Closing the Rural Credit Divide: Pathways to Increase PRONAF Access for Smallholders

Introduction

Smallholder farming occupies 77% of rural properties in Brazil, employs around 10 million people, and accounts for 23% of agricultural production.[1] In this context, the National Program for Strengthening Family Farming (Programa Nacional de Fortalecimento da Agricultura Familiar – PRONAF) stands out as the main federal public policy supporting smallholder farming, offering subsidized rural credit with reduced interest rates. Created in 1995, the program provides credit to finance productive activities, the acquisition of equipment, and the adoption of sustainable practices, with the aim of increasing production, income, and sustainability in rural areas, as well as contributing to food security. Evidence shows that PRONAF has been effective in increasing the production and income of smallholders and reducing inequalities in rural areas, reinforcing its strategic role for a more just and sustainable agricultural transition in Brazil.[2],[3]

In the 2025/26 Agricultural Plan (Plano Safra), the federal government allocated R$ 78.2 billion to PRONAF.[4],[5] However, these resources remain unevenly distributed and insufficient to meet the needs of smallholder farmers. Although smallholders are amongst the most vulnerable to climate change, most still face limited access to rural credit and more restricted financing. A previous study by Climate Policy Initiative/Pontifical Catholic University of Rio de Janeiro (CPI/PUC-RIO) showed that around 85% of smallholders do not have access to credit.[6]

Given this scenario, researchers from CPI/PUC-RIO analyzed the main barriers to rural credit and identified pathways to expand it, ensuring that smallholders have the resources needed to increase sustainable production and strengthen their climate resilience. This study finds that access to technical assistance and membership in farmer cooperatives are key determinants of access to PRONAF.

Existing academic literature already indicates that farmers with higher levels of education, older age groups, and those located in Brazil’s Southern region tend to have greater access to PRONAF.[7],[8] Building on this evidence, CPI/PUC-RIO researchers simulated how access to credit would change if farmers in the North, Northeast, Midwest, and Southeast regions had characteristics similar to those in the South. The results show that expanding technical assistance and rural extension (Assistência técnica e extensão rural – ATER) would be the most effective way to increase access to PRONAF in the North and Northeast, while strengthening cooperative membership would be the most relevant factor in the Southeast and Midwest.

Although rural credit, particularly through PRONAF, needs to reach a larger share of smallholder farmers, expanding access alone is not enough to meet the growing challenges facing Brazil’s agricultural production systems. Climate change is already affecting farmers’ income and livelihoods, increasing the need to strengthen resilience and adaptation.

This publication highlights persistent inequalities in access to credit and emphasizes that strengthening PRONAF requires coordination with complementary public policies, particularly ATER. These services play a critical role in improving the financial, productive, and climate resilience of smallholder farming. In this context, the recent decline in investments in ATER compromises the reach of PRONAF and limits its potential as a strategic instrument for supporting this transition.

What is PRONAF?

PRONAF is a credit program aimed at smallholder family farming. Under Law no. 11,326/2006, family farming is well-defined in terms of size and type of activity performed.[9] Thus, a smallholder farmer is defined as a producer who operates a property smaller than four fiscal modules, works primarily on the property, manages the productive activities, and relies on the farm as the main source of household income.[10] Since the producer does not necessarily need to own the property, settlers, tenants, sharecroppers, and usufructuaries, for example, can also access PRONAF.

Building on Law no. 11,326/2006, the Central Bank of Brazil (Banco Central do Brasil – BCB) in the Rural Credit Manual (Manual do Crédito Rural – MCR) indicates that, in addition to the previous items, the annual income prior to applying for credit via PRONAF must not exceed R$ 500,000.[11]

