From Banks to Capital Markets: Alternative Investment Funds as a Potential Pathway for Refinancing Clean Energy Debt in India

Clean energy must play a central role in achieving India’s green growth goals. The IFC estimates India will need $450 billion to finance its 2030 clean energy targets (IFC 2017). Assuming a typical 70-30 split of financing via debt vs equity, the debt funding requirements translate to $315 billion through 2030.

While India’s clean energy sector continues to grow and attract significant investment, there can be serious challenges to the growth trajectory, if the capital deployed in existing projects is not recycled and if new sources of capital are not included to meet the increased future investment requirements (Pragathi and Veena, 2018). It is, therefore, imperative that operational renewable energy projects access capital markets to recycle capital and attract new investor classes.

This study, produced by Climate Policy Initiative under the US-India Catalytic Solar Finance Program (USICSF), and as a knowledge partner with the Indian Renewable Energy Development Agency (IREDA), looks at various avenues for renewable energy to access capital markets.

We show that shifting project debt to capital markets can be primarily achieved via two pathways:

- Financial institutions such as banks and NBFCs shift diversified loan portfolios to capital markets by converting pools of regular cash flows into investable financial securities, via a process known as securitization.

- Alternatively, developers directly go to capital markets, and use the proceeds to retire existing loans.

These paths are common in economies with more developed capital markets, however, in India, barring a few sporadic transactions, both pathways are yet to take off in any substantive manner. We therefore suggest specific solutions that would help to address some of the main barriers in the medium and longer term. These include:

- Greater investor protection in case of default to increase demand for the lower-rated securities and help deepen the bond market

- Development of risk-transfer mechanisms, for example Credit Default Swaps (CDS), that would also help increase demand for bonds

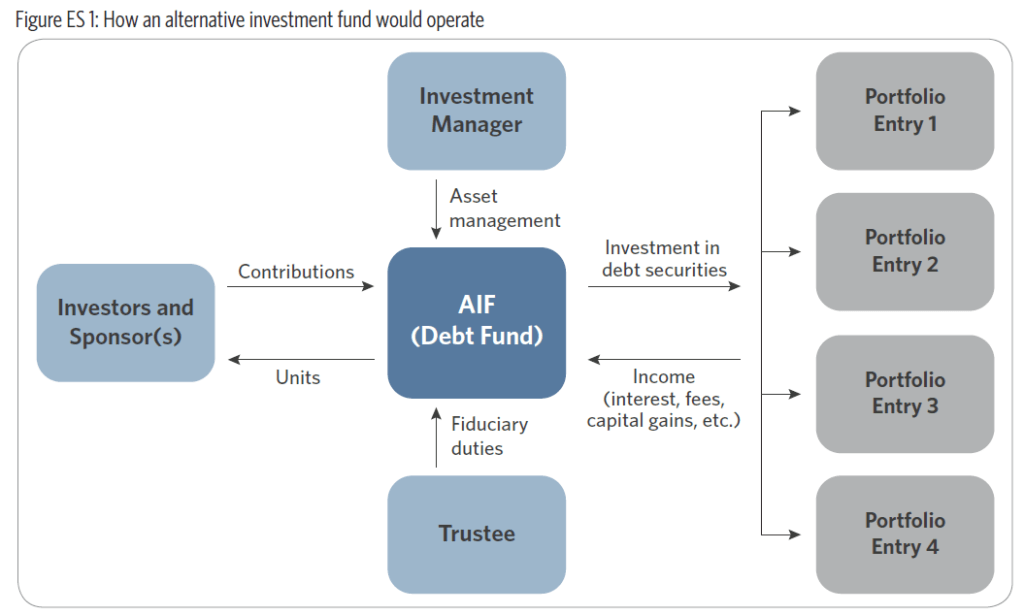

In addition, our research shows that Alternative Investment Funds (AIFs) offer the best near and medium-term path to expanding renewable energy access to capital markets while more structural issues are addressed.

AIFs are essentially managed pools of money that can invest in a pre-specified mandate. As the name suggests, AIFs are alternatives and can deploy investment strategies that are beyond the purview of the more commonly deployed pathways such as mutual funds – e.g. investing in startups/unlisted companies, deploying leverage and complex trading strategies, etc. Through participation of institutional investors, an AIF allows investment in debt securities issued by renewable energy project developers, which are backed by cashflows from stable and operational projects. The proceeds from bond issuances can then be used to retire loans that the developers would have taken from banks/NBFCs.

While AIFs may not fully address the structural issues prevalent in the Indian capital markets, they may partially resolve or help to circumvent some of these barriers, such as, by:

- Enhancing the credit rating of the structured bond issuance: In cases where the sponsor of an AIF for renewable energy is able to directly provide a partial credit guarantee, the ratings of the bonds may see an improvement as well, which can attract the interest of institutional investors. This possibility, would for example, be in play if IREDA were to sponsor an AIF. Alternatively, it would be possible to credit enhance at the level of the AIF through other sources of credit enhancements (e.g., balance sheets) available to the sponsor.

- Creating scale through aggregation of renewable energy projects loans: A financial institution like IREDA could bundle multiple projects and increase the size of issuance. The same aggregation could also be possible at the level of AIF for upstream investment.

- Crowding in long-term institutional investors: AIFs, by regulation, cannot invest more than 25% in a single security; this by definition requires other investors in the project. With an anchor sponsor (e.g. IREDA), however, a project may be able to attract more institutional investors, create better credit enhancement structures, and increase the scale of placement relative to an individual project.

Further, AIFs appear to be the most flexible of similar instruments (e.g., INVITs and IDFs) and, therefore, are likely to be more successful in taking renewable projects to capital markets.

This study recommends that potential sponsors work toward a next step of a demonstration AIF focused on renewable energy debt. Such a project – particularly if offered by a public agency like IREDA – could provide useful demonstration effects, and create track record to build investor confidence about the economic viability of clean energy projects, offering potential for further replication of this model.