The Cost of Inaction

“Our world is a house on fire.”

evoked by many, including youth activist Greta Thunberg

The longer our home remains aflame, the harder and more expensive it will be to extinguish the fire and repair the damage.

Delaying climate action will inevitably increase the negative impacts that the world will experience due to climate change. Continued inaction will make achieving the 1.5°C goal of the Paris Agreement more and more costly, and eventually, completely out of reach.

The Inaction Price Tag

The fact that failing to act on climate change now will create greater costs in the future, or the cost of inaction, is well understood in climate circles. However, these costs can be difficult to quantify. Various studies suggest that current policies will lead to warming exceeding 3°C, causing staggering losses. However, projections of associated costs vary greatly.

Putting a price on each year of delayed climate action is critical for the public and decision-makers to understand the scope and urgency of the climate crisis. Concrete figures and projections can urge policymakers to act more effectively than metaphors of burning homes, and act as a rebuttal to the myopic idea that climate action is too expensive. In fact, inaction will be much more costly.

The two-year Global Stocktake for the Paris Agreement concluded at COP28 a few weeks ago and confirmed what we already knew: We are off track from the targeted 1.5°C pathway, and there is a “rapidly narrowing window” for increasing efforts in order to achieve the Paris Agreement goals. We need to increase investment in a net zero transition without delay (UNFCCC, 2023).

