the biome, therefore, soy has a bigger share and cattle has a smaller share.

The analysis of the ratio between rural credit and agricultural Gross Value Added shows that credit use in MATOPIBA appears to be less intense than in other Cerrado municipalities. In 2018, this indicator had a value of 0.55 in MATOPIBA, compared with 0.74 in the rest of the biome.

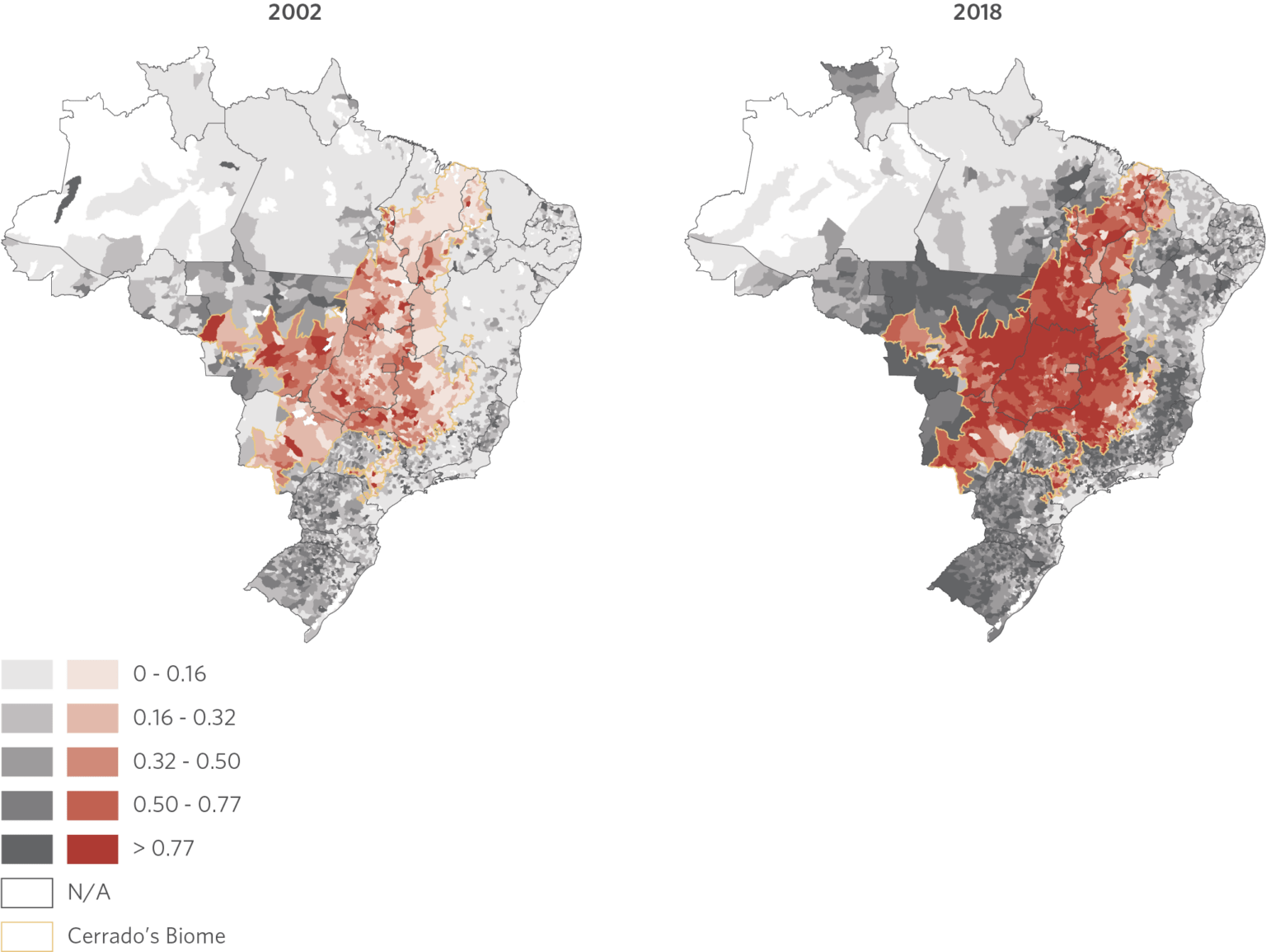

The intensity of credit use in agriculture is also analyzed geographically in Figure 8, which shows the territorial distribution of the ratio between the volume of municipal rural credit and the Gross Added Value of municipal agriculture for the years 2002 and 2018. Over those years, there was a noticeable increase in the use of rural credit in relation to the agricultural added value. Additionally, the maps suggest heterogeneity in this indicator as well. The central region (Goiás, Mato Grosso, and Tocantins) is more credit intensive. On the other hand, more extreme regions like Maranhão show much lower credit intensity than the rest of the biome. This pattern holds true between the years under analysis.

