Landscape of Methane Abatement Finance

Sharp and rapid reductions in methane emissions this decade are essential to limiting global warming to 1.5°C. While carbon dioxide has a longer lasting effect, methane has 80 times the warming power of CO2 in the first 20 years after emissions reach the atmosphere, meaning methane is setting the pace for near-term global warming. Reducing human-caused methane emissions by 30% this decade from 2020 levels, as set out in the Global Methane Pledge, would avert at least 0.2°C in global warming by 2050 (CCAC and UNEP, 2021).

Even though methane is responsible for nearly half of net global warming to date, our findings show that finance for methane abatement measures represented less than 2% of total climate finance flows, or just over USD 11 billion, in 2019/2020[1]. At least a ten-fold increase in methane abatement finance is necessary to meet the estimated more than USD 110 billion needed from private and public sources annually.

This first-of-its-kind report on methane mitigation finance aims to assess global investment in methane abatement activities and create a baseline against which investment needs and progress can be measured. This work focuses on existing and established abatement solutions in three broad sectors: fossil fuels, waste (solid waste and wastewater), and agriculture, forestry and land use (AFOLU). Together, these sectors account for 95% of human-made methane emissions.

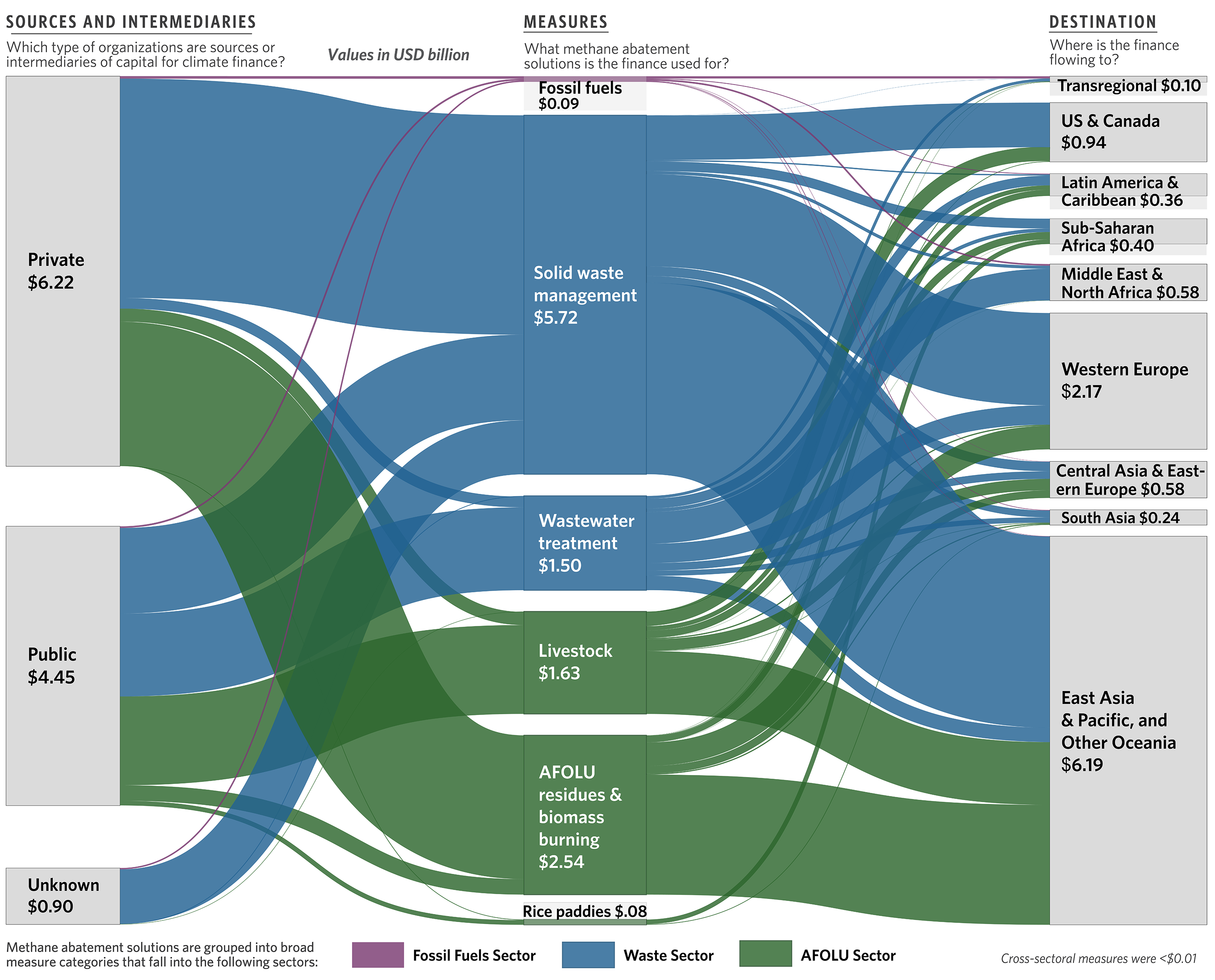