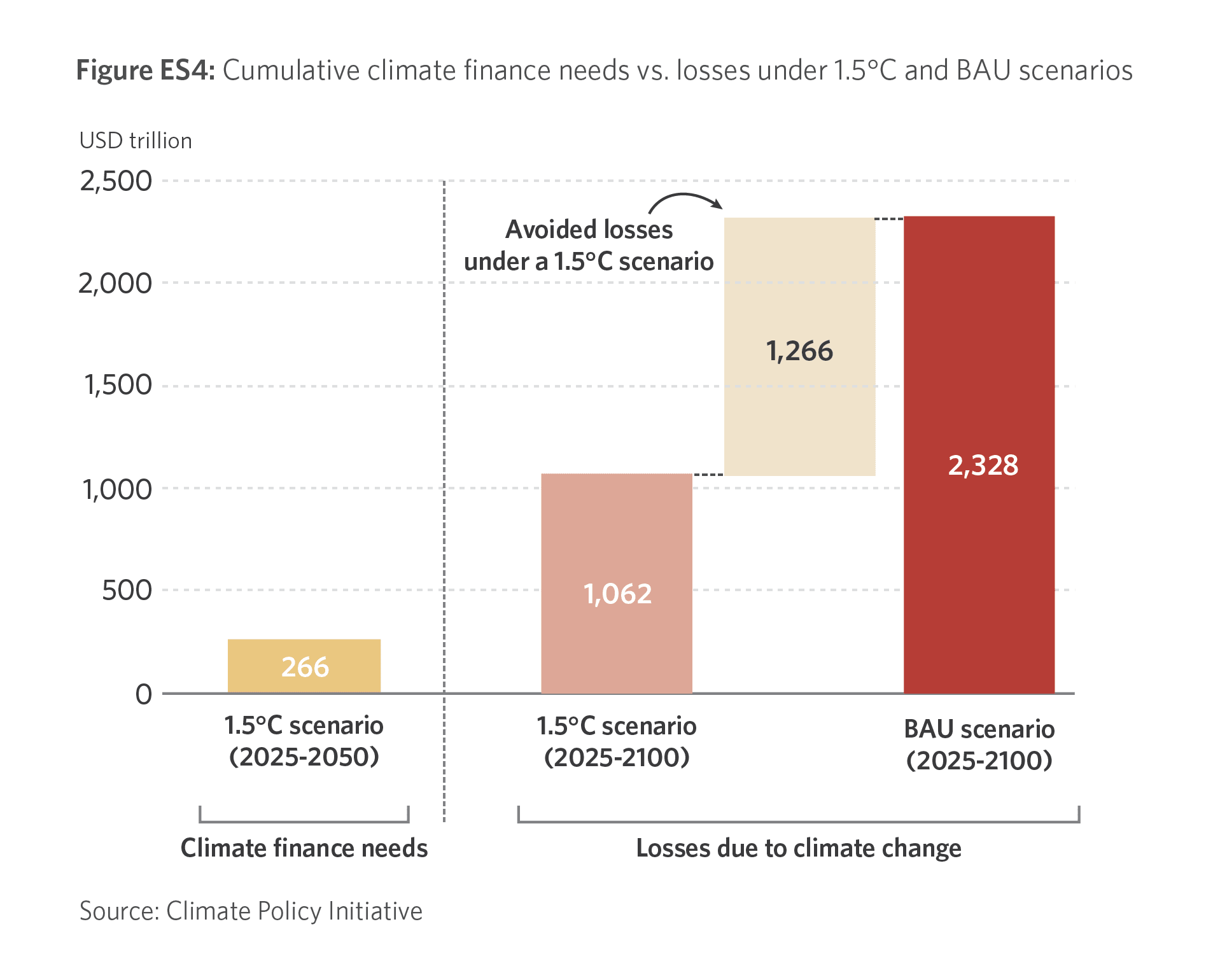

In 2021/2022, CPI tracked USD 1.3 trillion per year in global climate finance (CPI, 2023). Though this marks the largest volume of such flows to date, nearly double those of 2019/2020, we need to increase this amount by at least five-fold annually.

CPI estimates that climate finance needs to ensure global temperatures do not rise above 1.5°C range from USD 5.4 trillion to USD 11.7 trillion per year until 2030, and between USD 9.3 trillion and USD 12.2 trillion per year over the following two decades.[1] These needs are dwarfed by the increased social and economic costs that will be incurred under business-as-usual (BAU) warming scenarios (which CPI estimates to be at least USD 1,266 trillion) and will only worsen the longer action is delayed.

The house is on fire, and current efforts are akin to using a squirt gun where a water cannon is needed to douse the flames. And these costs will only grow as the planet gets hotter.

Estimating the Cost of Inaction

CPI’s estimate of USD 1,266 trillion for the cost of inaction is derived from modeling by the Network for Greening the Financial System.[2] However, existing cost of inaction estimates vary widely because different models are based on different costs, warming scenarios, and timeframes.

Broadly, costs of inaction fall into two categories:

- Economic costs: Direct losses to GDP due to climate-related risks and impacts, and

- Social costs: Indirect costs incurred due to negative climate-related impacts on people and/or their environments.

Although all the above aspects contribute to the cost of inaction, they are not all always included in modelling. Costs that are easy to quantify (e.g., damage to assets and losses due to reduced productivity) are often included in projections, while more challenging aspects (e.g., costs from loss of nature or costs of conflict and migration) may be omitted. The graphic below shows what costs each publication considers when modelling the cost of inaction. Click on the report authors in the graphic to see more information, including total estimated costs.

Quantifiable Costs of Inaction

We have a fairly good understanding of the direct economic losses from climate change impacts, such as increased temperatures, sea-level rises, and extreme weather events. For instance:

- Even a temperature rise of 1.5°C is projected to reduce global working hours by 2.2% worldwide by 2030, costing the global economy USD 2.4 trillion (ILO, 2019)

- Climate-related disasters (e.g., hurricanes, floods, wildfires) were responsible for USD 299 billion in economic losses due to damage to assets and capital in 2022 alone (Aon, 2022)

- Sea-level rises could add a further USD 400-520 billion per year in losses by 2100 under the most extreme warming scenarios (Depsky et al., 2022)

We are also able to quantify climate-related health costs, from rising temperatures and worsening air quality:

- In the U.S. alone, the health costs of air pollution and climate change far exceed USD 800 billion per year (NRDC, 2021).

- Globally, rising temperatures are projected to cause an additional 250,000 deaths per year between 2030 and 2050 from malnutrition, malaria, diarrhea, and heat stress alone (WHO, 2021). Developing countries and areas with weak health infrastructure will experience the worst effects.

These impacts all result in direct losses and will only increase in magnitude with each additional degree of warming. Because these losses are more easily quantified, they are usually included in projections of climate-related costs.

Quantifying the Unquantifiable

Other impacts, such as biodiversity, nature loss, and broader social costs like increased conflict and migration are more difficult, if not impossible to quantify. While we cannot put a true price on human suffering or loss of nature, it is useful to devise metrics to compare these costs to investment needs.

Nature and Biodiversity: The World Bank projects up to USD 225 billion in GDP losses by 2030 due to lost ecosystem services, such as pollination and the provision of timber and marine stocks (World Bank, 2021). However, uncertainty surrounding quantifying the costs of nature means that these costs are often excluded from most cost-of-inaction projections.

Broader Social Costs: Current cost-of-inaction estimates are also unable to capture broader social costs such as increased conflict and migration and worsening local and global inequalities. These costs are difficult to estimate given the uncertainty surrounding future warming.

