Can carbon finance work for smallholder agriculture?

Can voluntary carbon markets (VCM) help close the funding gap for sustainable agriculture? The conclusion from the ClimateShot Investor Coalition’s (CLIC) Action Group on financial innovation (AG1) December meeting was: not yet, and not by itself. Members and practitioners broadly agreed that VCM revenue can meaningfully support agribusiness models, however, the market remains too early-stage for carbon to serve as a secure, bankable revenue stream. Reinforcing barriers, such as unreliable demand, front-loaded costs, low and fluctuating carbon prices, and misaligned market incentives, keep carbon credits stuck as a promising but impractical tool.

Despite accounting for 11% of VCM projects, agrifood systems generate just 1% of issued credits. Agrifood projects produce far fewer credits per project than other sectors, a structural problem that affects the viability of smallholder-focused credit models. These projects have reached thousands of farmers and covered millions of hectares, signalling significant potential for scale, however, activity and scale have not yet translated into financial viability. In this blog, we identify three barriers to the efficacy of VCM for agrifood systems—unreliable corporate demand, high upfront costs, and asymmetric market incentives—and discuss what needs to shift to unlock the potential of credits in the agrifood space.

In this blog, we identify three barriers to the efficacy of voluntary carbon markets for agrifood systems—unreliable corporate demand, high upfront costs, and asymmetric market incentives—and discuss what needs to shift to unlock the potential of credits in the agrifood space.

Unreliable corporate demand for agrifood credits, which drives the VCM, is a major constraint to financial viability. Market volumes have declined significantly in recent years as integrity concerns and regulatory uncertainty have eroded buyer confidence. Both offsetting and insetting markets depend on buyer commitments that shift quickly: when demand becomes uncertain, prices follow. During the AG1 meeting, members discussed how many early-stage agribusinesses describe carbon models as too nascent, intensive, or volatile to treat as core revenue, viewing credits as complementary income at best. For agribusinesses operating on thin margins, with high project development costs and returns that take years to appear, this volatility alone can make participation unviable.

Weak demand is partly driven by the voluntary nature of corporate purchases, allowing buyers to routinely scale back commitments when priorities change. Other drivers, more specific to agrifood systems, are low credit yields per project, high monitoring, reporting, and verification (MRV) costs, and unresolved questions around permanence. This makes projects less competitive than credit types that offer buyers greater scale and verification certainty, such as renewables or engineered removals.

These demand-side risks are compounded by costs that are heavily front-loaded against revenues that arrive late, if at all. For example, a carbon project discussed at the AG1 meeting took around two years to scope and cost hundreds of thousands of dollars to reach 7,000 farmers. Costs also add up at the farmer level, with a soil carbon project requiring around USD 150 per farmer for inputs and training, plus an additional USD 150-200 per farmer for MRV. Meanwhile, a smallholder sequestering 1-3 tCO2e per year at current prices of USD 5-15 per credit generates only USD 5-45 annually. In many cases, therefore, the economics do not work without grant subsidies.

For earlier-stage agribusinesses, adopting carbon models requires significant upfront capital, extended payback periods, and tolerance for market volatility. These characteristics structurally favour businesses with established projects and demonstrated credit issuance over those still building the operational infrastructure needed to generate and verify credits. Some models with higher credit volumes per project, such as methane capture or clean cooking energy, can reach viability, but even these remain exposed to demand and regulatory risk.

High upfront costs are compounded by entry barriers to carbon credit adoption. With country-specific methodologies constantly evolving and few documented success cases to learn from, each new entrant essentially rebuilds the same knowledge base from scratch, repeating the same costly learning process. The result is that participation is only viable for projects with enough capital and institutional capacity to absorb years of development costs before seeing any return.