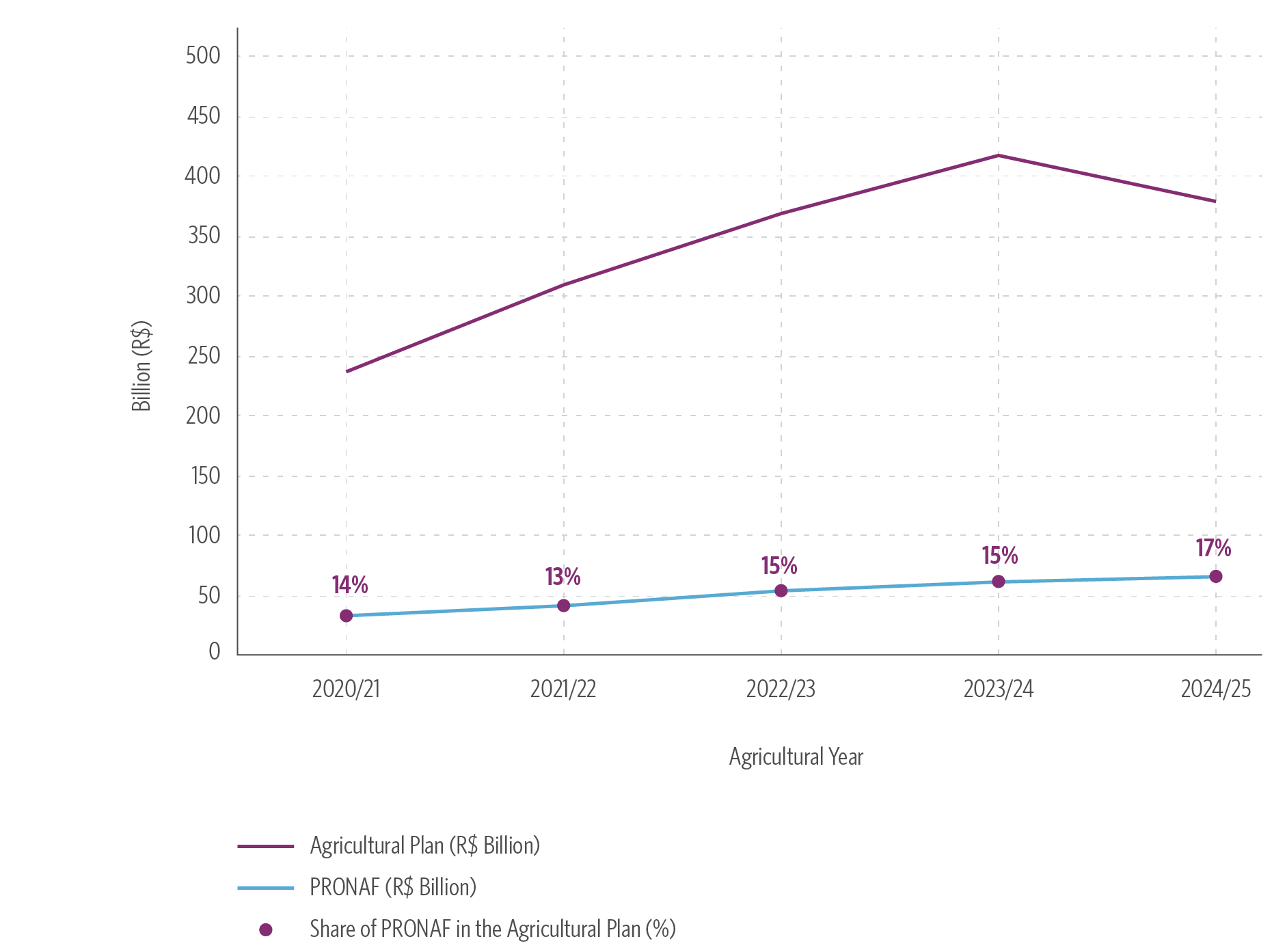

Figure 1 below shows the evolution of the funding allocations of the most recent agricultural plans, as well as the portion of these resources directed to PRONAF.

Figure 1. Evolution of Disbursed Funding to PRONAF and the Agricultural Plan, 2020/21 – 2024/25

Source: CPI/PUC-RIO with data from BCB (2025), 2026[12]

The total amount of funding disbursed to PRONAF has grown over the last six years, even as the total funding for the Agricultural Plan has seen an overall drop (Figure 1). The allocated amount for PRONAF in the most recent 2025/26 Agricultural Plan totaled R$ 78.2 billion.

Although the actual volume allocated to PRONAF reaches tens of billions of reais, these resources remain concentrated across regions, products, and producer profiles, limiting access for many farmers. This unequal access results from several factors. Before examining them in greater detail, however, it is important to understand the documentation requirements for obtaining credit. As a credit program, PRONAF involves specific eligibility criteria and documentation requirements that can create barriers for small-scale farmers. Box 1 outlines these requirements.

Box 1. Documentation Requirements for Obtaining PRONAF

While the legal and regulatory requirements for obtaining PRONAF are well-defined, the documentation required for implementation varies. To begin with, smallholders are required to complete the National Registry of Family Farming (Cadastro Nacional da Agricultura Familiar – CAF, formerly the Declaration of Aptitude for PRONAF – Declaração de Aptidão ao Pronaf – DAP) to be considered a smallholder farmer eligible for PRONAF.

PRONAF offers a range of credit lines designed to meet the diverse needs and profiles of farmers. These lines often differ in their eligibility criteria, conditionalities, and repayment terms, with some providing more favorable financial conditions than others. Access to these tailored credit options is linked to specific versions of the CAF, which certify that smallholders meet the legal and socioeconomic requirements to benefit from financing arrangements. In this way, the CAF serves not only to confirm a farmer’s status as a small-scale producer but also to determine eligibility for credit lines with conditions that are better aligned with their production context and income level.

Consequently, while the CAF is the primary instrument used to identify and qualify farmers for PRONAF, it encompasses different classifications rather than functioning as a single, uniform document. This also means that there is a varied level of difficulty in completing the CAF. Oftentimes, securing better interest rate conditions requires a farmer to meet more conditionalities and submit evidence to justify these better conditions.

In addition to CAF, farmers must also present the usual documents required to obtain bank credit, such as identification documents (including Individual Taxpayer Registration), marriage certificate, proof of residence, voter registration card, and proof of voting in the last election. Additionally, the process also requires several documents related to the property, such as the Rural Environmental Registry (Cadastro Ambiental Rural – CAR), Tax on Rural Land Property (Imposto Territorial Rural – ITR), lease, deed or a similar document declaring ownership of the property, and the Rural Property Registration Certificate (Certificado de Cadastro do Imóvel Rural – CCIR). Furthermore, applications also require a soil analysis for agricultural projects and documentation on other movable and immovable properties.[13]

Beyond these extensive requirements, financial intermediaries that grant PRONAF credit may require additional documentation or use the abovementioned documentation in greater depth. Therefore, small-scale farmers with limited financial history may find it more difficult to access PRONAF than other farmers who have an established history of credit, repayments, and income.

Profile of Smallholders who Obtain PRONAF

Allocated resources for PRONAF credit exceeded R$ 78 billion in the 2025/26 Agricultural Plan. The Plan provides more than R$ 8.26 billion in subsidies for this type of credit, underscoring the importance of understanding inequalities in access to the program from both a public spending and a policy effectiveness perspective.[14]

In this study, PRONAF access is analyzed at the municipal level using data from the Brazilian Institute of Geography and Statistics (Instituto Brasileiro de Geografia e Estatística – IBGE). The empirical analysis relies on the 2017 IBGE Agricultural Census, the most recent census data available, referring to the 2016/17 Agricultural Year. As a result, while earlier sections present more recent figures on rural credit, the empirical assessment draws on the most comprehensive dataset currently available to examine barriers to smallholder farmers’ access to PRONAF.

