Climate finance in China – can adaptation investment mirror the successes of mitigation finance?

Against a backdrop of more frequent and intensifying climate hazards, investment in adaptation is critical for sustainable economic growth. China offers a compelling example. The world’s second-largest economy, also categorized as the largest developing country, is increasingly exposed to a diverse and overlapping range of climate hazards. Without sufficient finance for adaptation, climate risks threaten China’s long-term growth and prosperity (World Bank), hindering the contributions that mitigation and clean energy have made to its GDP (Carbon Brief). China has the opportunity to lead internationally by translating its strong foundation of national strategies, plans, and policy priorities into adaptation finance, both domestically and overseas.

Various natural disasters caused China direct economic losses of approximately USD 58 billion in 2024 (Ministry of Emergency Management), before accounting for difficult-to-quantify social and indirect costs. These losses underscore the urgent need to scale up adaptation action and financing in China.

To date, the narrative framing China’s climate finance has been one of mitigation success. Solar PV capacity has increased 5-fold since 2018 (IRENA), whilst battery electric vehicle car sales have increased nearly 8-fold over the same period (IEA). This is reflected in CPI’s tracked climate finance—the country accounted for 37% of global mitigation flows in 2023. China’s recent 15th Five-Year Plan shows a particular focus on carbon intensity reduction and continued clean energy roll-out, while recent data shows China’s CO2 emissions have been ‘flat or falling’ for 21 months (Carbon Brief). But China only represents 10% of adaptation flows in 2023 (GLCF).

This blog spotlights China’s adaptation opportunity. Having built a robust enabling environment, where resilience is increasingly integrated across national plans and frameworks, China is well-positioned to scale adaptation investment. The 15th Five-Year Plan reinforces this direction at a high-level, calling for the refinement of China’s adaptation framework and enhanced resilience (The People’s Republic of China). The opportunity now lies in translating ambition into progress: can national strategies, taxonomy expansion, and the integration of resilience into high-level policy ambition propel adaptation finance growth?

1. China’s need for adaptation action

China faces a wide range of climate hazards that pose significant risks to public health and safety, the stability of national infrastructure, and the resilience of key industries that underpin the country’s export-led growth. The strength of China’s trade links means that these risks also cascade across borders.

China experienced unusually warm and wet conditions as well as more frequent extreme weather events in 2024 (Ministry of Ecology and Environment). Similar anomalies persisted in 2025, with China’s average temperature tying the previous year’s record as the highest in history (CMA).

Provinces in Northern and Western China are particularly vulnerable to more frequent heatwaves and droughts, intensifying water insecurity and pressure on agricultural systems (World Bank). In 2024, droughts damaged 1.2 million hectares of crops, resulting in USD 1.2 billion in direct damages (Ministry of Emergency Management). In South China, pre-flood season precipitation in 2024 was 40% higher than normal, while the North experienced a rapid shift from drought to flooding mid-year. Floods and related disasters alone in 2024 led to direct economic losses of approximately USD 38 billion (Ministry of Emergency Management).

Rising sea levels, storm surges, as well as coastal flooding and erosion threaten densely populated, low-lying coastal cities. Around one-fifth of China’s population lives in these coastal cities, which generate a third of the country’s GDP (World Bank). Without adequate adaptation expenditures, China could face some of the world’s biggest economic losses from rising sea levels and flooding (IPCC), with estimates suggesting impacts of up to 2.3% of GDP by 2030 (World Bank).

Integrating adaptation into planning can accelerate the adaptation-development ‘triple dividend’ of: (1) avoiding loss and damage; (2) preserving economic growth and benefits; and (3) ensuring social and environmental protection (WRI). This is both a domestic opportunity to safeguard growth and an international opportunity as demand for resilient infrastructure rises.

The opportunity represented by the ‘triple dividend’ comes into sharper relief when considering China’s mitigation progress. As well as direct economic losses and damages, climate change detrimentally impacts the productivity of mitigation assets: flooding and droughts impede hydropower, cold snaps negatively affect turbine blades, and wind power can drop in hot, stagnant conditions (WEF).

2. Key national adaptation plans and strategies

China’s adaptation policy architecture has expanded significantly in recent years. The National Strategy for Climate Change Adaptation (2013)—China’s first national adaptation framework—established guiding principles and adaptation objectives through to 2020. Distinct strategies for urban, agricultural, and ecological zones were proposed, and the need to form regional adaptation units that align with national plans was outlined (ADB), covering provinces, cities, and national agencies.