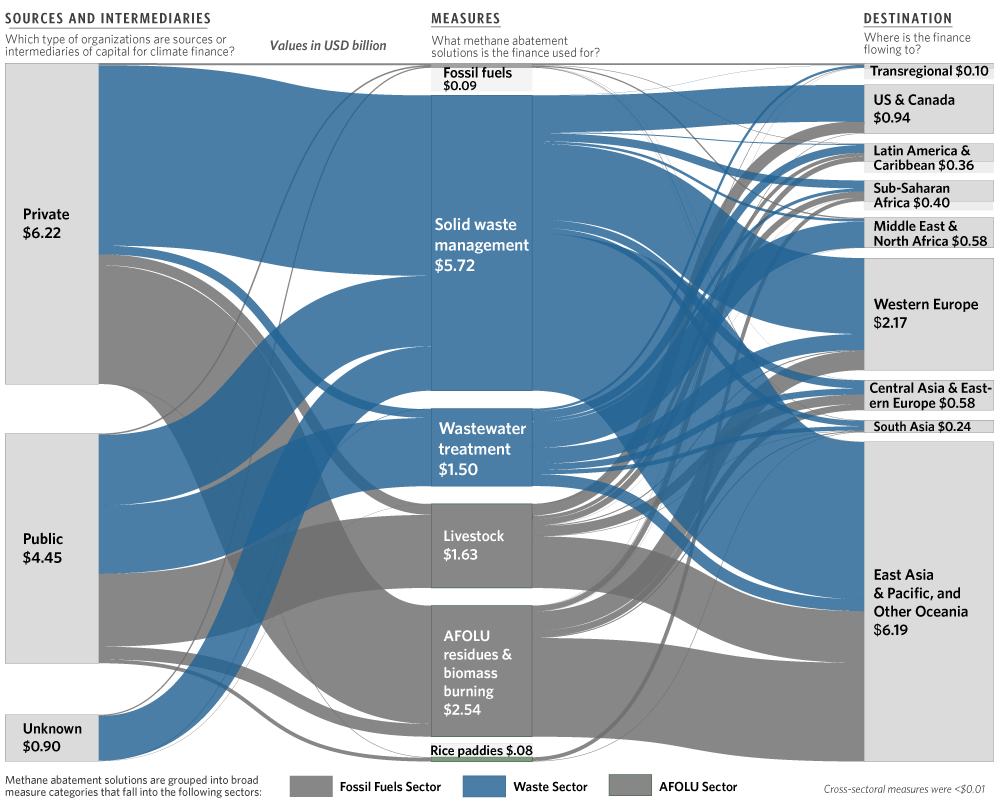

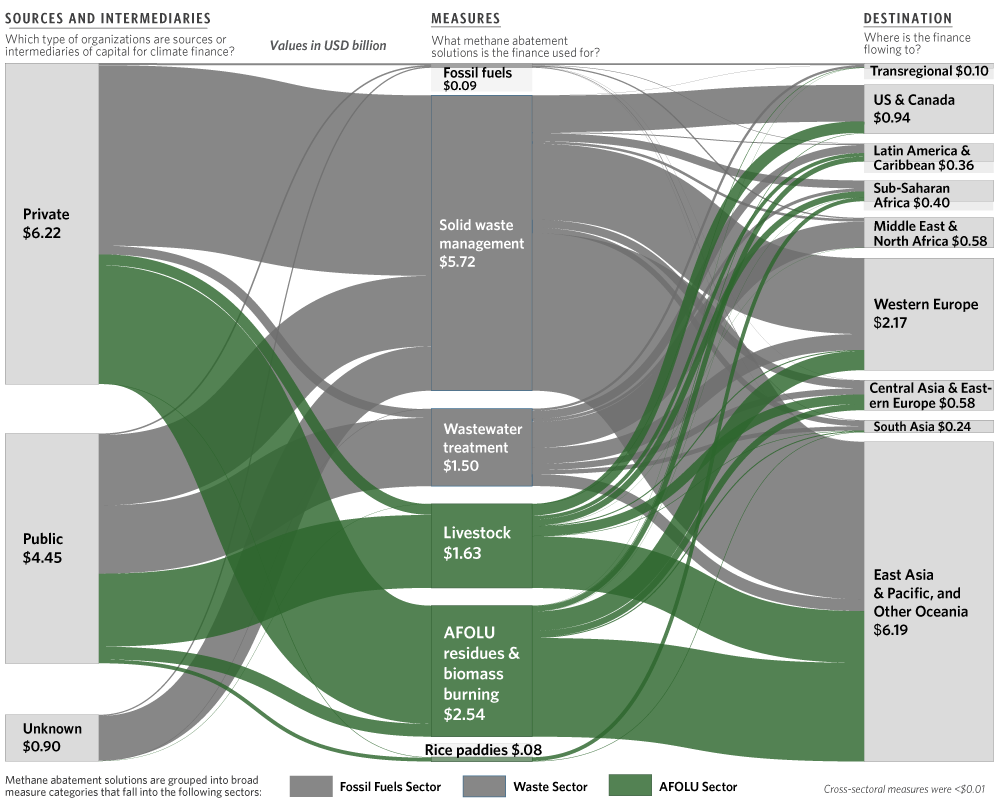

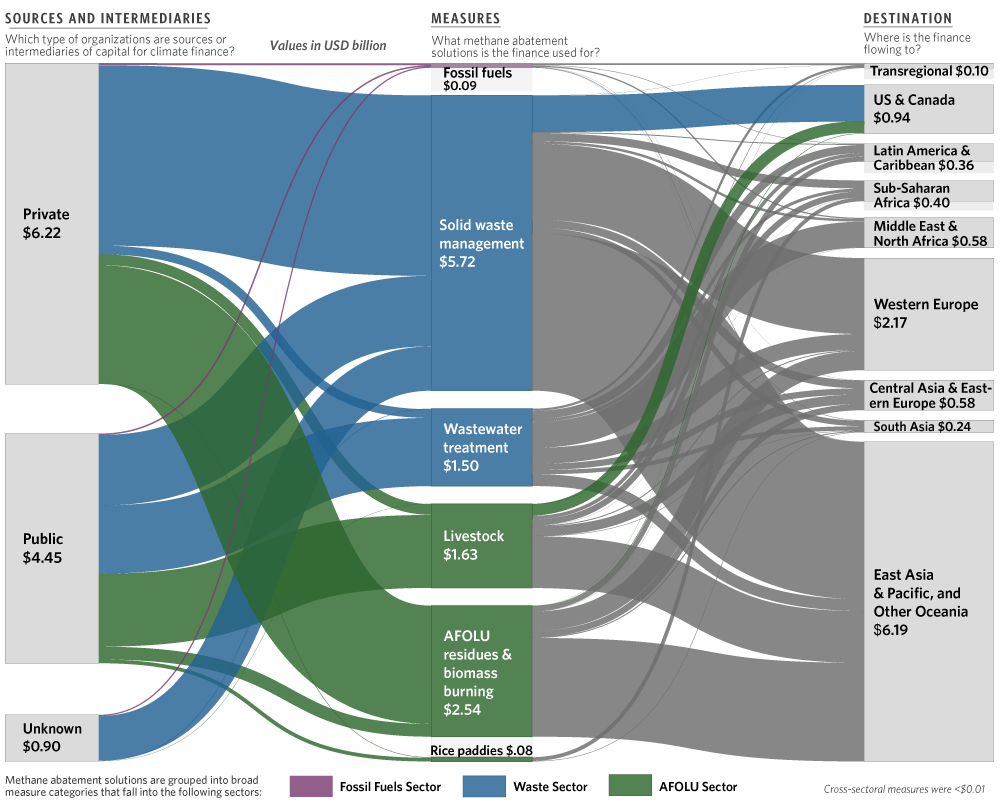

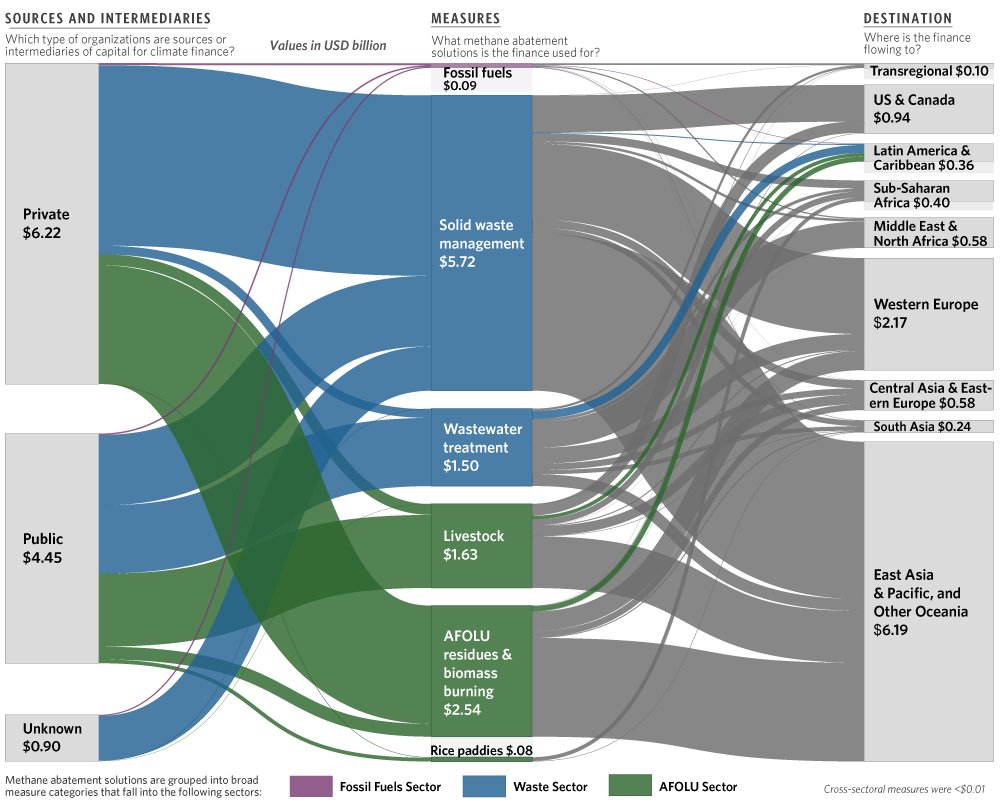

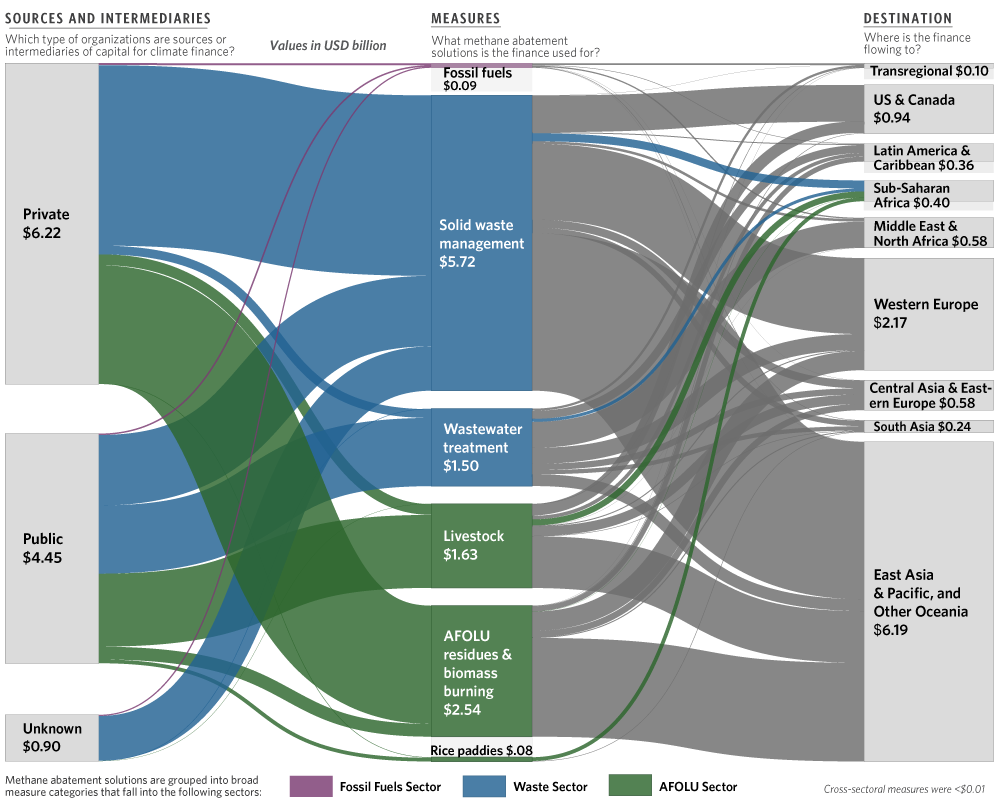

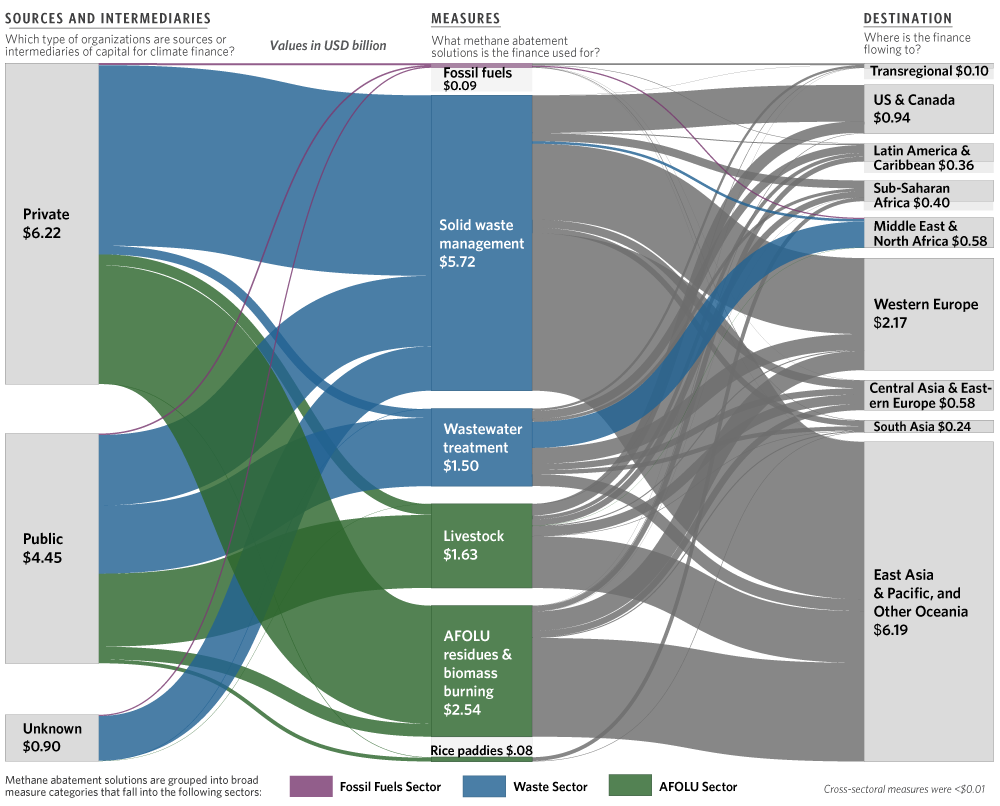

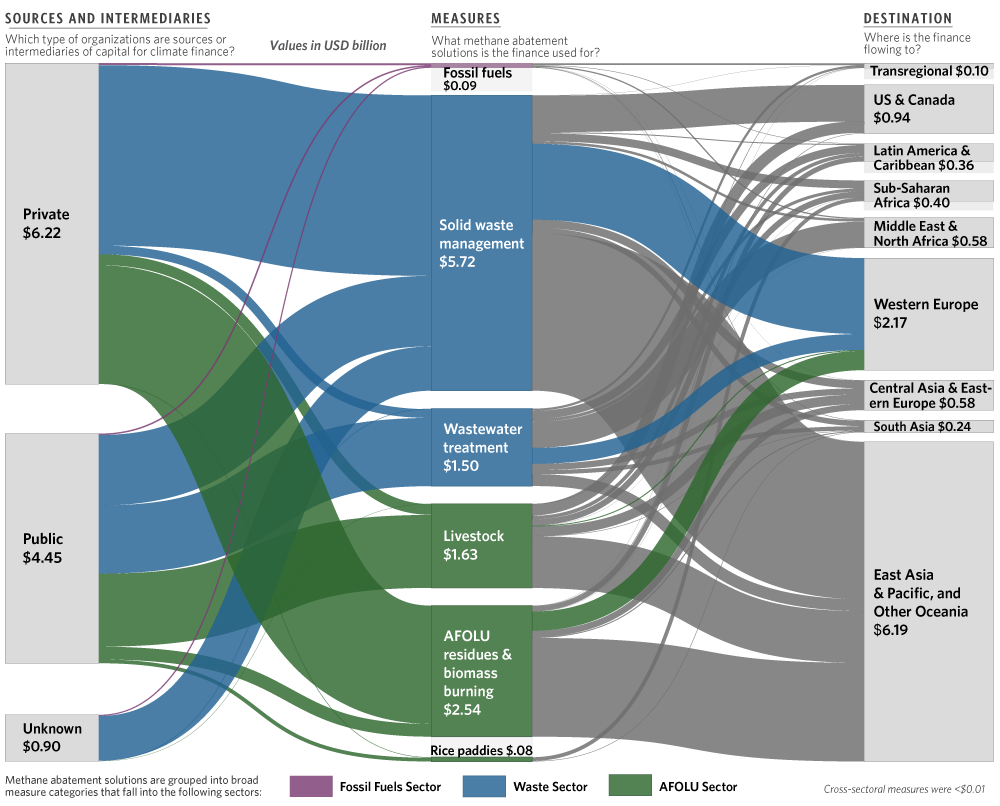

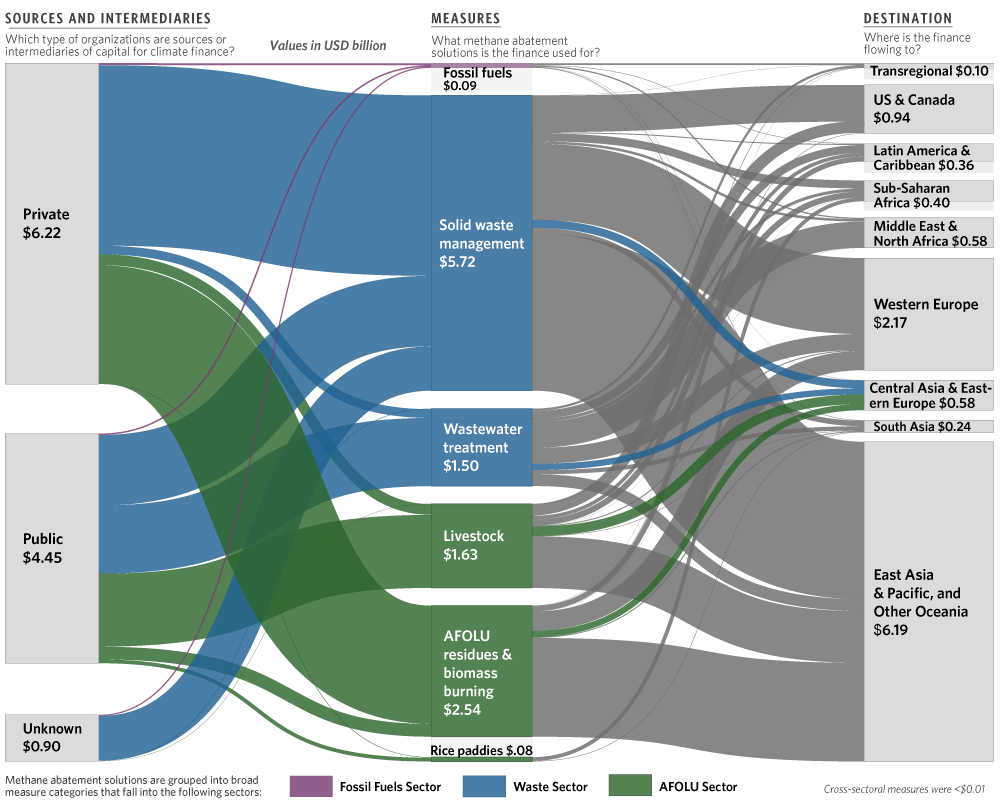

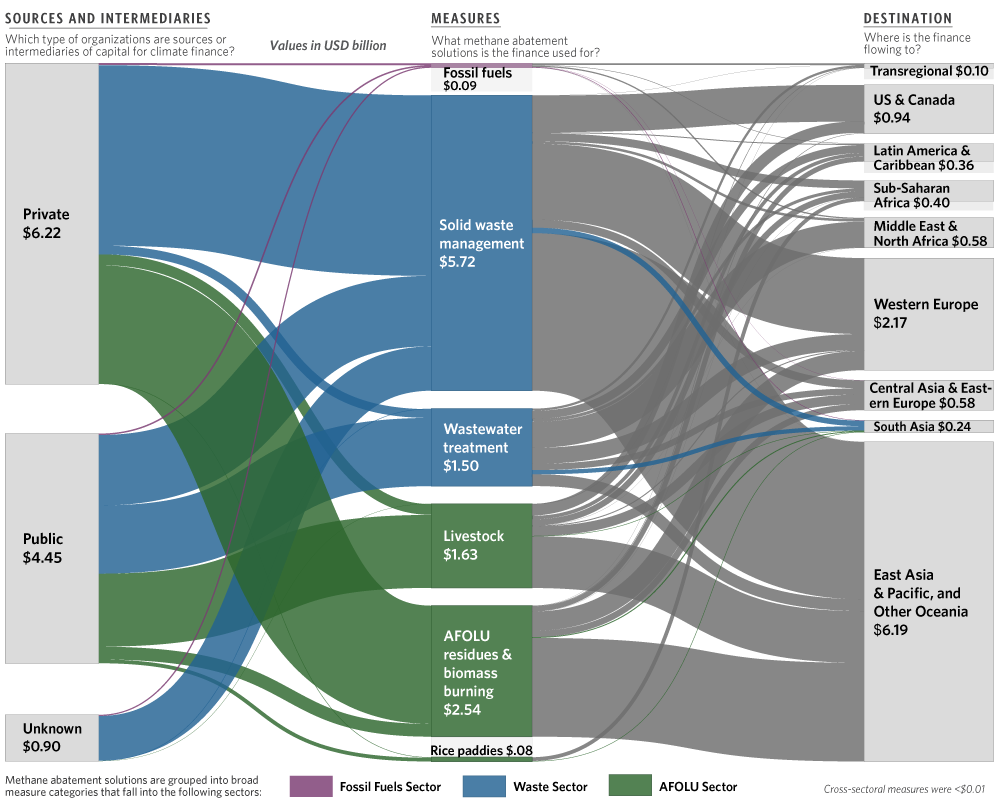