Figure 8. Intensity of Rural Credit Use, 2002 and 2018

Note: The data refer to the ratio of the Volume of Rural Credit and Gross Value Added of agriculture by municipality. The intervals in the maps were defined based on the observed quintiles of this ratio in 2018. The municipalities painted in white had zero amount of credit or it was impossible to determine the amount borrowed from the database. Amounts deflated by the IPCA, using December 2020 as reference.

Source: CPI/PUC-Rio with data from IBGE and from RECOR and SICOR from Central Bank of Brazil, 2021.

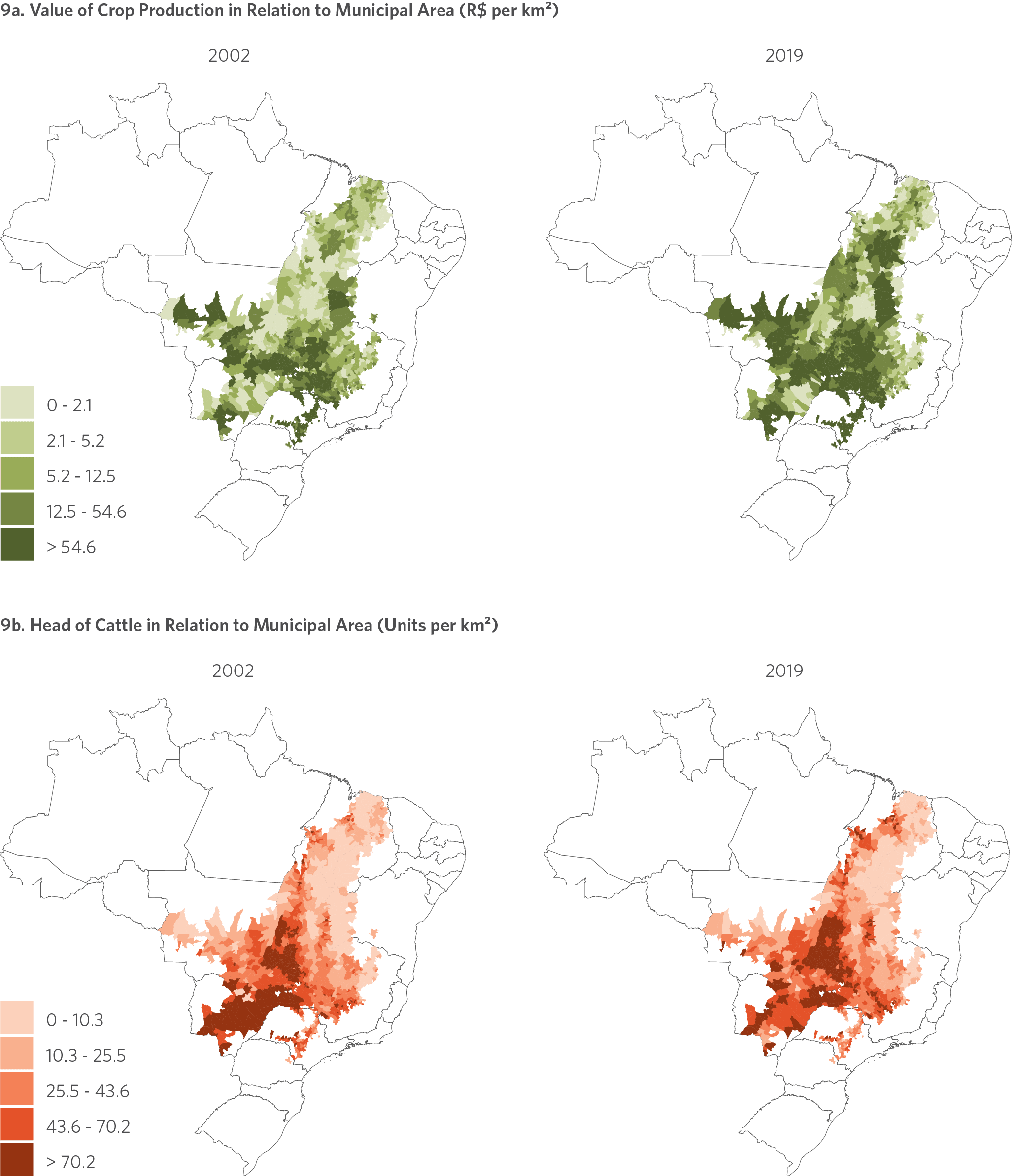

BOX 3. The Geographical Evolution of Production in the Cerrado

Figure 9 shows the intensity of agricultural production at the municipal level in 2002 and 2019. Figure 9a shows the distribution (by municipality) of the ratio between the value of crop production and the area of each municipality. Figure 9b shows the ratio between the head of cattle and the area of each municipality. Between 2002 and 2019, there was an increase in the value of crop production per area, especially on the border between Goiás and Minas Gerais, and in a good part of the border regions of the states that make up MATOPIBA. It is the opposite for cattle. The scenario is quite similar between the years and, in some regions (e.g., Mato Grosso do Sul), the number of cattle per area has declined.

Figure 9. Intensity of Agricultural Production in the Cerrado, 2002 and 2019

Note: December 2020 constant values (inflation adjusted by IPCA).

Source: CPI/PUC-Rio with data from IBGE’s Produção Agrícola Municipal (PAM) and Pesquisa da Pecuária Municipal (PPM), 2021

4. CREDIT USE AND BORROWERS

The bigger properties and the higher average value of rural credit contracts in the Cerrado do not translate into greater participation of corporations in the biome’s rural credit market. In the 2019/20 agricultural year, 99% of the number – and 85% of the amount – of credit operations in the Cerrado were directed to individuals (Figure 10). For the rest of the country, the statistics are 99.6% and 73%, respectively. The greater representation of corporations in the total amount of transactions compared to their share of the number of contracts reflects a higher average value of rural credit contract for corporations.

