Lab Instrument Analysis: Energy Efficiency Enabling Initiative

This publication is CPI’s analysis of the Energy Efficiency Enabling Initiative, an innovative climate finance instrument endorsed by the Global Innovation Lab for Climate Finance (the Lab). CPI serves as the Lab’s Secretariat. Each instrument endorsed by the Lab is rigorously analyzed by our research teams. High-level findings of this research are published on each instrument, so that others may leverage this analysis to further their own climate finance innovation.

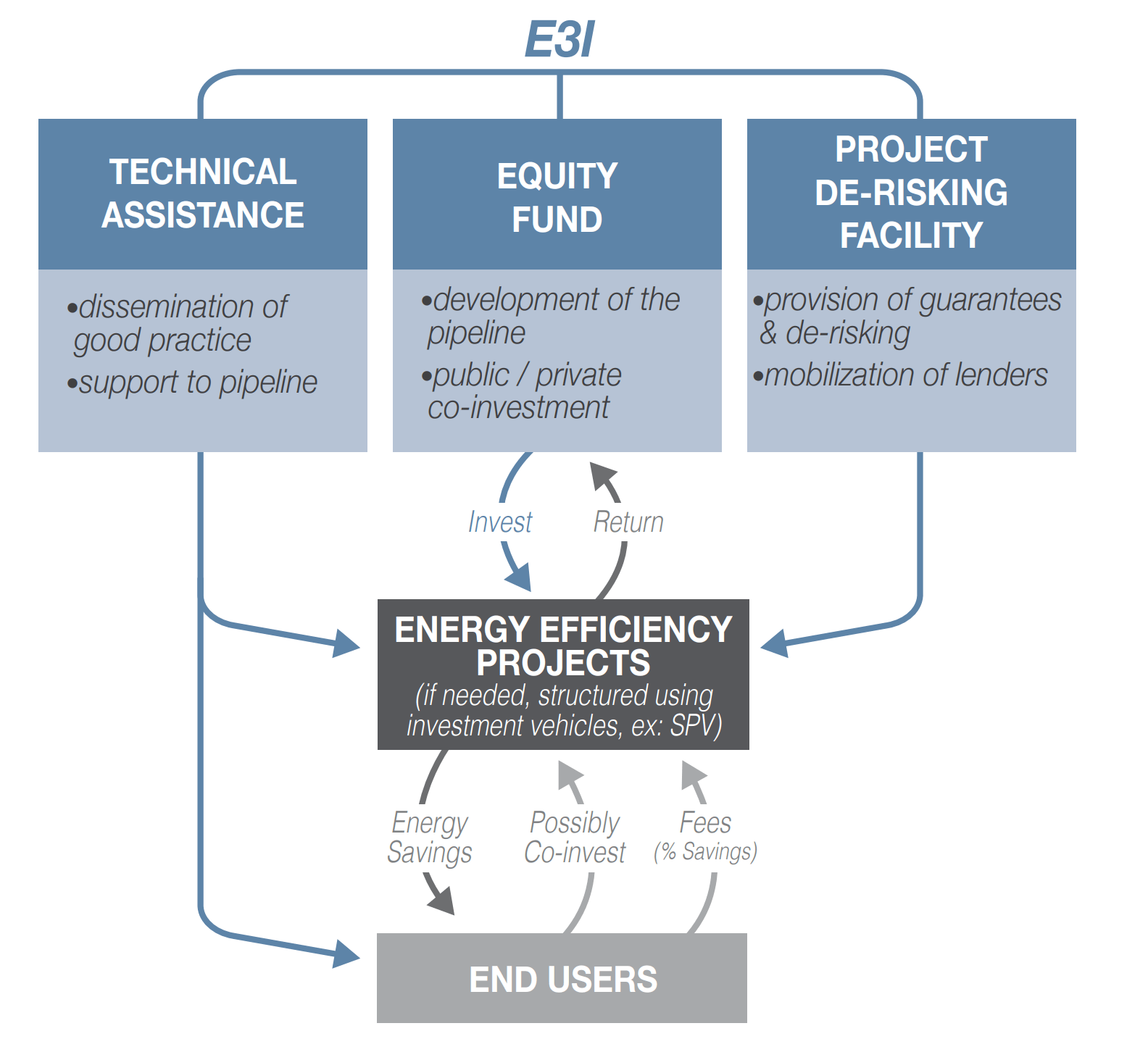

This report provides the analysis on Energy Efficiency Enabling Initiative, a private equity fund that relies on donor-backed equity capital, technical assistance, and risk mitigation instruments to crowd in private investment in energy efficiency.

Energy efficiency has enormous potential to help achieve global climate objectives, but current investment levels fall far short of what is needed to stay within a 2°Celsius climate scenario. The IEA estimates that USD 13.5 trillion in cumulative investment will be required in energy efficiency by 2035, with USD 6 trillion for developing countries.

The funding gap is partly a result of the way in which energy efficiency is financed. Today’s energy efficiency investments are primarily self-financed by end users, making it difficult to scale the market without greater access to debt or equity (IEA, 2014). This is especially true in emerging economies.

The Energy Efficiency Enabling Initiative instrument aims to address these issues. Specifically, it will increase the supply of risk capital (equity) by involving new investors via an energy efficiency equity fund. The fund will have a specific investment mandate to source and support energy efficiency initiatives and will be backed by clear guidelines, investment eligibility criteria, and investment reporting.

The instrument would operate as a private equity fund with a specific investment mandate in selected sectors and energy efficiency technologies.

The initiative will benefit from donor-backed concessional equity capital, which will enhance the risk profile of energy efficiency investments at the fund level by offering priority distributions to private investors. Depending on the geographies targeted, it may be complemented by a guarantee or other instruments to de-risk investments at the project level. Both features aim to mobilize and crowd-in private investors, including institutional investors – as equity partners in the fund, and/or as equity and debt providers in the project-level investments. Tailored technical assistance will also be provided to support the fund and energy efficiency market development.