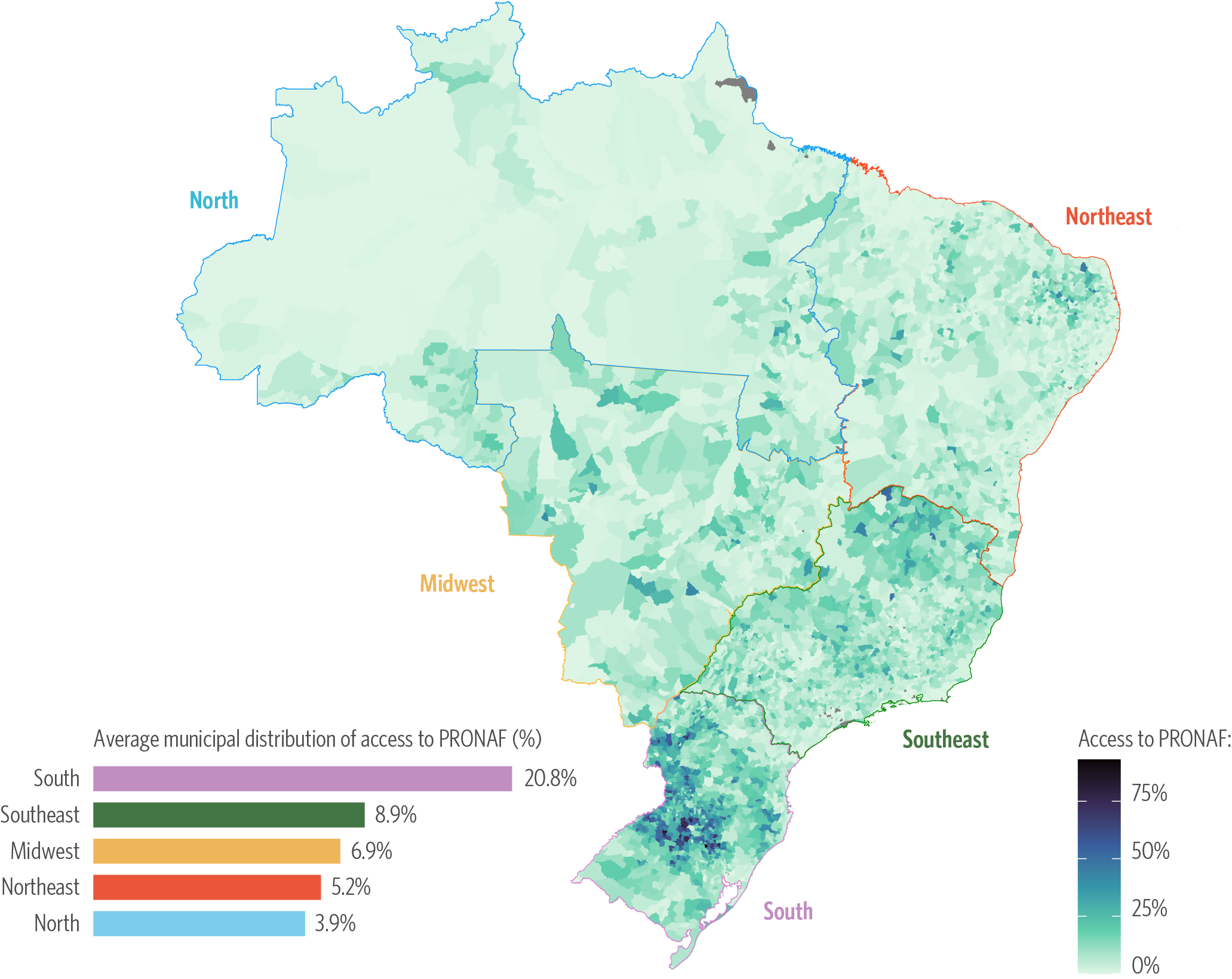

In this context, Figure 2 illustrates the municipal distribution of PRONAF access among smallholders.

Figure 2. Share of Smallholder Access to PRONAF in the 2016/17 Agricultural Year

Note: The grey areas indicate municipalities where it was not possible to calculate access to PRONAF, generally because they have few or no smallholder farmers. These municipalities are primarily concentrated in Brazil’s Northern Region, where non-urban areas largely consist of environmental reserves, Indigenous lands, or other legally protected forms of land use. Regional averages are calculated as the means of municipal PRONAF access values within each region, rather than through direct aggregation of regional data. Brazil’s Agricultural Year runs from July 1st to June 30th of the following year.

Source: CPI/PUC-RIO with data from the 2017 Agricultural Census, 2026

Figure 2 shows a clear concentration of access to PRONAF in Brazil’s South region, in contrast to significantly lower levels of access in the North and Northeast. The regional disparity becomes more evident in the bar chart, which presents the municipal average share of smallholder farmers accessing PRONAF in each region. On average, around 21% of smallholders in municipalities in the South access PRONAF compared to approximately 5% in the Northeast and 4% in the North. In other words, average municipal access to PRONAF in the South is roughly five times higher than in the North.

