Connecting Capital within African Agrifood Systems

Capital flows to African agrifood systems remain far below what is needed. While the climate finance gap is well documented, less understood is why capital so often fails to reach agrifood enterprises.

This report explores a core challenge within capital mobilization for African agrifood systems: the misalignment between how investors allocate capital and how agribusinesses operate. Investors deploying capital through climate finance vehicles seek risk-adjusted returns that meet their mandates, which are frequently misaligned with enterprise realities. This misalignment is systemic, rooted in investor return expectations, underdeveloped local financial markets, and policy environments that do not yet effectively support agricultural finance. Addressing these root causes will require long-term policy and market development; however, Africa’s agrifood systems need capital now.

CPI is well-placed to examine this misalignment because it operates on both sides of the market within the current ecosystem. We analyze how the supply and demand sides of capital can connect more efficiently, drawing on our experience providing technical assistance (TA) to investors and enterprises through the ClimateShot Investor Coalition (CLIC) Connector, Global Innovation Lab for Climate Finance (the Lab), and the Catalytic Climate Finance Facility (CC Facility). These are distinct programs which operate at different points on the capital continuum, but running them in parallel has nonetheless given us a cross-cutting view of where and why supply- and demand-side activity align and diverge.

Through these three programs, we have gained insights into the needs of both vehicles deploying capital and agrifood enterprises raising funds. We identify that among the most practical levers for investment the development of well-structured vehicles that effectively mitigate and price risks, address risk-return misalignment, and make projects bankable. While enterprise-level TA can improve an agribusiness’s investor-readiness, it can rarely, on its own, shift the risk-return profile that an investor sees in a deal and governs capital flow. Closing that gap typically requires complementary TA at the vehicle level.

Drawing on CPI’s experience supporting both funders and enterprises, this report identifies high-impact, practical actions to help capital flow more effectively and strengthen Africa’s agrifood investment ecosystem.

