Uncovering the Private Climate Finance Landscape in Indonesia

Climate finance in Indonesia is falling far short of the need.

Indonesia needs an estimated USD 247 billion by 2030 to meet its NDC target of reducing greenhouse gas emissions by 29%. However, research from Climate Policy Initiative (CPI) tracked only about USD 13.2 billion of private climate finance between 2015-2018, highlighting Indonesia’s need to significantly scale up climate finance in the next ten years to achieve its NDCs. This analysis comes at a time when financial institutions, listed companies, and public companies will start reporting the sustainable aspects on their portfolios by 2021, as mandated by the POJK 51/2017 regulation issued by the Financial Services Authority (OJK).

These estimates are a follow-up to a previous CPI report on Indonesia’s public climate finance, where we found that at least USD 951 million of climate finance from public sources was disbursed in Indonesia in 2011. The analysis was instrumental in supporting the Ministry of Finance’s efforts to develop a climate finance budget tagging system.

CPI’s upcoming study, Uncovering the Landscape of Private Climate Finance in Indonesia, is aimed at developing a first-of-its-kind approach for tracking private climate finance in Indonesia. For the study, we collected data from different investor categories including, but not limited to, financial institutions, project developers, corporations, domestic philanthropies, and impact investors, supplementing it with publicly available data.

Through our research, we’ve identified 5 preliminary trends in climate finance in Indonesia:

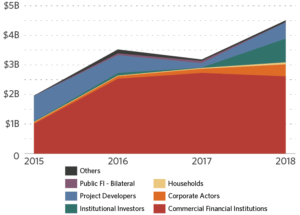

- Total climate finance from the private sector reached USD 13.2 billion between 2015-2018, with commercial financial institutions (FIs) accounting for a majority (67%) of this. However, this only accounts for 2.3% of commercial FIs’ total credit issuance (USD 378 billion), highlighting the big chasm between their total financing compared to their climate financing.

- Debt financing continues to be preferred mode of lending, accounting for 71% of total financing, or USD 9.4 billion. However, the amount of debt financing on climate investment has stagnated over the last two years (USD 2.7-2.8 billion per year), probably due to policy amendments on renewable energy (RE) use. The latest regulation from the Ministry of Energy and Mineral Resource (no.50/2017) is putting all RE projects in development under the BOOT scheme, and in direct pricing competition with coal-fueled power plants. As a result, many RE developers found it difficult reach financial closing, despite having secured the power purchase agreement with PLN (Indonesia’s national utility company).

- The distribution of private finance is skewed towards renewable energy projects, reflecting the appetite for increased private sector involvement in the renewable energy market, especially in small hydro and geothermal power plants, which are perceived to be less risky.

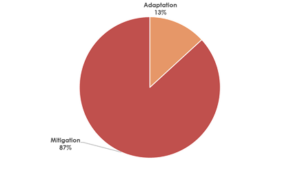

- Private finance flows to adaptation remains limited (USD 1.7 billion) despite tremendous potential economic value, as these sectors are traditionally considered as “government responsibility.” For instance, improvement in coral reef state by 2030 could unlock an additional value of USD 37 billion (or USD 2.6 billion per annum) in Indonesia (Coral Reef Economy, UNEP, November 2018) but investments in agriculture, forestry, land use and natural resource management were reported at less than a billion between 2015-2018.

- The current private philanthropy fund in Indonesia, which is disbursed almost exclusively in the form of grants, has been playing a large role in climate activities currently uncovered by private finance. This includes technical assistance and grassroots community engagement in forestry, land-use, natural resource management, coastal protection, and disaster management. The private, philanthropic climate fund has stagnated for the last three years, most likely due to its increasing focus on education and health.

Figure 1: Indonesia private climate finance by source in 2015-2018

Figure 2: Adaptation vs. mitigation projects financed by the private sector in 2015-2018

CPI and the OJK convened a workshop on December 19, 2019 to discuss the initial findings from our work tracking private climate finance. The event was attended by 51 participants from 27 different institutions including financial institutions, regulators, corporations, donors, philanthropies, and NGOs.

Key messages from the workshop included:

- There is lack of clarity on the definition and methodologies for tracking and reporting climate finance across various financial institutions, which makes the currently available data less accurate. This is particularly true for energy efficiency and adaptation investment projects, where the relevant investments are often components within larger projects, requiring additional information to know which private actors are unlikely to report voluntarily.

- Financial institutions are bound by various prudential and fiduciary duties to hold adequate capital and to maximize financial returns to their beneficiaries without taking excessive risks, while also meeting their liabilities over the long run. Given these institutions’ long-term portfolio exposure to climate risk (e.g. stranding of fossil fuel assets), there is clear need to ensure the disclosure of carbon footprints in their portfolios, and the integration of climate-related risks into the macro prudential regulations. These disclosure and risk management frameworks will give financial institutions a head start to gradually diversify from high carbon sectors, and to gradually rebalance their portfolio in favor of climate friendly investments.

- There is a need to explore the role of blended finance in unlocking and mobilizing more private finance in climate investments. The funds from philanthropies are mostly used in the form of grants to: support project preparation activities; develop project pipelines through technical assistance; and to design financial de-risking instruments. This type of funding can be used for innovative sustainable projects to leverage the profitability in order to meet the market rate expectations of private investors.

- Financial institutions and corporations need to share opportunities, successes, and failures in implementing SDG targets, including climate-related goals, to better identify which gaps can be covered by private and public actors.

- The scope of sustainable reporting should be expanded to consider Sharia-compliant bonds within the intermediation function (or financing to deposit ratio) as part of climate finance.

What’s next?

It is important to acknowledge that private climate finance tracking and reporting is instrumental in helping governments develop policies and regulations to mobilize finance, and to motivate the private sector to align with the overall national policy objectives.

CPI is currently collaborating with data providers, government agencies, and financial institutions to track public and private finance and optimize the impact of these investments on climate change. For instance, CPI’s team in Indonesia is currently helping the Fiscal Policy Agency (BKF) formulate NDC – related climate finance recommendations. The team is also providing technical assistance and advise for SMI – an operator of SDG Indonesia One Platform comprised of USD 2.3 billion in public and private funds for SDG – related infrastructure investment – on the development of innovative financial instruments for renewable and energy efficiency investment.