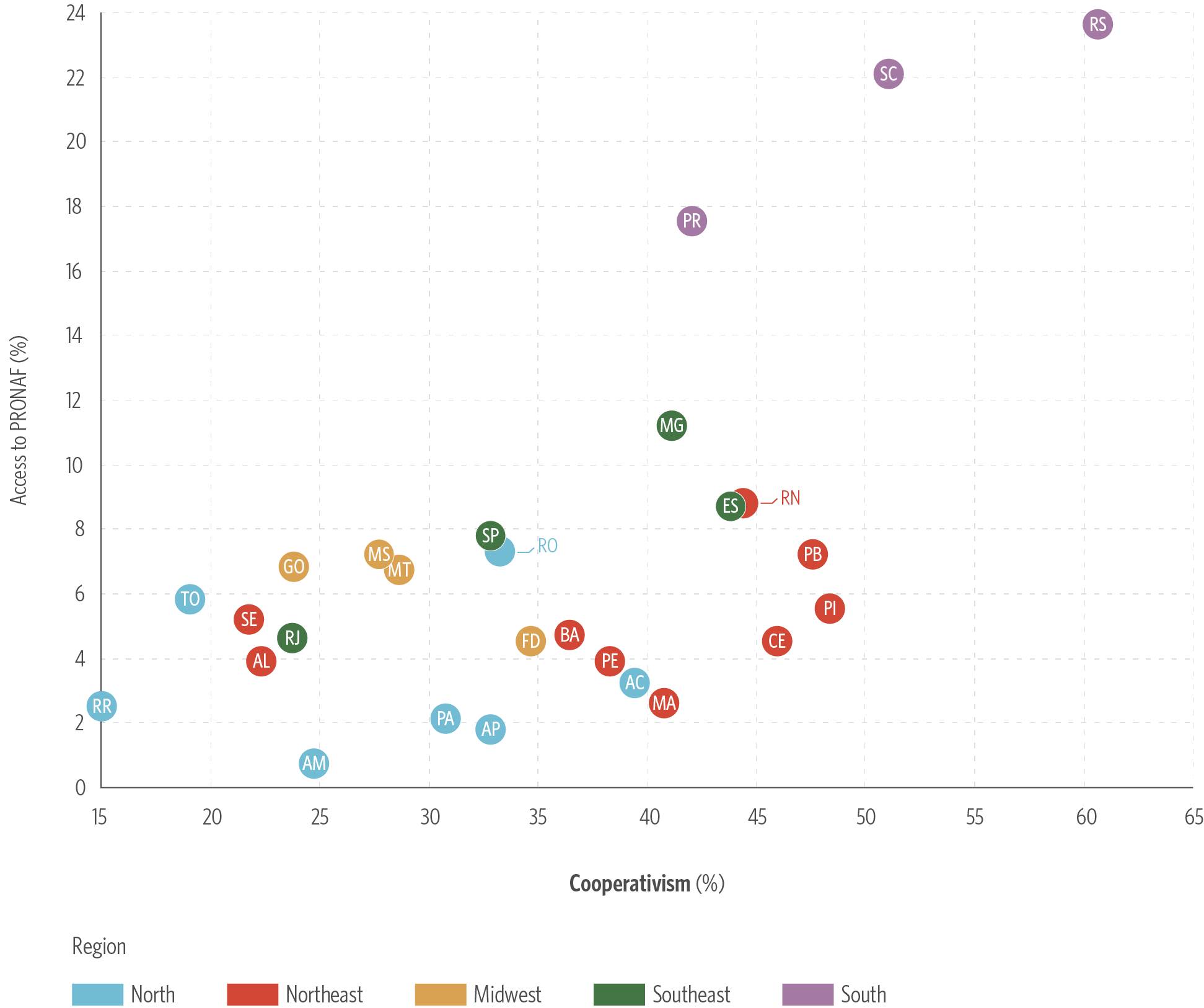

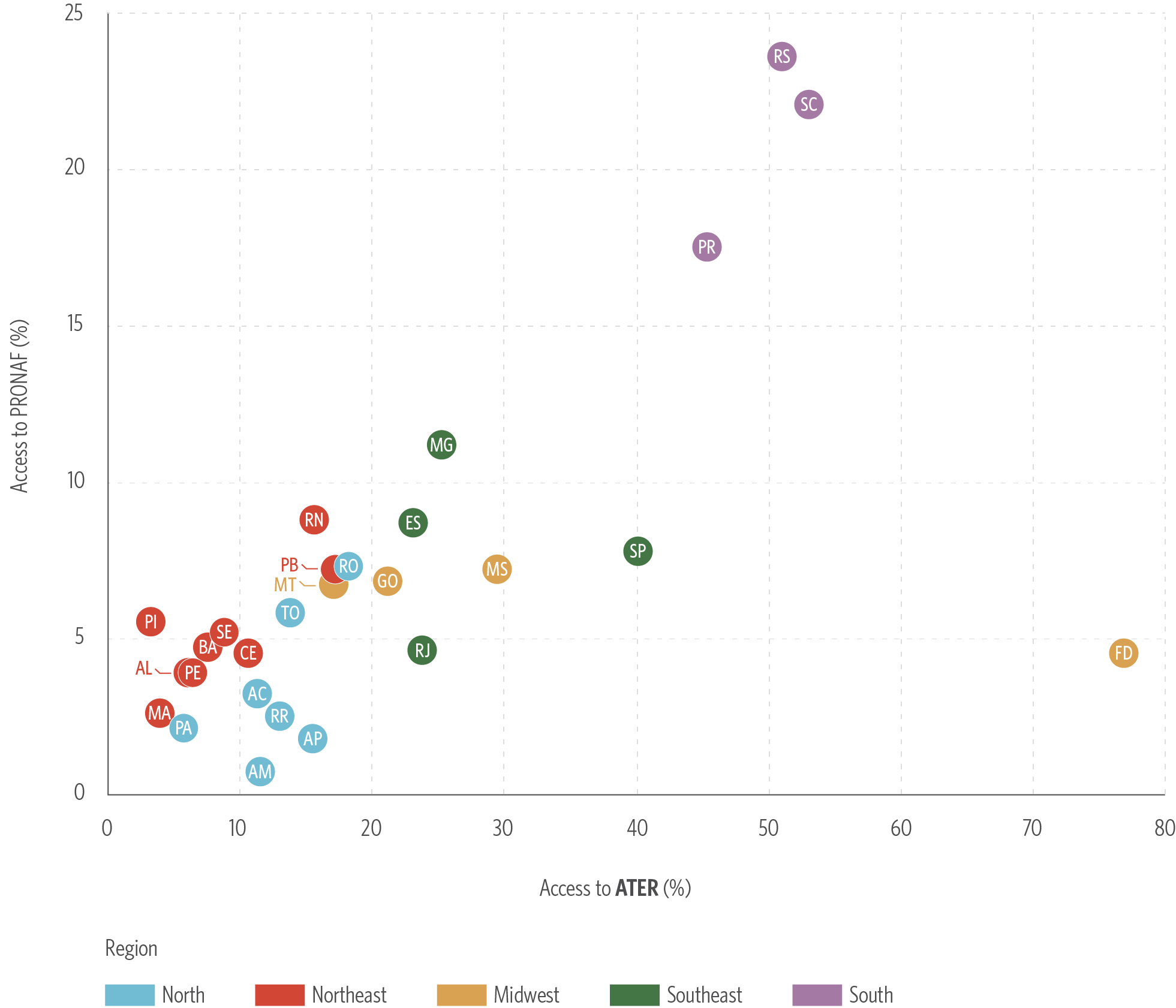

Based on these results, the analysis further examines how specific factors influence access to PRONAF, using data from the 2017 Agricultural Census. In particular, access to ATER and membership in farmer cooperatives are analyzed as key determinants of credit access across Brazilian municipalities, as shown in Figure 3.