PORTFOLIO INSIGHTS

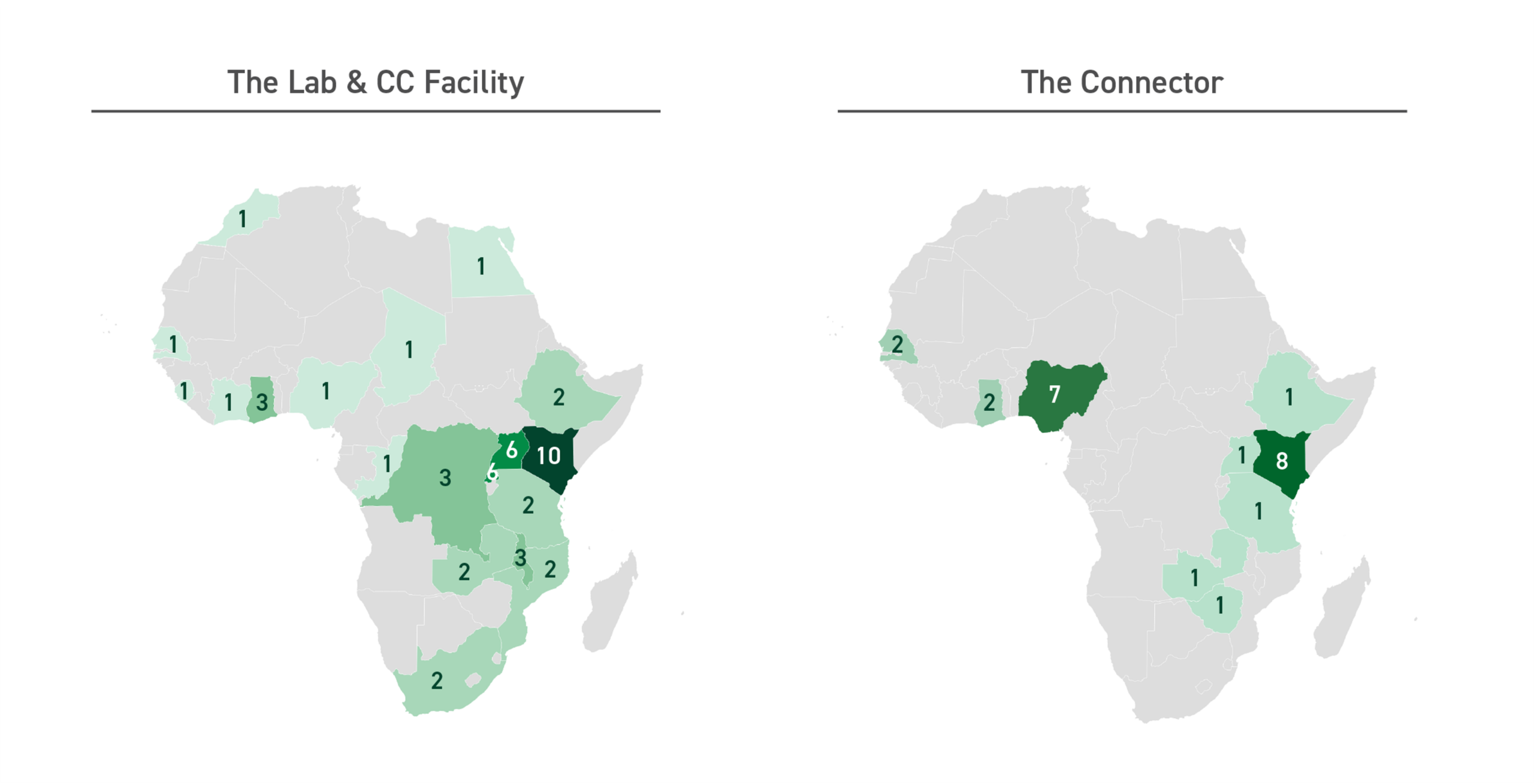

We analyze CPI’s diverse African agrifood portfolio to distill evidence-based lessons and actionable recommendations for funders and TA providers. The evidence base spans 23 agribusinesses supported through the Connector, and 17 climate finance vehicles incubated and accelerated through the Lab and CC Facility, as well as CPI’s broader ecosystem-building activities. For more information on each vehicle or enterprise, please visit their profile pages on the Connector, Lab, and CC Facility websites.

Geographical presence

Activity is concentrated in a small number of established agrifood markets, with Kenya, Nigeria, and Uganda accounting for nearly half of all engagements across programs. This concentration is not a program design choice; instead, it reflects the characteristics of African markets where investor activity, financial infrastructure, and SME ecosystems are more developed.

Markets where conditions for capital mobilization are strongest are not necessarily those where the need for climate investment is greatest. Many of the geographies facing the most acute food security and climate adaptation pressures are precisely those where investor presence, intermediary capacity, and enterprise pipeline are thinnest. For example, the ten most vulnerable countries in Africa only received 11% of climate finance flows in 2024.

Value chain stage

Finance vehicles are heavily concentrated in upstream production activities, such as on-farm climate adaptation, input financing, and smallholder lending. This partly reflects where catalytic finance has found it easier to operate, as production-level activities offer more measurable outcomes that align with the requirements of concessional capital providers.

The enterprise portfolio is more evenly spread across the value chain. In contexts where intermediary infrastructure connecting producer to buyer is weak or absent, enterprises tend to operate end-to-end across the value chain. This helps secure independent routes to market and reduce exposure to supply chain disruptions.

This difference in focus between enterprises and funds can create a mismatch in capital demand and supply. Finance vehicles tend to be designed around upstream segments, while the enterprises seeking capital frequently operate across the value chain. As a result, a vehicle specifically mandated for upstream production may not readily accommodate an enterprise that also operates at the midstream and downstream stages.

Crop type

Over half of Lab and CC Facility vehicles do not specify a crop focus at the design stage, reflecting broader agrifood or climate mandates that leave crop selection to the fund manager post-capitalization. Where vehicles do specify a crop focus, cash crops are well represented relative to their share of regional production, consistent with investor preference for export-oriented, hard-currency value chains. Coffee and cacao tend to dominate these mandates:sFor fund managers building a first commercial track record, these value chains offer the most defensible route to demonstrating returns.