Global targeted methane abatement finance flows in 2019/2020

Our findings show that current investment in targeted methane abatement is not enough to limit global warming to 1.5°C and that the limited existing investment flows are not being directed to the geographies or sectors of highest abatement potential. Key takeaways from this analysis include:

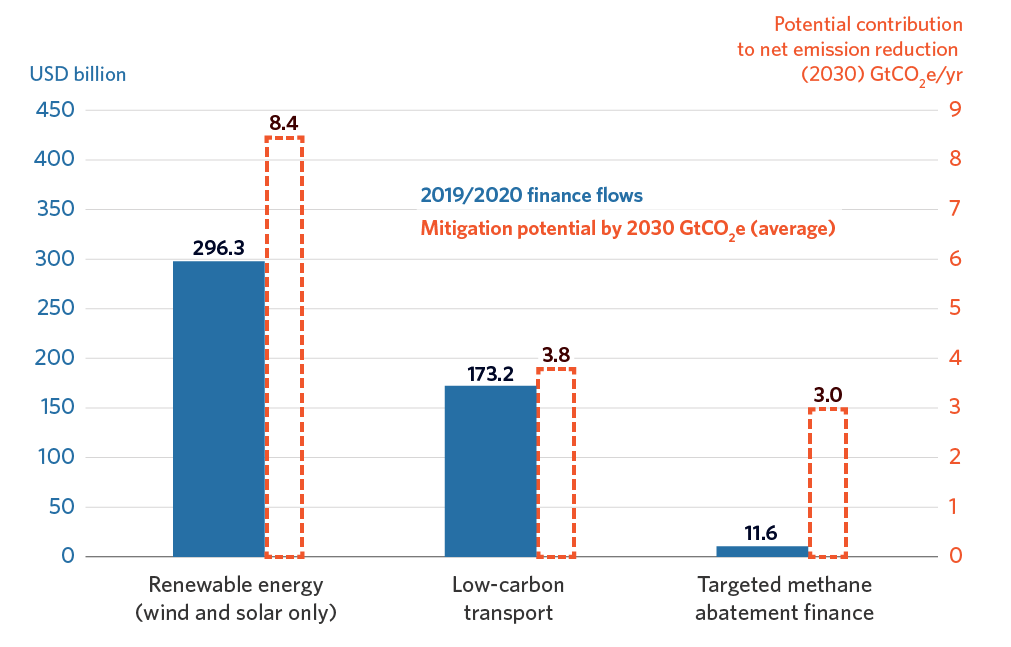

- Methane abatement solutions are severely underfunded considering their climate change mitigation potential. While also underfunded, other climate change solutions with similar mitigation potential, such as low-carbon transport, received 15 times the investment of methane abatement measures, while solutions such as solar and wind received 26 times the investment.