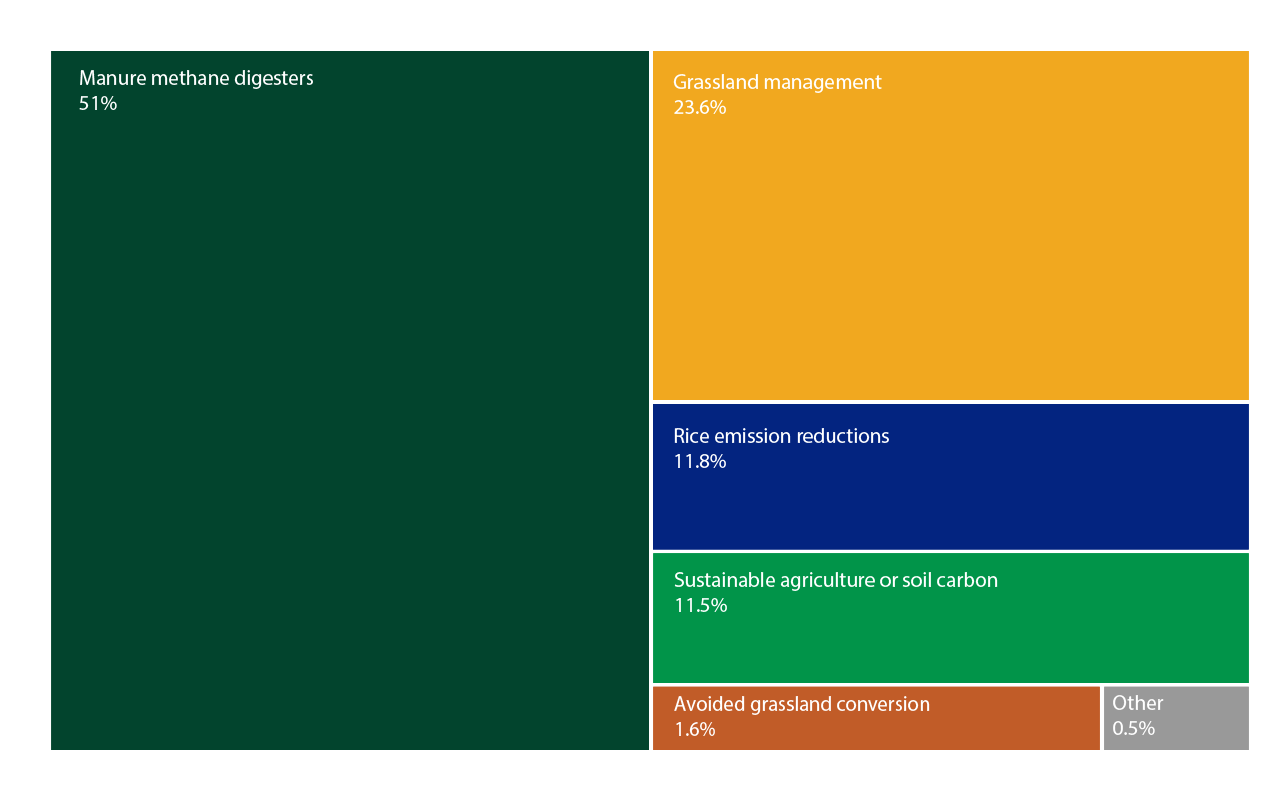

Another issue arises from market design: the VCM currently rewards verifiability over climate impact, prioritizing projects that are easier to measure and certify. Between 2018 and 23, around 75% of agricultural credit issuance was concentrated in just two categories, grassland management and anaerobic manure digesters. Practices with strong mitigation and co-benefit potential, such as agroforestry or food crops like maize remain marginal (see Figure 1). While integrity standards are non-negotiable, market incentives can at times channel investment toward lower-impact interventions that meet existing methodologies, while higher-impact opportunities remain unfunded precisely because they are harder to measure.

Between 2018 and 23, around 75% of agricultural credit issuance was concentrated in just two categories, grassland management and anaerobic manure digesters. Practices with strong mitigation and co-benefit potential, such as agroforestry or food crops like maize remain marginal.

It is important to note that these barriers do not operate in isolation. Unreliable demand suppresses prices, which exacerbates the timing mismatch between costs and revenues. As a result, only the cheapest-to-verify interventions survive. Breaking this cycle requires simultaneous interventions at multiple points.

Figure 1: Agricultural credits issuance, % (Source: Voluntary Registry Offsets Database, Berkeley Carbon Trading Project)

Participants of the AG1 meeting agreed that models that aggregate smallholder farmers are the clearest response to these barriers. Pooling farmer portfolios reduces per-farmer MRV and transaction costs, diversifies risk, and smooths cash flow mismatches that make carbon projects unviable at the individual SME level. Circkular AgroFintech‘s cluster-based model, which groups 80-100 farmers per cluster, illustrates what this looks like in practice: farmers convert agricultural and biomass waste into biochar through pyrolysis and apply it directly to their land, permanently sequestering carbon in the soil. By aggregating this biochar carbon removal (BCR) practice across clusters and paying 60% of revenues upfront, early results suggest an 8-10% income uplift without requiring any farmer investment.

Institutional appetite for these aggregated structures is growing within CLIC’s member base. IFC has expressed interest in aggregated portfolio vehicles, in which carbon serves as a primary source of investor returns, signalling that pooled carbon-backed models are approaching the threshold of investability. GIF is taking a complementary approach, supporting a range of soil carbon projects and seeking to pool learning across them to build sector-wide guidance on financing and implementation.

Participants also agreed on the need for clear, comparable evidence on which agrifood carbon interventions deliver the strongest returns for smallholders, and how transaction costs can be meaningfully reduced. Currently, reporting focuses primarily on capital raised and enterprise growth rather than standardised metrics. As a result, individual enterprises generate evidence in isolation, and the sector lacks the collective knowledge to determine which models improve farmer returns while reducing MRV and intermediation costs at scale. CLIC is exploring how to address this gap through comparative research on the financial mechanics of carbon integration in agrifood investment vehicles.

Voluntary carbon markets will not close the agrifood finance gap on their own. However, with the right aggregation structures and better collective evidence and models, carbon can become a meaningful layer in blended finance for smallholder agriculture. The groundwork is being laid; discussion platforms like CLIC’s action groups demonstrate the potential for the agrifood community to pool data, compare approaches, and build a shared evidence base. This information helps the sector move towards best practices and can help address some of the challenges everyone is facing. The question now is whether the sector can move from isolated experiments to coordinated, evidence-driven approaches fast enough to matter.