On the enterprise side, the Connector portfolio is split among cash crops (46%), other staple crops (40%), and maize (14%). Staple crops underpin regional and domestic food security and rural livelihoods but operate on thinner margins, face higher climate exposure, have limited access to premium markets, and sit less comfortably inside the structured finance architectures that mobilize international capital.

Staple crops feature heavily in the enterprise pipeline but are not strongly represented in the vehicles designed to reach commercial scale. Maize, rice, sorghum, and millet sit at the center of food security, yet the financing architecture reaching enterprises focused on these crops is thinner, more concessional, and smaller in ticket size than what is needed to support cash crop value chains.

Impact area

Adaptation is the strongest area of convergence across the portfolio, although each program addresses it differently. The Lab and CC Facility support capital-intensive adaptation solutions, including irrigation systems, storage infrastructure, weather-indexed insurance, and fintech tools. The Connector supports localized, on-farm adaptation through soil and water management practices, drought-tolerant seeds, organic fertilizers, regenerative agriculture, and digital advisory tools.

Gender is addressed through distinct but reinforcing pathways. The Connector integrates a gender lens into its selection process, supporting agribusinesses that are led or founded by women, or specifically serve female farmers and vendors. The Lab addresses gender by expanding finance for women-led agribusinesses, while the CC Facility embeds gender requirements in grant terms and acceleration support, requiring and supporting grantees to develop and operationalize gender strategies.

LESSONS LEARNED

Our cross-program experience points to four features of agrifood climate finance TA that can support capital flows more effectively.

1. Effective vehicle design starts with a clear understanding of demand. An effective investment vehicle fills a specific market gap, either by generating a pipeline where none exists or by creating a funding structure that moves a backlog of viable enterprises off the ground. When mandates default to what investors are familiar with rather than to actual investable opportunities, deal flow can narrow significantly. Embedding granular knowledge of enterprise characteristics, ticket sizes, absorption capacity, and financing needs into mandate-setting from the outset calibrates vehicles to market realities.

2. Moving from concept to investment requires alignment between pipelines, agribusiness needs, and investor mandates. Geographic or thematic overlap between investment supply and demand is the starting condition for financial deployment. Converting overlap into transactions requires active intermediation. CPI’s experience shows that supply and demand do not align spontaneously, even across shared geographies and value chains. Facilitation needs to be built in as its own function

CPI does this in two complementary ways: pipeline identification and analysis are integral to our vehicle-level work, and addressing market fragmentation through ecosystem building is core to how our programs operate. This dual vantage point gives us insight into both the structural conditions that govern capital flow and the practical mechanics that bridge supply and demand.

3. Enterprise preparation is most effective when calibrated to specific investor requirements. Generic TA builds a necessary foundation, but investment conversion depends on calibration with the screening criteria and risk parameters of the capital being targeted. That calibration increasingly extends to local and context-specific dynamics, as investors prioritize locally-led vehicles and projects with strong anchoring on the ground. Demand-side programs that maintain active connections to supply-side intelligence can materially improve the rate at which enterprises convert into an investable pipeline.

4. Mobilizing private capital at scale and supporting food security are distinct goals that call for distinct vehicles. Vehicles built to mobilize commercial capital tend to focus on export-oriented, hard-currency value chains. Diversification, liquidity, and scalability all reward cash crops. CPI-supported vehicles reflect this: over half target cash crops or are crop-agnostic due to investor preferences. As a result, financial structures purpose-built for local food crop economies remain in short supply.

Advancing food security and resilience at scale will require concessional, grant-based, or public funding alongside commercial vehicles. Blended finance is the clearest example of how this can work: by combining concessional and commercial capital, it aligns multiple investor mandates around a shared risk-return profile and channels investment into markets that would otherwise remain underserved or stuck at an early stage.

RECOMMENDATIONS

Acting on these findings requires deliberate shifts in how TA is designed, funded, and delivered, and represents a high-leverage opportunity for the donors and funders best placed to back this work. Every dollar of TA funding for both vehicles and SMEs across CPI’s agrifood portfolio has mobilized commercial and concessional investment many multiples of its size, making systemic market support among the most efficient uses of catalytic grant capital. This report sets out six recommendations, directed at the actors best positioned to implement each.