Figure 10. Number of Contracts and Rural Credit Volume by Producer Type in the Cerrado and Other Biomes, 2019/20

CERRADO

OTHER BIOMES

Source: CPI/PUC-Rio with data from SICOR from Central Bank of Brazil, 2021

Most rural credit in the Cerrado is directed toward working capital and investment (Figure 11), which is also the case elsewhere in the country. These two uses together accounted for 98% of the number – and 88% of the amount – of contracts in the biome in the 2019/20 agricultural year. When these numbers are broken down, credit used for investment accounted for 58% of the number and 25% of the amount of contracts in the Cerrado – numbers very close to the average for the rest of the country.

Figure 11. Number of Contracts and Rural Credit Volume by Credit Type in the Cerrado, 2002/03 – 2019/20

11a. Number of Contracts

11b. Rural Credit Volume

The statistics for credit used for working capital, on the other hand, are slightly divergent. In 2019/20, the credit used for this purpose accounted for 41% of the number of Cerrado contracts (compared to 43% in the rest of the country) and 63% of the credit amount in the municipalities located in the biome (compared to 53% in the rest of the country). Thus, though the working capital purpose may be similar in terms of the number of contracts, the credit amount used for this purpose is proportionally higher for the Cerrado.

This difference is offset by the lower share of the amounts of credit used for commercialization and industrialization purposes,[21] which are typical of a more business-oriented agriculture. In 2019/20, 1% of the number – and 10% of the amount – of contracts in the Cerrado were intended for commercialization purposes. Elsewhere in the country the numbers were 1% and 13%, respectively. Credit for industrialization accounted for 0.05% of the number – and 2% of the amount – of contracts in the Cerrado, compared to 0.1% and 8% in the rest of the country.