The instrument could be the first source of equity financing for particularly risky regions, sectors, and technologies.

The Lab Secretariat analysis shows that a USD 100 million fund piloted in potential target countries like Mexico and Colombia could generate 200-225 GWh of annual savings, corresponding to 20-100 kt of CO2 abated every year. When fully invested, the fund would also help end-users save around USD 30 million in energy bills every year. Through to 2025, the replication of the mechanism could deliver up to 9000 GWh, or 5300 ktCO2, if learning is transferred to the market, and the limited availability of public equity is matched with higher investment mobilization through risk mitigation instruments.

We estimate that the overall time needed to prepare a pilot of this instrument is 24 months, which would include structuring the fund and contracts, fundraising, and building a project pipeline in line with investment eligibility criteria.

To establish a fund pilot, an implementing agency would require an estimated USD 1.2 million grant, with USD 700,000 required for the establishment of the fund, and USD 500,000 needed for every country targeted by the fund to finalize the related business plan, and preliminary pipeline.

DESIGN

The initiative would be designed and operationalized largely with public grant resources, which would lower the cost for the private sector.

The three main pillars of the initiative are:

- A one-stop-shop fund with a donor-provided public finance equity component that would facilitate origination of energy efficiency initiatives. Public finance equity, for example, at 30-40%, could mobilize private investors while preserving incentives for the fund manager to operate in a commercially sound manner. Private investors would see a “preferred return” payment structure with donors holding equity in a first-loss position.

- A guaranteed-risking facility could be provided on a case-by-case basis to cover losses beyond a share borne by the equity investor and could incentivize investments that have attractive energy savings potentials but would otherwise be deemed too risky.

- A technical assistance package would target energy service providers looking to operate under ESCO models with Energy Performance Contracts (EPCs), while on the demand side would raise awareness regarding the benefits on energy efficiency, in particular for SMEs.