Executive Summary

The government of India plans to more than double the renewable energy capacity installed in the country from 25 GW in 2012 to 55 GW by 2017. However, renewable energy is still approximately 52-129% more expensive than conventional power (CPI, 2014b). In our previous work (CPI, 2012), we found that the biggest barrier to renewable energy in India is the inferior terms of debt – i.e., high cost, short tenor, and variable rate – which raises the cost of renewable energy in India by 24-32% compared with similar projects in the US.

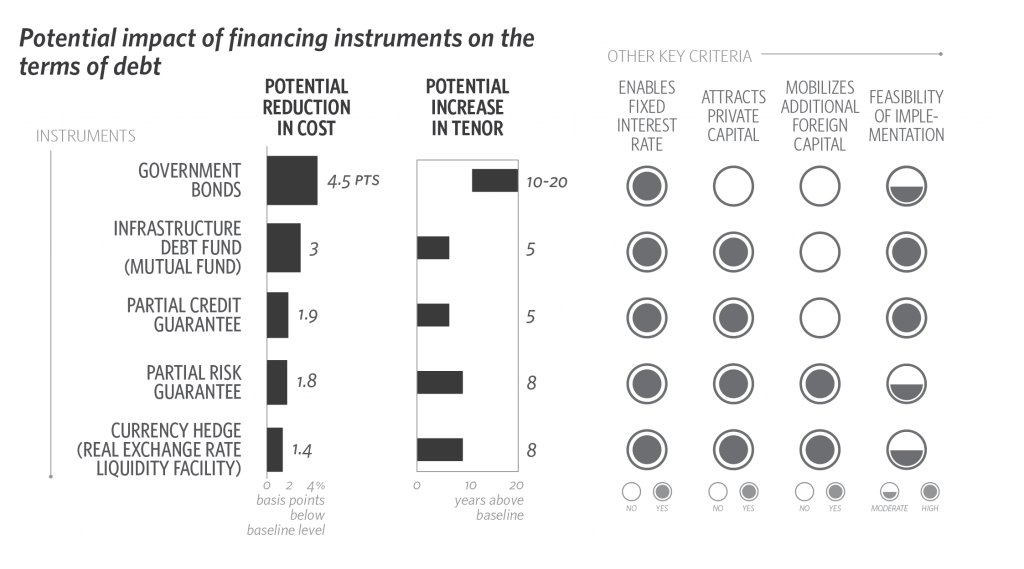

While a number of financing instruments that have been used elsewhere could contribute to solving the main problems in financing renewables in India, none are currently available. In this paper, we explore financing instruments, used in other regions as well as those that were recently introduced in India in other contexts that have the potential to provide and/or facilitate low-cost, long-term debt for renewable energy in India.

We explored three categories of instruments used to finance renewable energy around the world: (a) instruments that provide access to previously untapped lowcost, long-term funds from domestic capital markets; (b) instruments that provide access to foreign debt; and (c) guarantee instruments that mitigate the risk associated with projects. We then further analyzed five instruments for: (1) their cost reduction potential, (2) their potential to increase tenor of funds, and (3) whether they provide fixed interest rates. For each instrument, we also considered (4) potential to mobilize private capital, (5) potential to attract foreign investments; and (6) feasibility of implementation. The figure below presents our results.