5. CREDIT DISTRIBUTION CHANNELS

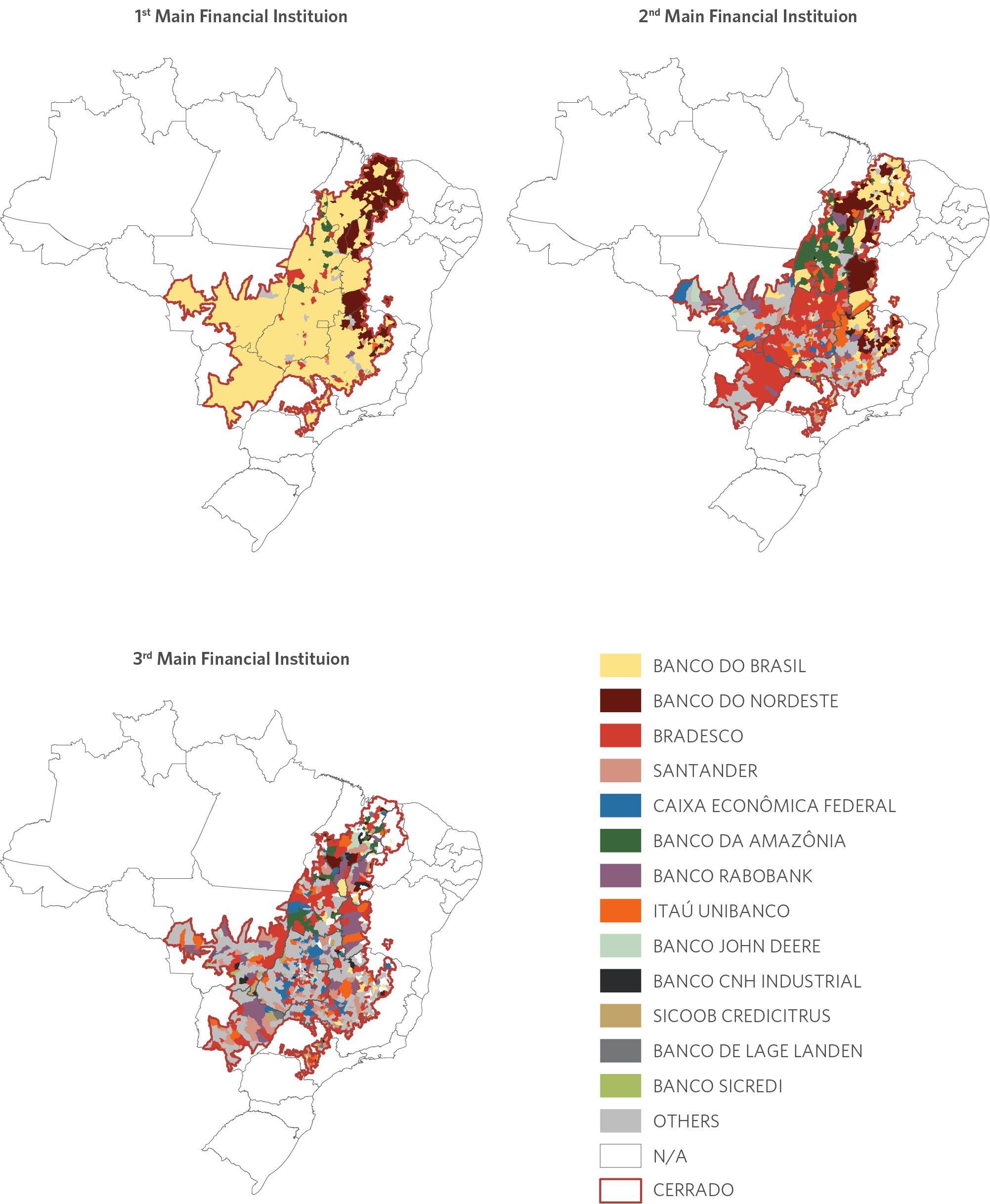

The share of public banks in the Cerrado rural credit market is considerably higher than that of private banks. Figure 12 shows the three main financial institutions offering rural credit in each Cerrado municipality, defined as those that lend the largest volume of credit locally. Overall, competition in rural credit markets is low in the Cerrado, much like in the rest of Brazil.

Figure 12. Main Rural Credit Provider by Municipality in the Cerrado, 2019/20

Note: The main financial institutions are defined as those that lend the highest volume of credit in each municipality.

Source: CPI/PUC-Rio with data from SICOR from Central Bank of Brazil, 2021

In most municipalities, the main credit provider is Banco do Brasil. Banco do Nordeste and Bradesco are also relevant, despite being the main credit provider in only a significantly smaller number of municipalities compared to Banco do Brasil.

Figure 13 shows that the competitive landscape has remained unchanged since the 2002/03 agricultural year, with the predominance of public banks. In 2019/20, Banco do Brasil was the main provider of rural credit in 757 municipalities, while Banco do Nordeste was the predominant provider in 197 municipalities, which means that one of these two institutions is the main credit provider for more than 90% of the municipalities of the biome. These same banks accounted for 50% and 5% (respectively) of the volume borrowed in that agricultural year.