The National Strategy for Adaptation to Climate Change 2035 (2022) establishes China’s most comprehensive blueprint to date, with targets and timelines running to 2035 that cover key areas such as climate resilience in cities and ecosystem restoration. The plan also includes year-specific ambitions across forecasting, risk assessment, and early warning systems. Annual Progress Reports track progress toward these goals. As of 2024, 24 provinces had developed provincial action plans, and 80 national policies addressing 12 dimensions of adaptation had been issued (Climate Corporation China).

Progress reports provide overviews of developments in key areas such as water management, flood control, early warning systems, agriculture, and public health (Climate Cooperation China 2023, 2025). A robust progress assessment framework can, in theory, identify financing gaps and drive timely action.

Dedicated action plans toward early warning, risk monitoring, and the intersection between climate adaptation and health were also released in 2024 (Figure 1). The Action Plan on Early Warning for Climate Change Adaptation (2025-2027) embeds South-South cooperation and knowledge sharing with developing countries.

Figure 1: Inexhaustive timeline of China’s key national adaptation strategies and reports

Five-Year Plan cycles set out China’s high-level economic and industrial priorities. The 14th plan, released in 2021, references strengthening the observation and assessment of climate change impacts, and increasing adaptive capacity (Climate Change Laws). The recent 15th Five-Year Plan places strong emphasis on a new carbon intensity target and continued clean energy scale-up, but also references refining frameworks on adaptation and enhancing resilience (The People’s Republic of China). The implementation of high-level objectives occurs in forthcoming sectoral and provincial plans, and how adaptation will be translated into these remains to be seen.

Beyond national plans, green financial reform is the main channel for mobilizing resources toward national priorities. The People’s Bank of China (PBoC) has led green finance policies since 2014 (CPI), creating much of the architecture that enabled China’s mitigation progress. In 2025, a new catalogue of green finance-supported projects unified and expanded the country’s eligible activities (The People’s Republic of China), broadening the scope of China’s green finance taxonomy. The updated catalogue includes activities related to climate resilience (CBI), though clear labelling and expanded coverage remain important next steps (Carbon Brief). Advancing resilience in finance taxonomies can provide clarity for potential investors, helping to address challenges in identifying and classifying adaptation actions and highlighting investable opportunities to address climate risk.