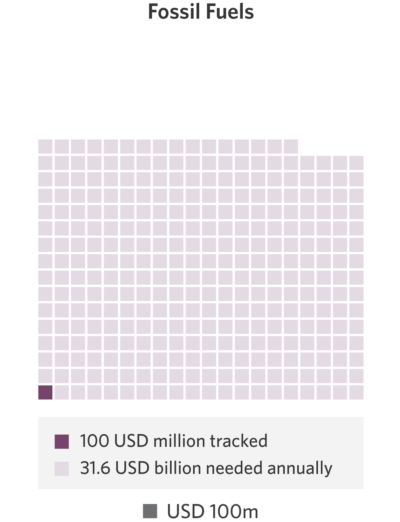

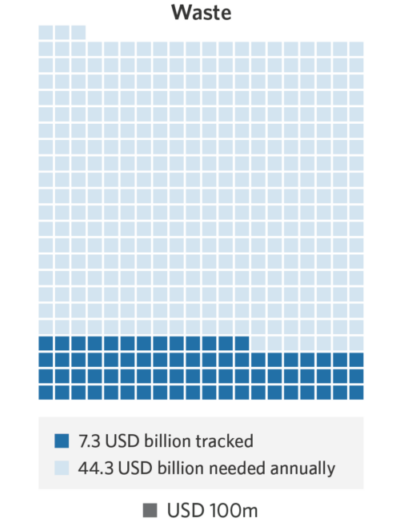

- The fossil fuel sector has the highest potential for methane mitigation potential by 2030, yet by far received the lowest amount of methane abatement finance. Eighty-two percent of anthropogenic methane emissions originated from activities in the fossil fuel and agriculture sectors, yet the fossil fuel sector received less than 1% of methane abatement finance (USD 0.1 billion). Almost two-thirds of methane abatement funding was directed towards the waste sector.

- Regionally, most methane emissions originate in the East Asia and Pacific region, and most of the methane abatement finance in 2019/2020 was concentrated there. However, significant abatement potential exists in other regions, particularly in Latin America and the Caribbean and Sub-Saharan Africa, respectively the second and third largest methane emitters, which combined attracted only 6% of methane abatement finance.

- The private sector accounted for the majority of tracked financial flows, particularly in more mature segments (e.g., certain waste-to-energy technologies) where commercial viability at scale is well established.

- Within the public sector, development finance institutions were a key source of financing, accounting for 13% of all methane abatement flows in 2019/2020.

Despite the availability of cost effective and market ready abatement solutions, business and policy strategies for methane reduction are not prioritized by policymakers and investors. The Global Methane Pledge has brought together nearly 120 countries in support of methane emissions reductions. Building on this momentum, countries should develop concrete methane reduction plans, as well as financing strategies, to leverage methane abatement’s fast mitigation benefit and unique impact opportunity.

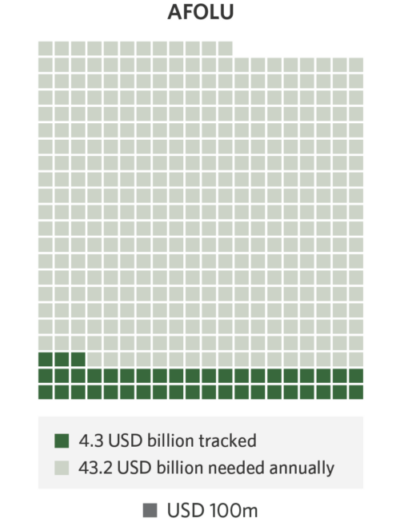

Tracked methane abatement investment, annual needs through 2050

To ensure key stakeholders adequately invest in methane mitigation, we recommend that public actors:

- Cultivate a strong enabling environment for methane mitigation projects by providing enhanced regulatory signals and binding policy that are tailored to key sectors and specify minimum standards, and penalties, for methane emissions.

- Work to set sector-specific benchmarks and catalogue best practices and investment needs across the key methane-relevant sectors.

- Develop common approaches to track the finance for, and impact of, methane abatement interventions, including through improved methane emissions measurement approaches to quantify methane reductions impact of climate finance.

- Build a dedicated pipeline of investable methane reduction projects across sectors, including through existing development and climate finance structures.

- Incentivize the uptake of existing technologies, redirect capital from energy intensive activities to methane reducing activities, and direct spending towards methane abatement research and development.

We recommend that private sector financial and corporate actors:

- Incorporate ambitious and rapidly escalating methane reduction targets in interim net-zero goals.

- Monitor Scope 1, 2, and 3 methane emissions and improve transparency on methane-related capital expenditures.

- Promptly deploy existing methane abatement solutions and provide catalytic finance support to innovate methane abatement solutions.

- Annually report on progress towards meeting abatement and finance goals.

Methane abatement finance has one of the highest ratios of global warming benefit per dollar of capital invested. The world cannot avoid the worst impacts of climate change without sufficient finance flows towards methane abatement. Both public and private actors have an essential role to play in closing the methane abatement finance gap.

[1] CPI reports two-year averages (2019 and 2020) to smooth out annual fluctuations in data.