Figure 13. Number of Municipalities and Share of Total Volume by Financial Institutions in the Cerrado, 2002/03 – 2019/20

13a. Number of Municipalities by Main Financial Institution

13b. Share of Credit Volume by Financial Institution

Source: CPI/PUC-Rio with data from RECOR and SICOR from Central Bank of Brazil, 2021

Bradesco is the largest lender in only 13 municipalities but is the second largest in 223 municipalities and the third largest in 195 municipalities. This explains Bradesco’s relatively high share of credit volume in the biome. In 2019/20, the bank was responsible for 7% of the total amount borrowed in the Cerrado. The other financial institutions accounted for the remaining 38%.[22] In any case, they do not enjoy the same degree of capillarity as the main prominent financial institutions, which prevents many producers from having access to competitors in the credit market. Promoting greater competition among financial institutions – through the creation of instruments to ensure greater participation by private banks and cooperatives – can improve the efficiency of the credit distribution system in the region.

The next section shows that there was a relevant increase in private funding sources for rural loans. However, public banks, especially Banco do Brasil and Banco do Nordeste, are still the main financial institutions in the provision of rural credit. Thus, there is room for an increase of private sector participation and for more banking competition in the region.

6. SOURCES OF RURAL CREDIT FUNDS

Despite the prevalence of public banks, the Cerrado stands out in terms of use of private and less subsidized funding sources. In the 2019/20 agricultural year, the three main sources of funds for rural credit in the Cerrado were Compulsory Resources, LCA, and Rural Savings – Unrestricted. Elsewhere in the country, Compulsory Resources also feature as the main source of funds, with Rural Savings – Restricted in second place and LCA in third.

The other relevant sources for the Cerrado are Rural Savings – Restricted and Unrestricted Resources. Constitutional Funds for the Northeast, Midwest, and North, on the other hand, are present in certain regions of the biome, but are of lesser importance for the biome as a whole.

Figure 14 shows that earmarked resources have been losing ground over time to private resources in the Cerrado. Compulsory Resources and Rural Savings – Restricted accounted for 43% and 21% of the credit value in the biome in 2002/03 and 25% and 13% in 2019/20, respectively. On the other hand, LCA (which did not exist in 2002/03)[23] and Rural Savings – Unrestricted – which accounted for 0.04% in 2002/03 – increased to 19% and 15% in 2019/20. In the rest of the country, the contribution of these two sources to the total value of rural credit increased from 0% and 0.05% in 2002/03 to 12% and 11% in 2019/20, in that order. The Cerrado has attracted more private resources for financing its agriculture than the rest of the country.

Figure 14. Evolution of Rural Credit Volume by Funding Source in the Cerrado, 2002/03 – 2019/20

Compulsory Resources are the first or second most relevant source of funds in terms of value in all states except Maranhão (where it is only the fourth biggest source). Constitutional Funds are the main source of funds for the Northern and Northeastern states located in the biome.[24] LCA is more relevant in the Midwest, Southeast, and South.[25]

7. RURAL CREDIT PROGRAMS

The most striking difference between the Cerrado and other biomes is the lower relevance of credit for small and medium producers (from PRONAF and, to some extent, also PRONAMP). In the 2019/20 agricultural year, PRONAMP, PRONAF and MODERFROTA – the three programs with the highest volumes – were responsible for, respectively, 13%, 4%, and 3.8% of the total amount of credit operations in the biome. In the rest of the country, loans associated with PRONAMP, PRONAF, and MODERFROTA accounted for 16%, 22%, and 3%, respectively.

It should be noted that most of the loaned amount (76% in the 2019/20 agricultural year) was not tied to a specific program. These loans are generally associated with larger producers. In the rest of the country, loans not linked to programs constituted 56% of the total amount in 2019/20. This difference is associated with significantly higher average contract values than in the rest of the country, as noted above. When credit is not linked to a program, the contract follows the rules and conditions of the source of funds.

An analysis of the temporal evolution in the Cerrado reveals a 12 percentage point increase in the participation of credit operations tied to PRONAMP between the 2002/03 and 2019/20 agricultural years. In 2019/20, PRONAF and MODERFROTA accounted for levels like those of 2002/03 (a variation less than one percentage point).