3. The state of China’s climate finance—and why adaptation tracking matters

a. Domestic adaptation finance

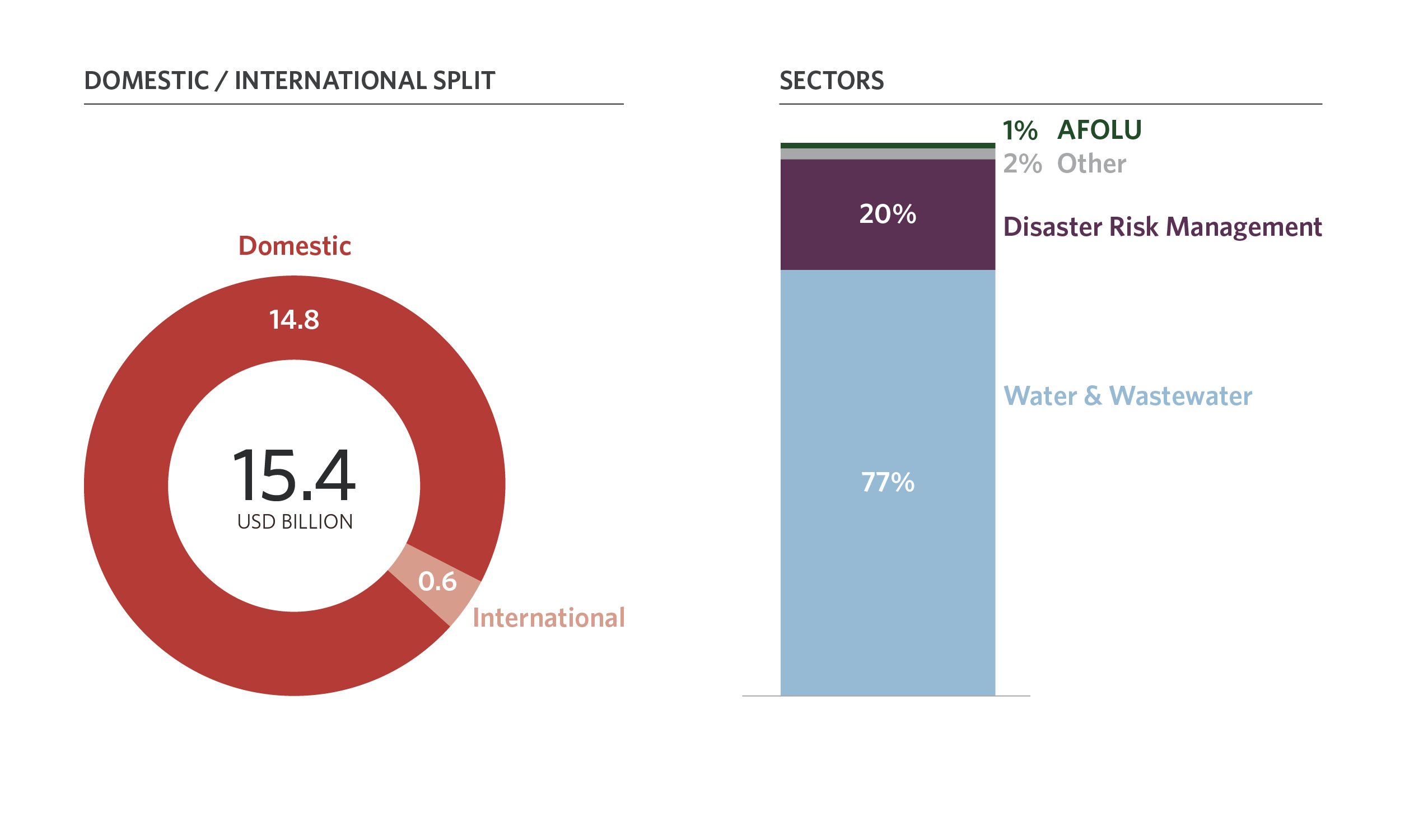

Despite challenges in tracking adaptation finance, available data shows that from 2018 to 2023, annual adaptation investment flowing within China averaged USD 15.4 billion. The sectoral destination of this tracked finance aligns with the previously identified policy priorities of Water and Wastewater and Disaster Risk Management (DRM) investment (Figure 2). Water and Wastewater solutions have dominated adaptation finance in more recent years (90% from 2021-2023), while DRM investment was more concentrated from 2018 to 2020. Agriculture, Forestry and Other Land Use (AFOLU), another key policy priority, is less reflected in tracked adaptation finance (GLCF).