Figure 3 reinforces the existence of strong regional disparities. The South (shown in purple) combines higher average access to PRONAF with greater availability of ATER services and higher levels of cooperative participation. On the other hand, the North and Northeast (shown in blue and red, respectively) display the opposite pattern: low levels of access to PRONAF, ATER, and cooperatives. Finally, the Southeast and Midwest present intermediate levels of acces to the variables under consideration.

Figure 3. State Averages for Access to PRONAF

Cooperativism (%)

ATER (%)

Source: CPI/PUC-RIO with data from the 2017 Agricultural Census, 2026

Overall, Figure 3 suggests a strong association between higher access to PRONAF, greater availability of technical assistance, and strong ties to cooperatives. Together, these factors reflect a broader issue: smallholders’ access to quality information. Limited access to information, generally associated with lower levels of education and restricted access to banking services, limits farmers’ ability to identify and secure suitable credit options. At the same time, technical assistance and membership in cooperatives help bridge information gaps by disseminating knowledge, strengthening productive practices, and facilitating access to financial services.

In addition to these key variables, Box 2 details the relationship between gender and access to PRONAF.

Box 2. Gender and Access to PRONAF

PRONAF is formally available to any individual who meets the criteria defining a smallholder farmer and can demonstrate productive and repayment capacity. However, in practice, gender inequalities and other structural barriers affect women’s access to rural credit. These challenges do not necessarily stem from formal restrictions in the program but from other structural barriers that shape opportunities differently for men and women in rural areas. Data from the 2017 Agricultural Census show that only about 13% of loans granted under PRONAF were directed to properties managed by women, even though women run 20% of properties classified as smallholder farms.

To address this gap, the federal government created PRONAF Mulher in 2003 to expand small-scale female farmers’ access to subsidized rural credit.[15] Disbursements under this sub-program significantly increased (351%) between the 2020/21 and 2024/25 Agricultural Plans, rising from R$ 59.38 million to R$ 268.03 million, according to BCB data at current prices. This movement is also evident in the fact that the share of PRONAF Mulher in total Agricultural Plan disbursements also grew over the same period, from 0.18% to 0.41%. Despite this progress, women-led establishments access PRONAF, on average, 16 percentage points less frequently than those run by men, signaling persistent barriers to inclusion.

Addressing this disparity requires not only expanding financial resources of PRONAF Mulher but also identifying and addressing the structural barriers related to access to credit, including gender inequalities in access to information, technical assistance, and membership in productive networks and cooperatives in rural areas.

The discrepancy between access to PRONAF observed between the South and other Brazilian regions suggests that there are additional structural factors that favor access to credit in this region,other than the determinants analyzed (association with cooperatives and access to ATER). These factors may include institutional, historical, or social characteristics that are not directly observable in the database. Thus, equalizing access to PRONAF in other regions requires more than isolated advances in these determinants but also coordinated public policies capable of reproducing, at least partially, the institutional environment that supports greater access to credit in the South.

