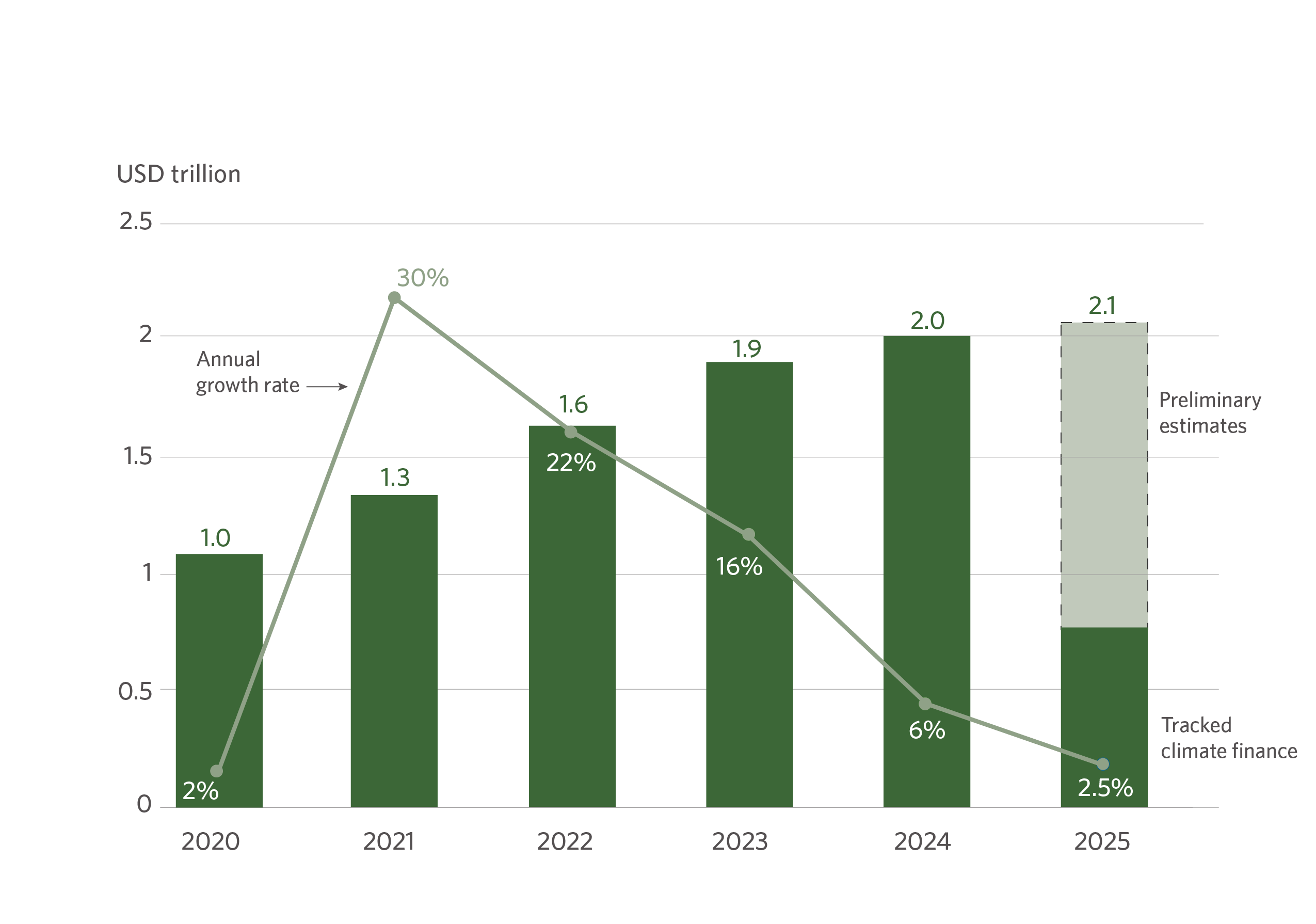

23 June, London—Global climate finance surpassed USD 2 trillion for the first time in 2024 with growth to USD 2.1 trillion estimated in 2025, according to Climate Policy Initiative’s latest Global Landscape of Climate Finance 2026 report.

Flows have grown every year over the last half-decade, despite COVID-19, energy market volatility, sovereign debt pressure, and geopolitical conflicts, pointing to resilient underlying structures for climate finance, including a maturing investment market for key climate solutions.

Yet, the annual rate of growth is slowing when acceleration is needed. Growth has decelerated from a 30% surge in 2021, to 6% in 2024, and an estimated 2–3% in 2025. While this deceleration may partly reflect maturing markets or declining technology costs, sustained, double-digit growth is required to meet climate goals.

At these rates, flows will not reach even the lowest estimated mitigation needs until well into the 2030s, exacerbating climate-related risks and putting investment further off track.

CPI’s latest report examines how climate investment can continue scaling at the pace required.

Where climate finance is growing, and where more is needed

The Global Landscape of Climate Finance 2026 identifies the key drivers of climate finance momentum, and highlights where targeted action can unlock the next wave of investment.

- Mitigation finance reached USD 1.9 trillion in 2024, but is concentrated in the energy sector. There is ample opportunity to expand that success across a wider range of sectors critical for a low-carbon, climate-resilient future.

- Other high-emitting sectors, such as agriculture, industry, and waste, still struggle to attract the required finance. Combined, they receive a small and volatile share of flows, presenting significant policy and investment opportunities.

- Domestic markets and households are driving growth. Over USD 1.7 trillion—85% of climate investment—was mobilized through domestic markets in 2024. Households invested USD 332 billion in low-carbon solutions, including EVs, heat pumps, and small-scale renewables, taking advantage of falling costs, better performance, shortening payback periods, and fiscal incentives.

- Private finance continues to outpace global public flows.

- Private investment drove climate finance growth, with flows exceeding USD 1.2 trillion and a 19% compound annual growth rate (CAGR) for the years from 2019 to 2024.

- International public climate finance fell by 6% in 2024, after increasing by 33% in 2022 and 20% in 2023.

- Commercial financial institutions more than doubled their flows between 2019 and 2024, reaching USD 572 billion.

- Emerging markets and developing economies (EMDEs) are in the driving seat for future climate finance growth. While advanced economies and China consistently account for around 80% of global flows, EMDEs excluding China and least developed countries (LDCs) are now the fastest–growing country grouping, with a 25% compound annual growth rate from 2022 to 2024.

- To continue this momentum, domestic resource mobilization, capital market deepening, and strategic use of public finance are increasingly important. Development finance providers will need to target their capital to leverage additional investment, deploying a range of instruments including catalytic equity. Country-led investment frameworks can also help to address fragmentation and efficiently channel resources to financing opportunities that deliver against countries’ own development plans and priorities.

“Climate finance has proven its resilience, growing through a pandemic, an energy crisis, and geopolitical upheaval,” said Barbara Buchner, CPI’s CEO. “The task now is to pick up pace. Further acceleration must take us to at least USD 6.2 trillion annually by 2035 to ensure a climate-aligned, sustainable world. This is within our reach if we mirror the success from earlier in this decade.”

“The shift we’re seeing in EMDEs is one of the most important stories in climate finance,” said Dharshan Wignarajah, CPI’s UK Director. “South Asia, sub-Saharan Africa, and Latin America hold significant investment opportunities in grid expansion, utility-scale and distributed solar, and clean transport. The conditions to unlock private investment are within reach, and this is precisely the moment for smarter, more catalytic international cooperation.”

Media contact

Jana Stupperich, Senior Communications Associate: jana.stupperich@cpiglobal.org