Figure 2: Adaptation finance to China, 2018-2023 annual average, USD billion

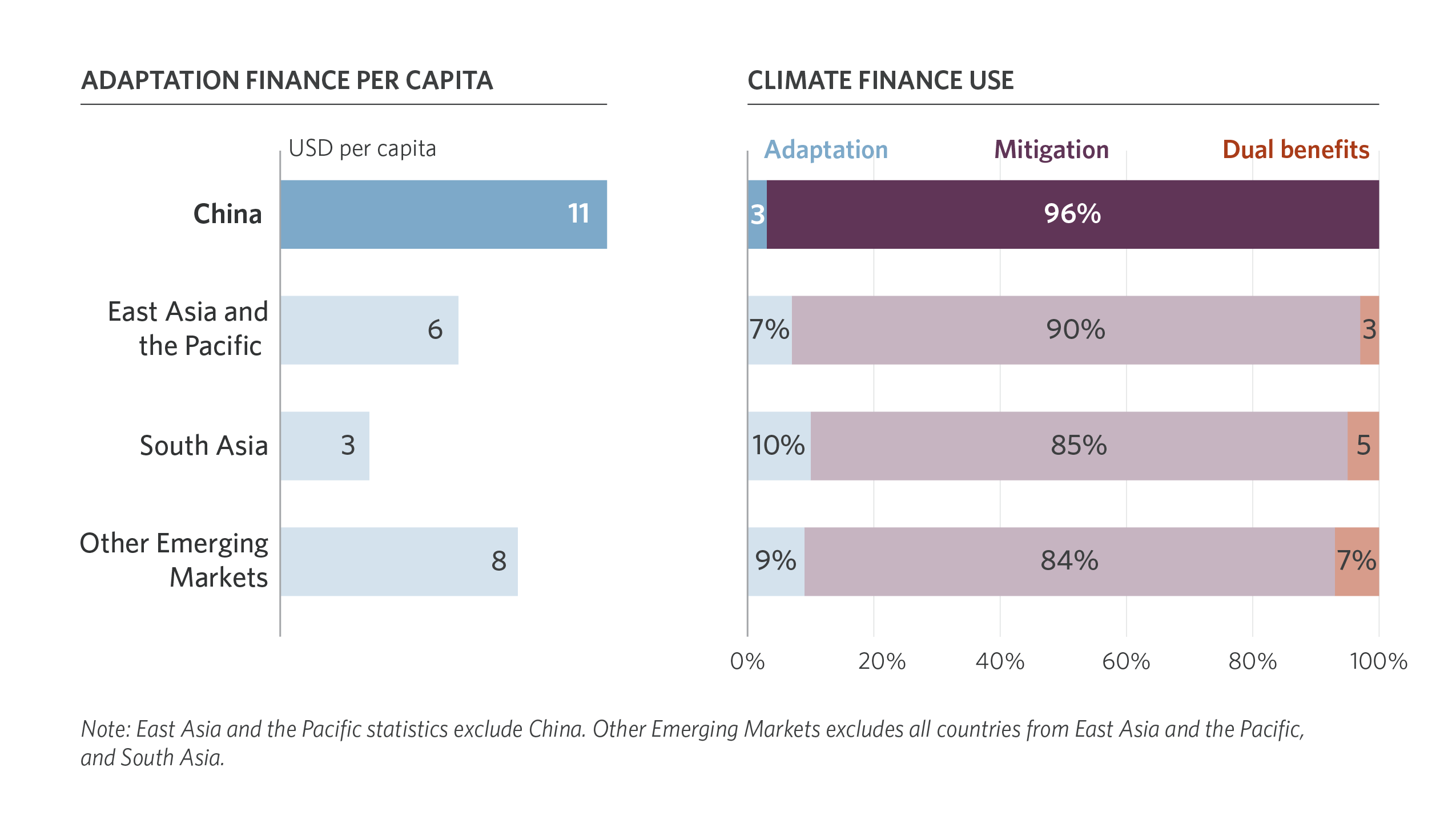

Tracked flows show China at a much higher level of adaptation finance per capita than neighbouring regions and Other Emerging Markets (Figure 3). This is despite South Asia and the rest of East Asia and the Pacific facing higher average vulnerabilities (ND-GAIN), and adaptation finance accounting for just over 3% of China’s total climate finance.

Figure 3: Adaptation vs mitigation finance, China vs. regional peers and other emerging markets, 2018-2023.