Determinants of Access to PRONAF

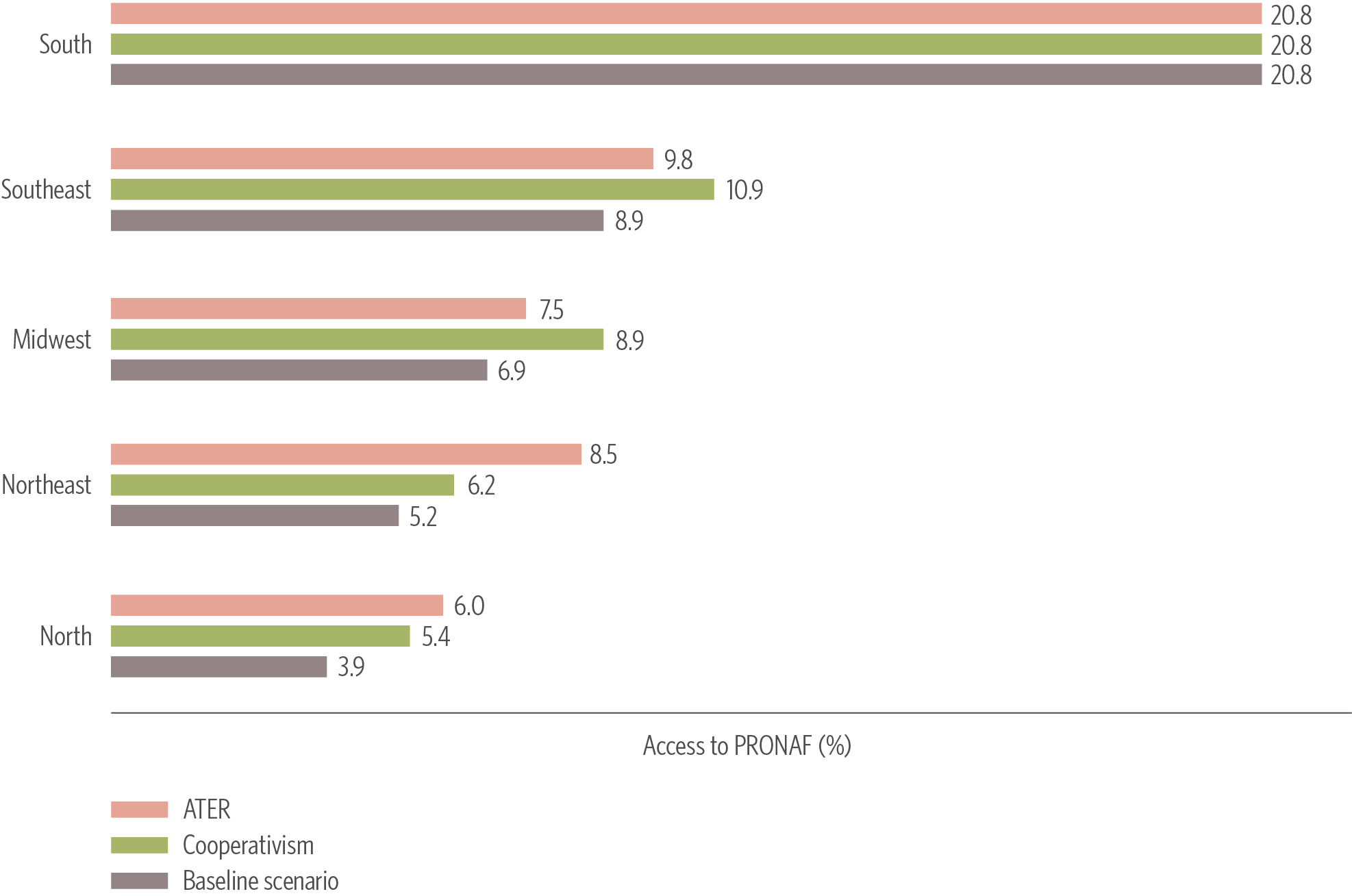

To better understand how access to technical assistance and membership in cooperatives affect the likelihood of obtaining PRONAF, this analysis conducts a counterfactual simulation. The exercise estimates how access to PRONAF would change if other Brazilian states had average characteristics similar to those observed in the South. This approach helps isolate the effects of structural variables, such as ATER and cooperativism, on rural credit access (Figure 4).

Figure 4. Simulation of Access to PRONAF by Region

Note: The baseline scenario considers in the simulation that each region has its own averages for ATER and cooperativism. Some values in the baseline scenarios differ marginally from the averages shown in Figure 1, since in this exercise the results were estimated using the model rather than calculated directly from the observed averages, as in Figure 1.

Source: CPI/PUC-RIO with data from the 2017 Agricultural Census, 2026

Figure 4 presents the results of these simulations by comparing observed levels of access to PRONAF in each region with hypothetical scenarios in which the key structural variables are aligned with the levels observed in the South. This approach helps illustrate how differences in access to technical assistance and participation in cooperatives may influence regional disparities in rural credit access.

To enhance the comparison, access to PRONAF is first analyzed presented on the characteristics observed in each region. Estimated access levels are then calculated by adjusting these characteristics to match those of the South. For example, the baseline level of access in the North is 3.9%. If the level of cooperative membership in the region were equivalent to that of the South, access to PRONAF would increase to 5.4%, representing an increase of 38.5%. Similarly, if the provision of technical assistance in the North matched Southern levels, access to PRONAF would rise by 53.8%, reaching 6%.

Although the results are derived from a simulation exercise, they offer clear indications for policy design. They show that expanding access to rural credit depends on complementary policies, especially investments in ATER and strengthening cooperatives. In the case of the North, strengthening ATER stands out as the most direct way to expand smallholders’ access to PRONAF, reinforcing that credit policy is more effective when linked to other structural interventions.

For the Northeast, the average levels of these two variables are associated with an average PRONAF access rate of 5.2%. If the region had the same level of ATER as the South, while holding all other characteristics constant, access to PRONAF would be 8.5%, representing a gain of 63.5%. By contrast, raising cooperative membership to Southern levels would increase access to 6.2%, corresponding to a 19.2% increase.

In the Midwest and Southeast, cooperative participation appears to play a more significant role in expanding access to PRONAF than ATER, although both factors contribute positively. In the Midwest, aligning cooperative membership with Southern levels would increase access to 8.9%, a rise of 28.9%, while matching the provision of ATER would raise PRONAF access to 7.5%, an increase of 8.7%. In the Southeast, similar adjustments would increase access to 10.9% through higher cooperativism (a 22.5% gain) and to 9.8% through expanded ATER services (a 10.1% gain).

Implications for Public Policy

PRONAF is a central instrument for supporting smallholder farming and has strong potential to enhance productivity, income generation, and resilience. Its effectiveness, however, depends on its integration within a broader portfolio of public policies aimed at strengthening rural production systems. The analysis highlights ATER as a particularly important determinant of access to PRONAF, pointing to an underexplored and feasible pathway for expanding financial inclusion in rural areas.