Public policy should focus on whether smaller producers have access to adequate financing for their operations. Previous studies by CPI/PUC-Rio show that when small and medium sized producers have better access to credit they intensify their production, leading to improved land use and less deforestation.[26]

Finally, it is important to note the growth of the National Program for Low-Carbon Emissions in Agriculture (Programa para Redução da Emissão de Gases de Efeito Estufa na Agricultura – ABC Program). In 2010/11, the first agricultural year in the program’s historical series, the amount borrowed in the Cerrado biome and linked to the ABC Program was R$ 19 million. By 2019/20 it had reached R$ 1 billion. As a result, in 2019/20 the ABC Program represented 1.5% of the total amount borrowed.

Figure 15. Evolution of Rural Credit Volume by Credit Line in the Cerrado, 2002/03 – 2019/20

The total amount of credit operations without a specific program is predominant across all states of the biome. Regarding contracts linked to programs, PRONAMP ranks first in the states of Bahia, Goiás, Mato Grosso, Mato Grosso do Sul, Minas Gerais, Paraná, São Paulo, and Tocantins. PRONAF takes the lead in the states of Maranhão and Piauí. MODERFROTA, in turn, is the number one such program in the Federal District; however, it accounts for only 4% of the total contracted amount, while contracts with no program attached account for 93% of the amount.

CONCLUSION

This brief examines rural credit in the Cerrado biome, adding depth to previous CPI/PUC-Rio analyses of credit at the national level and enabling a comparison with credit in the Amazon.[27]

Rural credit in the Cerrado has grown in recent years, and the average contracted amount is significantly higher than in the rest of the country. Thus, there has been a concentration of financial flows associated with the increase in soy production.

There is also a low volume of credit available for small and medium producers. Public policy should pay attention to the issue of credit access for small and medium-sized producers. Previous studies by CPI/PUC-Rio show that credit for these smaller producers is essential to achieving productivity gains in agriculture and reducing pressures on native vegetation.

The Cerrado has experienced an increase in private funds for credit, with an emphasis on LCA and Rural Savings – Unrestricted. Compulsory Resources and Rural Savings – Restricted, on the other hand, have seen a reduction in their participation in the total amount of operations, although they remain significant as credit sources.

Nonetheless, this increase in private resources has not yet had a significant impact with regard to the financial institutions that dominate credit distribution in the region. In recent decades, the predominant institution has been Banco do Brasil, followed far behind (i.e., at below 10% each) by Bradesco and Banco do Nordeste, showing that there is very little competition and limited options for rural producers. As such, there seems to be room for increasing the participation of the private sector and developing a more dynamic and less concentrated credit market.

Finally, native vegetation areas in the biome are shrinking with each passing year. With sustainability issues increasingly relevant to international markets and trade agreements, a more transparent and efficient credit policy can help preserve this biome. Access to credit must be directed to environmentally responsible producers who employ good land use practices and comply with the Forest Code, thus contributing to sustainable development. With all this, public policy should be able to generate incentives to promote economic and social well-being.

The authors would like to thank Solange L. Gonçalves, Eloiza R. F. de Almeida, and Nathalia Lima de Oliveira for research assistance, Natalie Hoover El Rashidy, Giovanna de Miranda, and Jennifer Roche for the editing and revision of the text, Nina Oswald Vieira and Matheus Cannone for formatting and graphic design and Meyrele Nascimento for editing the website and interactive graphics.

[1] The definition of the Cerrado biome uses the smallest geographic units in Brazil’s territory: the municipalities. Although a municipality may span different biomes, the classification scheme used in this paper is based on municipalities’ predominant biomes. That is, municipalities are placed in the Cerrado category if most of their territories are composed of this biome. According to this definition, the Cerrado biome spans a total of 1,062 municipalities.

[2] MAPA. AGROSTAT – Estatísticas de Comércio Exterior do Agronegócio Brasileiro. bit.ly/3j8T5Vs.

[3] ME. COMEX STAT. bit.ly/3zOgRvQ.

[4] INPE. PRODES Cerrado. bit.ly/3gOtShj.

[5] Souza, Priscila et al. 6 Peculiarities of Rural Credit in the Amazon: New Research Shows Credit Restrictions and Extensive Land Use in Agriculture. Rio de Janeiro: Climate Policy Initiative, 2021. bit.ly/3kdxUlC.