b. China’s international mitigation and adaptation finance

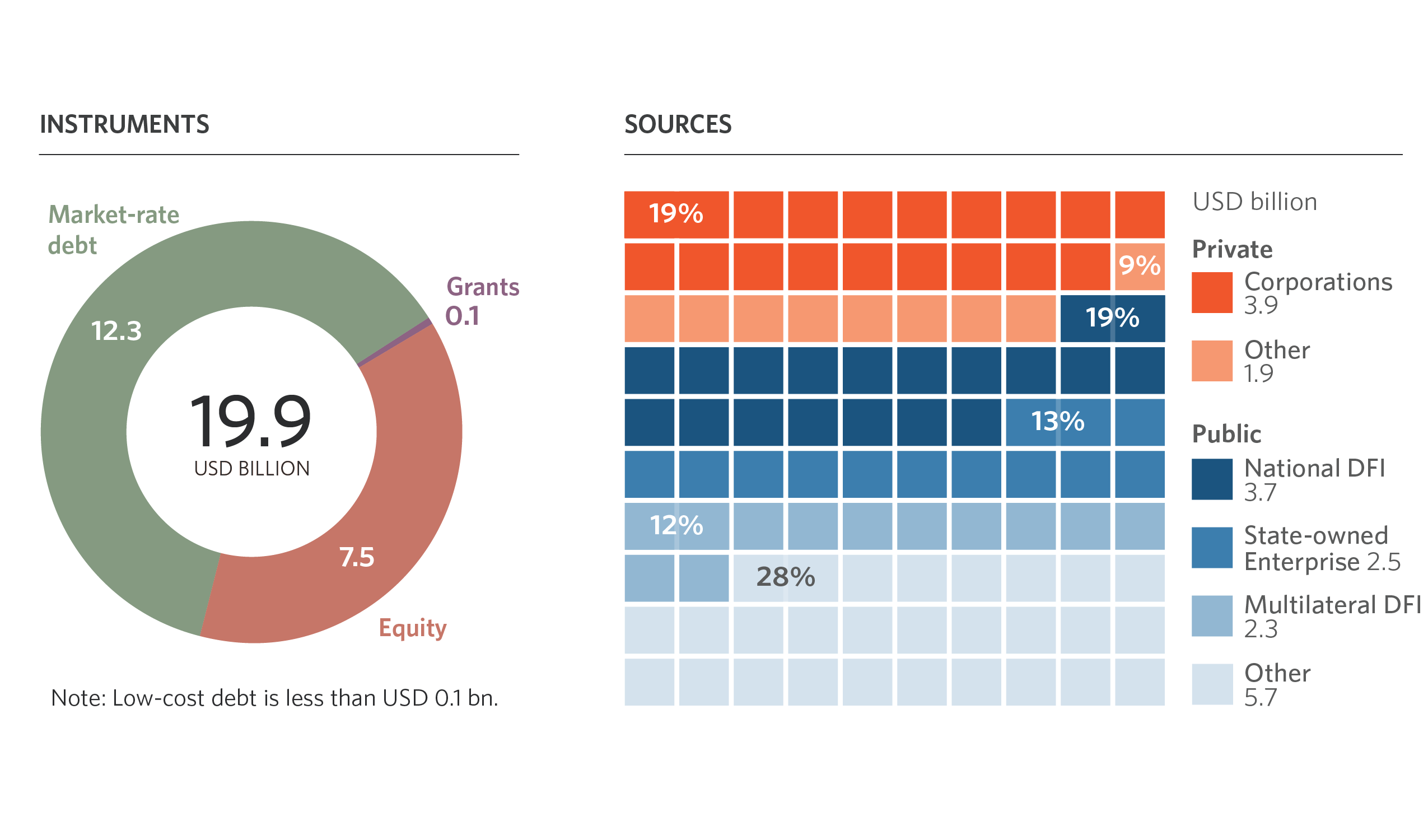

In addition to domestic investment, between 2018 and 2023, China provided USD 20 billion in ‘South-South’ flows – this is climate finance flowing between emerging markets and developing economies (EMDEs), including China. South-South flows shown in Figure 4 include both mitigation and adaptation projects—tracked international adaptation finance originating from China is minimal. China’s flows to other EMDEs were primarily for Energy Systems (USD 14 billion), Transport (USD 3 billion), and Buildings and Infrastructure (USD 1 billion).

Figure 4: South-South finance originating from China, 2018-2023, USD billion

China is playing a growing role in international financing—its share of tracked South-South flows has increased from 17% in 2018 to 25% in 2023, during which it provided USD 6.5 billion. South-South flows are already a significant source of finance for climate transition in EMDEs and are set to grow in importance in future years. The recent 15th Five-Year Plan showcased China’s willingness to steer climate governance on clean energy technology (Carbon Brief), and there is also a huge opportunity for adaptation finance in this sector. The integration of resilience into mitigation investments can ensure that the assets, services, and workforces needed to drive the low-carbon transition in partner countries remain resilient to climate hazards. This can strengthen development outcomes in partner countries, safeguarding critical energy, transport, and infrastructure projects. Additionally, expanding the provision of dedicated adaptation projects can directly address the growing international need for adaptation finance.

c. The importance of tracking

While adaptation is embedded in China’s development objectives, translating policy ambition into consistently tracked adaptation finance remains a challenge globally. Despite CPI’s Global Landscape being the most comprehensive database of adaptation finance to date, differences in definitions, methodologies, and reporting practices make it difficult to capture the complete scale and view of adaptation finance globally.

Strengthening transparency, data availability, and reporting allows for a more comprehensive picture of adaptation finance. A clearer landscape of national adaptation finance is crucial for policymakers. It also enables a wide range of actors to develop insights into how to prioritize investments, design effective interventions, and target resources toward the most pressing climate risks, thereby safeguarding lives and livelihoods. In turn, aligning domestic tracking with global adaptation frameworks, taxonomies, and goals presents international opportunities. For example, a recently proposed policy agenda explores potential EU and China collaboration on scaling adaptation finance—with key recommendations on shared definitions, incentives, taxonomies, and measurement frameworks (EU-China Cooperation).

4. China’s opportunity (and imperative) to build on adaptation progress

China’s national plans and strategies, growing articulation of adaptation priorities, and incorporation of resilience into green finance frameworks combine to form a strong enabling environment. The 15th Five-Year Plan further builds momentum for adaptation investment. Extending this internationally also provides an opportunity, where integrating adaptation into foreign direct investments can support climate-resilient growth in other EMDEs and meet a growing demand for adaptation solutions.

Adaptation finance is becoming a defining priority for global climate and development agendas. China is already demonstrating its ability to leverage ambitious policies to accelerate mitigation finance. The country now has an opportunity to translate its adaptation frameworks into finance at scale. Achieving this could help to safeguard its own development and that of international partners. It can also demonstrate a context-specific path to success that may generate lessons for other climate-vulnerable countries seeking to integrate resilience into national growth strategies.