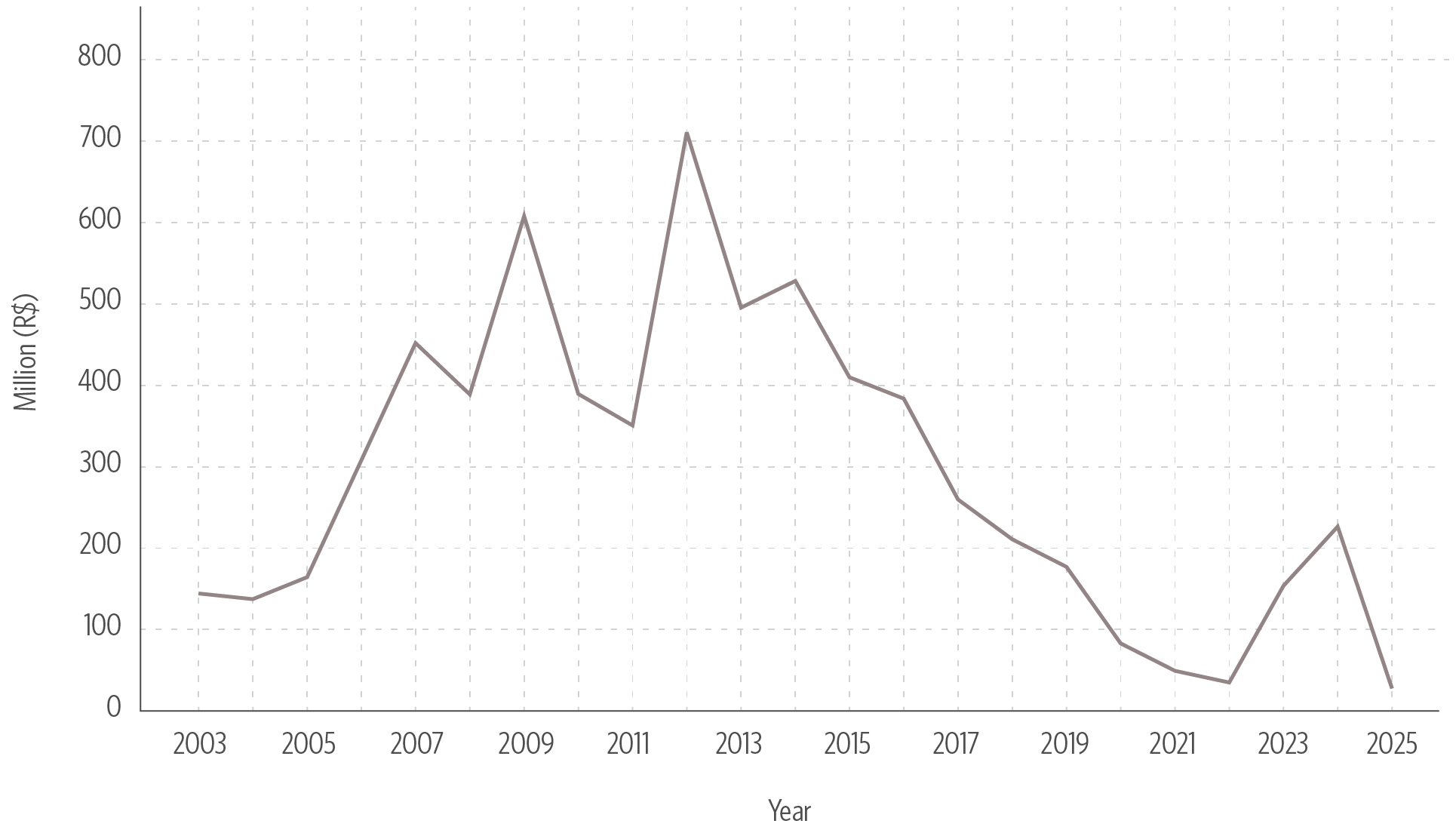

Despite its importance, resources allocated to ATER remain limited. In the 2025/26 Agricultural Plan, only R$ 240 million was allocated to ATER, an amount lower than in previous years and consistent with a broader trend of declining investment.[16],[17] Box 3 presents the evolution of actual federal expenditures on ATER between 2003 and October 2025, based on data from the Ministry of Agrarian Development and Family Agriculture (Ministério do Desenvolvimento Agrário e Agricultura Familiar – MDA).

Box 3. Evolution of Federal Expenditures on ATER in Brazil

Given that the budget for technical assistance and rural extension (Assistência técnica e extensão rural – ATER) reached a planned R$ 240 million in the 2025/26 Agricultural Plan, it is informative to analyze the actual expenditures on this policy.[18] Through the Brazilian Law of Access to Information (Lei de Acesso à Informação – LAI), CPI/PUC-RIO obtained the actual expenditures on ATER from 2003 to October 2025 (latest data available) from the Ministry of Agrarian Development and Family Agriculture (Ministério do Desenvolvimento Agrário e Agricultura Familiar – MDA).[19] Figure 5 shows the actual federal expenditures on ATER from 2023 to 2025. The monetary values are all inflation-adjusted to June 2025 prices, based on the IBGE’s Extended National Consumer Price Index (Índice Nacional de Preços ao Consumidor Amplo – IPCA) for the month and year in which the 2025/26 Agricultural Plan was released.

Figure 5. Actual Federal Expenditures on ATER, 2003-2025 Source: CPI/PUC-RIO with data from the MDA (2025), 2026

Source: CPI/PUC-RIO with data from the MDA (2025), 2026

Real-term expenditures on ATER show a downward trend, despite a temporary increase in these amounts in 2023 and 2024. Actual expenditures in 2024 were around R$ 225.39 million and in 2025 (through October) dropped to around R$ 26.48 million.[20] According to the MDA, although the MCR does not limit the percentage that can be spent on contracting ATER, average market values are used as a reference. Thus, for example, approximately 0.5% of the rural credit financing amount can be directed to the preparation of the technical project, while 1.5% of the financing amount can be directed to cover the costs of monitoring the execution of the financing by the ATER technician.

Investment in ATER is essential to expand smallholder farmers’ access to PRONAF, as well as for its productive and climate-related effects. While access to PRONAF contributes to greater financial inclusion and strengthens the productive capacity of small-scale farmers, ATER is crucial for transforming credit into sustainable productivity gains and increased climate resilience, especially in a context in which smallholder farming remains insufficiently covered by agricultural risk management instruments, such as insurance. Resilience should be expressed in a preventive and structural manner, rather than merely as a response to losses resulting from extreme climatic events.

The downward trend in ATER funding, highlighted in Box 3, is particularly concerning for regions that are more vulnerable to the impacts of climate change, where smallholders frequently identify the lack of ATER as the main barrier to climate adaptation. In these regions, access to credit without accompanying technical support tends to have a limited impact on productivity and climate resilience.

Although subsidies for PRONAF exceed R$ 8 billion under the 2025/26 Agricultural Plan, financial support alone is insufficient to foster production systems that can adapt to climate risks. Building resilience requires a broader policy approach that combines credit with technical assistance, risk management instruments, and measures to strengthen productive networks.

