The population in developing and emerging countries is urbanizing at three times the rate of developed countries. But cities in the ‘Global South’ have limited access to capital to invest in water, energy, housing and transportation systems to meet the needs of growing urban populations.

Many of them raise capital through local banking sectors whose loan terms are often unsuitable for funding new infrastructure. Capital markets offer an alternative source of cheaper and longer-term finance but less than 20% of cities in developing countries have access to local capital markets and only 4% have access to international capital markets.

In recent years, green bond markets have emerged as a new way for investors in the capital markets to access sustainable investments. Cities have taken note. European cities in France and Sweden have been issuing green bonds since 2012. Municipalities in the US have a long track record of raising low-cost debt in the municipal bond market but only recently have begun to label bonds as ‘green’ in order to meet this demand signal from investors.

So how much finance has flowed from green bond markets to cities in developing countries?

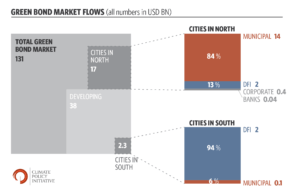

Climate Policy Initiative (CPI) analysis shown in the chart below shows that approximately USD 2.2 billion of total flows in the green bond market have been directed towards cities in developing countries (“the South”) compared to USD 17 billion in developed countries (“the North”).

The figure below breaks down the sources of those flows to cities in the North and South. Cities in the North mainly use their own municipal (MUNI) issuance power (84%) but also benefit from Development Finance Institutions (DFI) linking city-based projects to their green bonds (13%) while cities in the developing countries in contrast rely almost entirely on DFIs to raise finance for their projects (94%).

To date, Johannesburg’s USD 137 million bond is the only municipal green bond issued in developing countries. Important work to help address this imbalance is underway. It aims to develop local capital markets and improve the creditworthiness of cities.

But if a city cannot issue bonds, what is the potential of other channels open to them to access finance from green bond markets? Helping local governments and city administrators in developing countries to identify these channels and increase their access to the green bond markets is one way to close this investment gap. This is why CPI is contributing analysis and developing guidelines for accessing the green bond markets as part of the Green Bonds for Cities project.

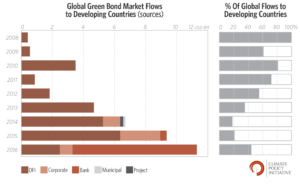

Our analysis shows the sources of green bond market flows to developing countries are diversifying.

Since 2008, USD 39 billion has been directed to projects or activities in developing countries. From 2008-2013, this consisted entirely of flows from Development Finance Institutions but, from 2014, domestic corporate issuance began to grow and was then joined by issuance from commercial banks from China and India in 2016.

Clearly, cities don’t necessarily need to issue their own bonds to tap the green bond market. City or municipal-based infrastructure development companies could provide one option for them to do so. Such companies commonly raise finance in developing countries such as China, often with central government guarantees.

Public-private partnerships with corporations or commercial banking institutions could help cities leverage their green bond issuances for new infrastructure developments.

Perhaps the avenue with the most significant potential is through domestic, bilateral and multilateral development finance institutions (DFIs). DFIs could scale up their own green bond mandates to increase support for city-based infrastructure in developing countries, work to source and help finance projects, and eventually support cities to issue their own bonds through guarantees or other risk mitigation instruments.

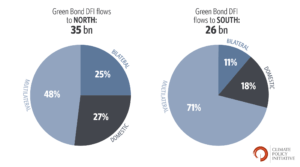

The chart above reveals three interesting insights into DFIs’ green bond issuance:

- Domestic DFIs in developing countries, such as NAFIN in Mexico and the Agricultural Bank of China, already account for 18% of total flows from DFIs’ green bonds to the South. They could provide a potential source of collaboration for cities.

- Multilateral DFIs such as the World Bank, EIB, ADB and AfDB currently only link USD 2 billion of the USD 18 billion flowing to the south to city-based projects. There is potential to scale-up.

- In combination, multilateral and bilateral DFIs such as EIB, EBRD and KfW’s send more green bond flows to projects in the North than the South. USD 25 billion of flows goes to the North versus USD 21 billion of flows to projects in the South.

CPI’s analysis will inform guidelines for city administrators and stakeholders in developing countries on how to develop a market access strategy for the Green Bonds for Cities project. From autumn 2016, this project will provide toolkits and training sessions with the aim of expanding green bond market flows to cities in the South.

CPI is working with South Pole Group on this in collaboration with ICLEI and Climate Bonds Initiative. The project is funded as part of the Low-Carbon City Lab (LoCaL) under Climate KIC.

This op-ed was originally published on Environmental Finance.