The world is already experiencing increased climate-related drivers of conflict, such as food insecurity and water scarcity. The IEP (2020) projects that:

- The number of people with uncertain access to food will increase from 2 billion to 3.5 billion by 2050.

- The number of people experiencing high or extreme water stress will increase from 2.6 billion to 5.4 billion by 2040. Over the past decade, the number of recorded conflict and violent incidents related to water increased by 270% worldwide.

- More frequent and more intense extreme weather events will drive mass migration; 1.2 billion people could be displaced globally by 2050, imposing massive economic costs and political instability.

Modelling by the Swiss Re Institute (2021) attempts to capture the costs of these “known unknowns” by applying multiplicative factors, but significant uncertainty remains, and therefore many cost-of-inaction projections are likely to be dramatic underestimates.

What we Need

There is still much work to be done to reduce uncertainty on total costs of climate inaction. However, the data we do have already sends the message loud and clear – turning up the fire hose now can help quell the towering blaze of future costs. In addition, the evidence that climate action offers huge economic, social, and environmental opportunities is clear.

Climate action is too often sidelined by businesses and governments in favor of what are considered more ‘immediate’ concerns. Massive expenditures on military spending, fossil fuel subsidies, and even COVID-19 emergency responses, demonstrate that financial flows have been found for other crises. At the same time, the cost of inaction makes it obvious that dealing with climate change is not something we can postpone. Even outside the costs of inaction, delaying the transition will still have high costs as we continue to pour money into the status quo, (e.g. oil and gas spending), and risk further losses from stranded assets[3]. Delayed policy action to accelerate renewable energy and energy efficiency could result in a doubling of stranded assets losses (IRENA, 2017)[4].

Failing to address climate change will yield monumental future costs for disaster relief, conflict mitigation, humanitarian aid, and mass human migration. On the other hand, investing in a net zero transition will bring its own immediate benefits such as improved energy security, creation of jobs, economic development, and lower, more stable energy costs.

We need to prioritize funding for the climate crisis with the swiftness we did for the pandemic, or the outbreak of war. The crisis is no longer distant, but on our doorstep.

All current and near-term decision making must consider the cost of inaction, and all actors have a role to play:

- Private sector actors must assess the economic impact of climate change on their assets and investments and integrate these assessments into their decision-making. They should also incorporate adaptive measures into business decisions and report transparently on climate risks and costs, while also pushing for greater public sector action.

- Governments and regulators can coordinate the charge for innovation of new climate change mitigation and adaptation technologies, both by directly pouring concessional finance into R&D, and via fiscal policies like emission taxes or carbon prices.

- International finance institutions are well placed to mobilize climate finance, particularly for vulnerable geographies, but must reform their operating models to advance near-term climate finance at scale, as described further in the CPI’s IFI Capital Mobilization Roadmap and in the recommendations of the Global Landscape of Climate Finance.

The findings from the first Global Stocktake reaffirm the need for swift action on climate change, and call for parties to transition away from “fossil fuels in energy systems, in a just, orderly and equitable manner” in order to “achieve net zero by 2050 in keeping with the science” (UNFCCC, 2023). While this signals, as stated by UN Climate Change Executive Secretary Simon Stiell, “the beginning of the end” for fossil fuels, the conclusion fell short of what many hoped would be a clear directive to ‘phase-out’ fossil fuels in all sectors.

We no longer have the luxury of time for incremental change. Given the staggering costs of delaying climate action, it is clear what we need to do: we need to make smart climate investments and policy decisions globally, and we need to do it now.

[1] Average global climate finance needs are estimated at USD 9.7 trillion between 2023 and 2050, moving from an average USD 8.6 trillion per year up to 2030 and rising to USD 10.7 trillion in the two decades after that. For further details please see Methodology document. Changes in our climate finance needs estimates compared to our 2022 Global Landscape report are mainly due to the inclusion of additional scenarios particularly for the agriculture, forestry and other and use (AFOLU), buildings and industry sectors; the update of BloombergNEF scenarios with lower hydrogen and storage investment needs; and re-classification of some carbon capture, use and storage (CCUS) needs estimates from Energy to Industry.

[2] Plus costs of stranded assets and biodiversity loss. See the GLCF 2023 Methodology document for more details.

[3] Stranded assets are investments (typically in fossil fuel industries) that will lose value or become obsolete due to changes in the market, new technologies, or increased environmental regulations related to a transition to a low-carbon economy.

[4] Modelling by IRENA shows that delayed policy action before 2030 could be up to USD 10 trillion higher than in a scenario where action is taken now.