Similarly, low levels of cooperative membership limits knowledge sharing, the adoption of improved practices, and access to information on available credit options, restricting smallholders’ ability to navigate credit requirements and participate effectively in the financial system. Addressing these barriers does not necessarily require substantial increases in public spending. For example, technical assistance can support farmers in obtaining the required documentation, selecting appropriate credit lines, and aligning financing with crop cycles. Other constraints, such as collateral requirements, remain structural and will require coordinated action across institutions.

Overall, findings show that access to rural credit for smallholder farmers remains both limited and uneven. Expanding PRONAF is therefore necessary but not sufficient to ensure resilient agricultural production. Resilience must be understood as a multidimensional objective encompassing financial, productive, and climate dimensions. While credit contributes directly to financial inclusion, complementary policies—particularly ATER, the strengthening of cooperatives, and information dissemination—are essential for broadening access to PRONAF and ensuring that finance results in sustainable productivity gains.

Thus, the expansion of PRONAF, through increased subsidies and more targeted credit lines, should occur alongside a well-coordinated portfolio of complementary public policies. Such an integrated approach is critical for reducing regional inequalities, expanding access to finance, and supporting a transition toward more resilient, sustainable, and inclusive small-scale farming.

This work is supported by a grant from Porticus Foundation. This publication does not necessarily represent the view of our funders and partners.

The authors would like to thank Kirsty Taylor, Giovanna de Miranda, and Camila Calado for editing and revising the text and Meyrele Nascimento and Nina Oswald Vieira for formatting and graphic design.

[1] IBGE. Censo Agropecuário 2017. 2017. Access date: September 25, 2025. bit.ly/3L57xxJ.

[2] Machado, B. S., M. C. R. Neves, M. J. Braga, and D. R. M. Costa. “Access and impact of Pronaf in Brazil: evidence on typologies and regional concentration”. Revista de Economia e Sociologia Rural 62, no. 3 (2024): e273994. bit.ly/4hqdgKI.

[3] Batista, Henrique R. and Henrique D. Neder. “Efeitos do Pronaf sobre a pobreza rural no Brasil (2001–2009)”. Revista de Economia e Sociologia Rural 52 (2014): 147–166. bit.ly/4qp9a9z.

[4] To learn more about the data from the 2025/2026 Agricultural Plan, visit: bit.ly/4obQNnk. Access date: September 25, 2025.

[5] For reference, R$ 78.2 billion is equivalent to US$ 14.4 billion, following June, 2025 exchange rates (where US$ 1 is equivalent to R$ 5.43).

[6] Souza, Priscila and Amanda de Albuquerque. Family Farming in Brazil: Inequalities in Credit Access. Rio de Janeiro: Climate Policy Initiative, 2023. bit.ly/Family-Farming-Brazil.

[7] Freitas, Rogério E.. Pronaf: observações sobre o programa e desafios futuros. Rio de Janeiro: Instituto de Pesquisa Econômica Aplicada (Ipea), September 2025. bit.ly/3Jr4T4T.

[8] Amaral, Felipe J. G. do. “Análise da concentração e da desigualdade na distribuição de crédito rural no Brasil”. PhD diss., University of São Paulo, 2023. bit.ly/4qqQ7vM.

[9] Law no. 11,326, July 24, 2006. bit.ly/3LqMVA0.

[10] The fiscal module is a land unit, a measure of area, whose definition and updating are carried out by the National Institute for Colonization and Agrarian Reform (Instituto Nacional de Colonização e Reforma Agrária – INCRA). Its definition takes into account the type of usual crop, income from agricultural production in the usual crop and other possible crops in that locality, and the size of a “family property”. The fiscal module is a municipal metric. The fiscal modules for most municipalities were established in the 1980s. Updates to the fiscal module whenever a municipality is created or changes in the size of the fiscal module of a given municipality are necessary, which is not common for most municipalities. The fiscal module ranges from 5 to 110 hectares. Furthermore, it is a relevant concept in different regulations, such as the Forest Code and the Rural Credit Manual, among other regulations and policies related to land. Learn more at: EMBRAPA. Fiscal Modules. sd. Access date: January 30, 2025. bit.ly/3Te0OAI.

[11] The MCR is the regulatory document for rural credit in Brazil. Learn more at: MCR. Normas 10-2-1. 2025. bit.ly/4pISYi5.

[12] BCB. Tabelas e Microdados do Crédito Rural e do Proagro. 2025. Access date: November 25, 2025. bit.ly/4i15VkX.

[13] Governo Federal. Acessar o Programa Nacional de Fortalecimento da Agricultura Familiar (Pronaf). 2025. Access date: September 25, 2025. bit.ly/4hporDn.

[14] Júnior, Daumildo. Montante para equalização do Plano Safra pode crescer 23,4% em 2026. Estadão. 2025. Access date: September 25, 2025. bit.ly/43vciqH.

[15] Cavalcante, Amanda da Cruz and Rodolfo Araújo de M. Filho. “Acesso ao crédito rural e gênero: uma análise do processo de aquisição do Pronaf Mulher no Assentamento Normandia em Caruaru – PE”. Revista Brasileira de Educação no Campo 8 (2023). bit.ly/4rCiw2C.

[16] MDA. Plano Safra 2025/2026. 2025. Access date: September 25, 2025. bit.ly/4obQNnk.

[17] ASBRAER. Plano Safra da Agricultura Familiar destina R$ 307 milhões para Assistência Técnica e Extensão Rural. 2024. Access date: September 25, 2025. bit.ly/3LcmAWp.

[18] MDA. Plano Safra 2025/2026. 2025. Access date: September 25, 2025. bit.ly/4obQNnk.

[19] MDA. Resposta e-SIC – 54800.001489/2025-15. Clarifications provided through the Law of Access to Information, December 23, 2025. bit.ly/4ps55Qj.

[20] Expenditures use June 2025 prices.