[6] Assunção, Juliano and Priscila Souza. The Impacts of Rural Credit on Agricultural Outcomes and Land Use: An Analysis by Credit Lines, Producer Types and Credit Uses. Rio de Janeiro: Climate Policy Initiative, 2020. bit.ly/3wCgn9s.

[7] Agricultural Credit Notes is an instrument offered by public or private financial institutions for their clients to invest. Of the total collected, 35% should be applied in rural credit, financing the agricultural sector. These resources are not linked to any program. Regarding Rural Savings, three institutions follow the rules for Rural Savings: Banco da Amazônia, Banco do Nordeste, and Banco do Brasil. For these banks, it is mandatory to keep 59% of the rural savings deposits applied to rural credit for a year. Most of the funds are offered at subsidized interest (Rural Savings – Restricted) and a small portion at free interest (Rural Savings – Unrestricted).

[8] Central Bank of Brazil. Sistema de Operações do Crédito Rural e do Proagro (SICOR). bit.ly/3em1xNX.

[9] Central Bank of Brazil. Sistema de Registro Comum de Operações Rurais. bit.ly/3hFABe0.

[10] Central Bank of Brazil. Sistema de Operações do Crédito Rural e do Proagro. bit.ly/3em1xNX.

[11] Compulsory Resources consist of 27.5% of deposits in checking accounts collected during the period of one year by Brazilian financial institutions.

[12] All figures in this report were deflated by the Extended National Consumer Price Index (Índice Nacional de Preços ao Consumidor Amplo – IPCA) and are shown in constant December 2020 prices.

[13] IBGE. Produção Agrícola Municipal. 2019. bit.ly/3yuDPYe.

[14] IBGE. Pesquisa da Pecuária Municipal. 2019. bit.ly/346Szi9.

[15] MapBiomas. Cobertura de Estados & Municípios (V2). 2019. bit.ly/3iGk4HP.

[16] EMBRAPA (Empresa Brasileira de Pesquisa Agropecuária) defines MATOPIBA as the region formed by the state of Tocantins and parts of the states of Maranhão, Piauí and Bahia, where there has been strong agricultural expansion since the late 1980s, especially in grain production. Of the 228 municipalities that make up MATOPIBA, 196 belong to the Cerrado biome. In this report, analyses referring to MATOPIBA cover only this smaller subset of municipalities.

[17] Throughout this report, the biomes grouped together as “Other Biomes” include Amazon, Caatinga, Atlantic Forest, Pampa and Pantanal.

[18] Ratio between the total area of agricultural establishments (in hectares) and the number of producers.

[19] IBGE. Censo Agropecuário. 2017. bit.ly/3oKt2ow. The reference period used in the 2017 Agricultural Census ranges from October 01, 2016, to September 30, 2017.

[20] States not included in the table do not have municipalities in the Cerrado biome. Data on Gross Value Added of Agriculture are available until 2018.

[21] According to the Rural Credit Manual (Manual de Crédito Rural), the purpose of commercialization credit is to provide rural producers or their agricultural cooperatives with the resources necessary to commercialize their products on the market. Credit for industrialization is intended for rural producers or cooperatives seeking to industrialize agricultural products, provided that, at least, 50% of the production to be processed is produced by the company itself (or by associates).

[22] Among them is Santander, with 4.7% of the total amount borrowed in the biome, and Caixa Econômica Federal, with 3.7%.

[23] The LCA was created in 2004, and its contribution only became non-negligible as of the 2014/15 agricultural year, when it accounted for 0.7% of rural credit funds in the Cerrado and 0.4% elsewhere in the country. The share of this particular source of funds increased significantly in the following agricultural year, reaching 7% and 9% in the Cerrado and the rest of the country, respectively.

[24] Tocantins, Bahia, Maranhão, and Piauí.

[25] Federal District, Goiás, Mato Grosso, Mato Grosso do Sul, Minas Gerais, São Paulo, and Paraná.

[26] Assunção, Juliano and Priscila Souza. The Impacts of Rural Credit on Agricultural Outcomes and Land Use. Rio de Janeiro: Climate Policy Initiative, 2020. bit.ly/3i94BOs.

[27] Souza, Priscila et al. 6 Peculiarities of Rural Credit in the Amazon: New Research Shows Credit Restrictions and Extensive Land Use in Agriculture. Rio de Janeiro: Climate Policy Initiative, 2021. bit.ly/3kdxUlC.